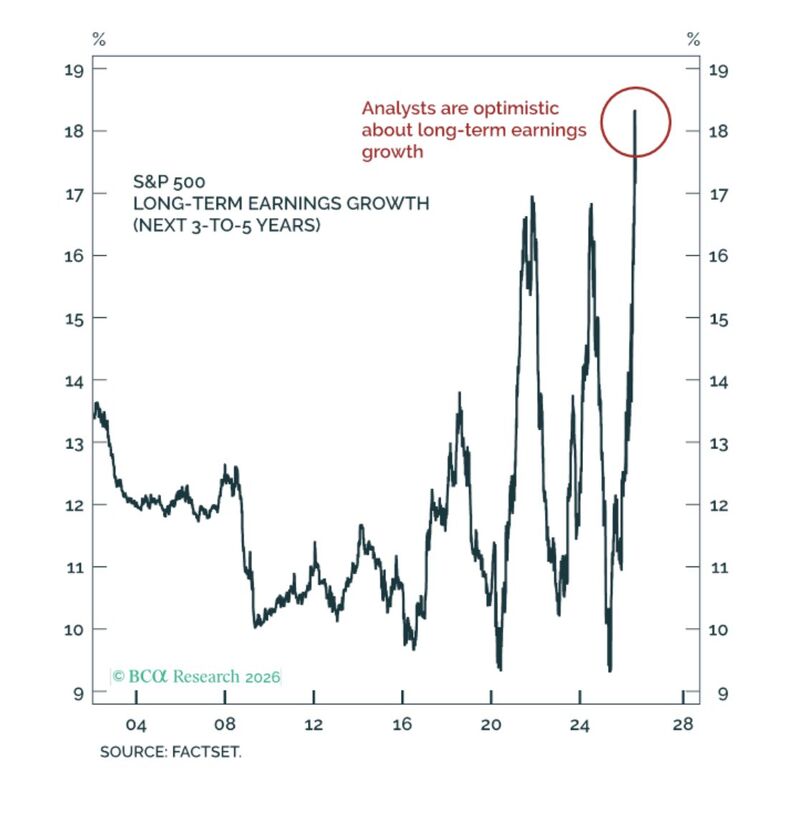

Peak optimism?

Source: Peter Berezin

🔴 $ASML fantastic Q2 2026 earnings ‼️

ASML on Wednesday raised its guidance for the second time this year and reported stronger-than-expected quarterly results as its customers continue to ramp up production of AI chips. The Dutch semiconductor-equipment maker said it now expects full-year sales to come in between 43 billion euros ($49 billion) and 45 billion euros, and a gross margin of between 54 and 56%. It previously predicted annual net sales of between 36 billion and 40 billion euros, and a gross margin between 51% and 53%. The opened up 7% and is now up 64% YTD. Market cap is close to EUR 630 billion. ASML Q2 results In a nutshell: • EPS: €7.59 vs €6.88 est. • Revenue: €9.33B vs €8.87B est. • Gross Margin: 54.0% vs 51.9% est. 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 𝗤𝟯 𝟮𝟬𝟮𝟲 Revenue: €11B-$12B vs €10.34B est. 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 𝟮𝟬𝟮𝟲 Revenue: €43B-$45B vs €39.34B est. Source: Investing visuals @InvestingVisual CNBC

