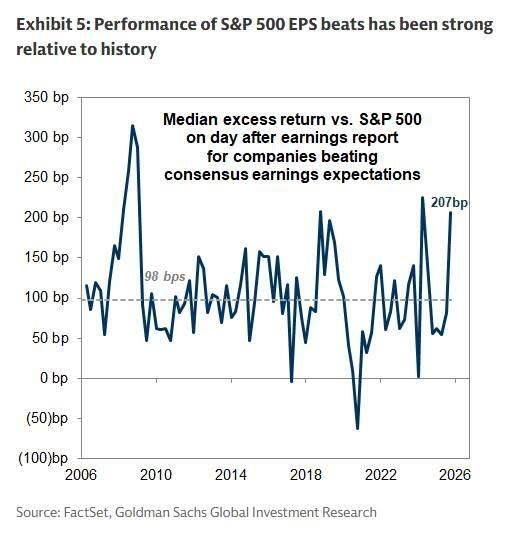

Goldman notes that after a few quarters of uninspiring market that follows positive earnings release, beats are finally being rewarded.

Companies beating consensus EPS estimates have outperformed on the day after reporting by +207 bp on average, more than double the historical average of +98 bp.