JP MORGAN $JPM

Q2’26 EARNINGS HIGHLIGHTS 🔹 Revenue: $58.02B (Est. $51.39B) 🟢; +27% YoY 🔹 EPS: $7.70 (Est. $5.72) 🟢; incl. $1.56/share from significant items 🔹 NII: $25.62B (Est. $25.64B) 🟡; +10% YoY 🔹 Net Charge-Offs: $2.37B (Est. $2.62B) 🟢 🔹 Investment Banking: $3.9B (Est. $3.06B) 🟢; +45% YoY 🔹 Equities S&T: $6.03B (Est. $3.98B) 🟢; +86% YoY 🔹 FICC S&T: $6.05B (Est. $6.29B) 🔴; +6% YoY Other Metrics: 🔹 Loans: $1.54T (Est. $1.52T) 🟢 🔹 Total Deposits: $2.71T (Est. $2.69T) 🟢 🔹 AUM: $5.1T; +18% YoY Segment Performance: 🔹 Consumer & Community Banking Revenue: $20.27B; +8% YoY 🔹 Commercial & Investment Bank Revenue: $24.85B; +27% YoY 🔹 Asset & Wealth Management Revenue: $6.85B; +19% YoY Financials: 🔹 Net Income: $21.2B; +41% YoY 🔹 Provision for Credit Losses: $2.52B 🔹 ROE: 24% (Est. 18%) 🟢 🔹 ROTCE: 29% 🔹 Standardized CET1 Ratio: 14.1% Capital Return: 🔹 Dividend: $1.50/share 🔹 Buybacks: $6.2B of common stock net repurchases 🔹 Authorization: New $50B buyback program effective July 1, 2026 Source: Wall St Engine

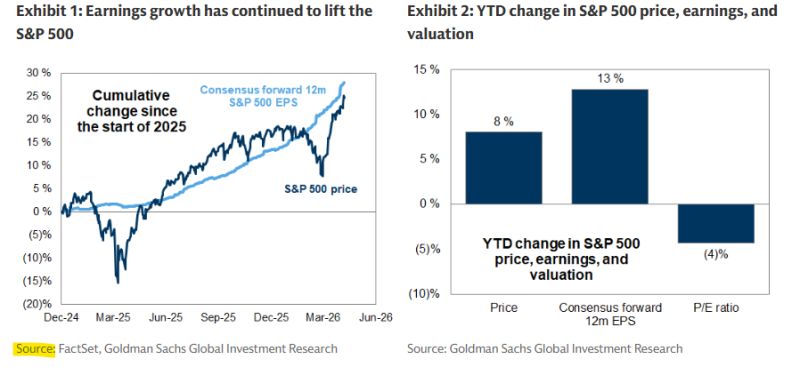

Since the start of 2026, the S&P 500 has risen by +8%, consensus forward 12-month EPS estimates have risen by +13%, and the P/E multiple has declined from 22x to 21x.

Source: Neil Sethi, Goldman Sachs

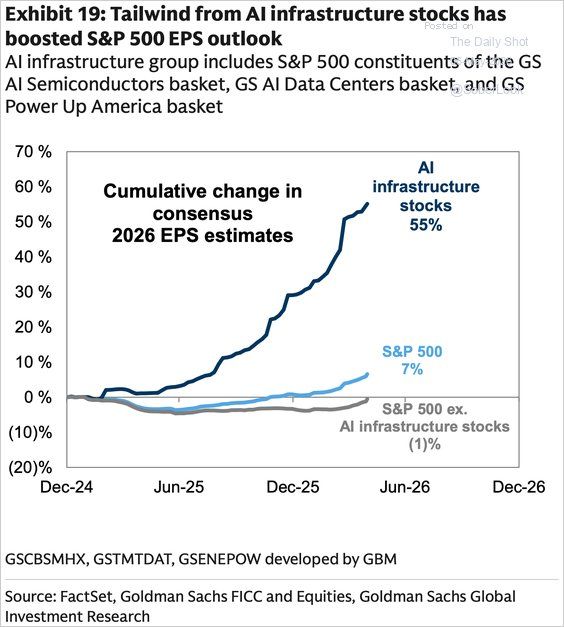

Upward revisions to earnings, which have been very sharp, have come mostly from AI infrastructure stocks where growth is very strong.

Source: Lance Roberts, Goldman Sachs, The Daily Shot

320 companies out of the S&P500 have reported earnings this season.

Of the 320, the average earnings surprise has been 20% so far, the US seeing the biggest beats in years. Source: Bloomberg, Negligible Capital

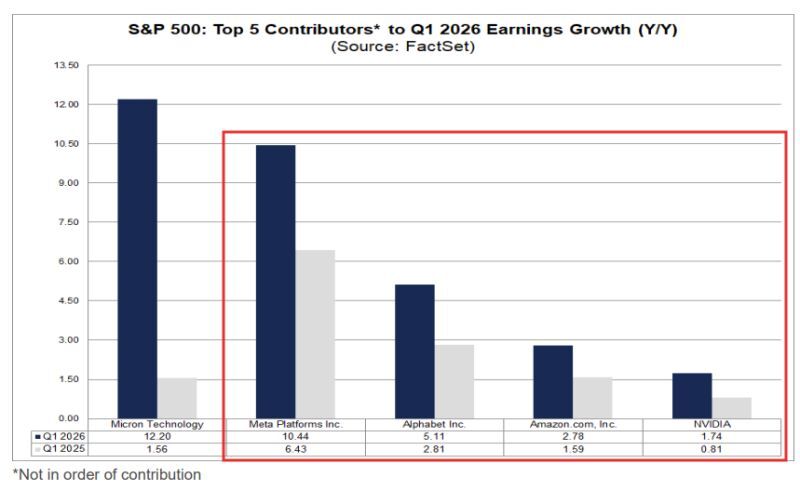

Factset notes that Mag-7 GAAP earnings growth for Q1 is now expected to come in at an astounding +61.0% up from 22.4% at the end of the quarter

(March 31st) with 4 of the top 5 contributors to SPX earnings growth coming from this cohort (Alphabet, NVIDIA, Amazon and Meta, the other is Micron) That said, Factset notes that the three of those who have reported though each were boosted by one-time non-cash items: "The (GAAP) EPS actual for Alphabet for Q1 2026 included a net gain of $37.7 billion primarily due to net unrealized gains on non-marketable equity securities. The (GAAP) EPS actual for Amazon.com for Q1 2026 included pre-tax gains of $16.8 billion included in non-operating income from investments in Anthropic. The (GAAP) EPS actual for Meta Platforms for Q1 2026 included an $8.03 billion income tax benefit." Source: Factset, Neil Sethi

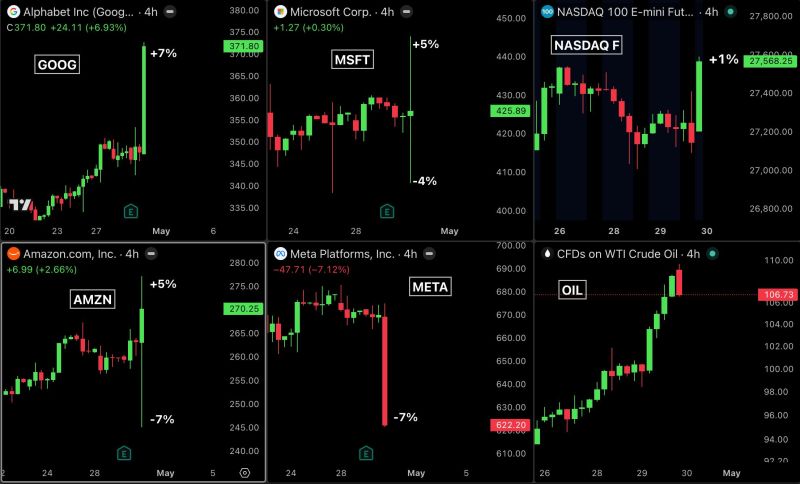

The "MAGNIFICENT 7" just reported the biggest revenue surge in stock market history.

Google nearly doubled what Wall Street expected. EPS came in at $5.11 against an estimate of $2.63, a 94% beat. Revenue hit $109 billion against an estimate of $107 billion. $GOOG jumped 7% and hit a new all time high. Microsoft beat every expectation. EPS of $4.27 against an estimate of $4.06. Revenue of $82 billion against an estimate of $81 billion. $MSFT gained 5%. Amazon had one of the biggest EPS beats of any company its size in years. EPS of $2.78 against an estimate of $1.64, a 70% beat. Revenue of $181 billion against an estimate of $177 billion. $AMZN dropped 7% immediately after the report and then fully recovered to close up 4%. Meta beat every single number Wall Street had. EPS of $10.4 against an estimate of $6.82, a 52% beat. Revenue of $56 billion against an estimate of $55 billion. $META dropped 7% anyway. Source: Bull Theory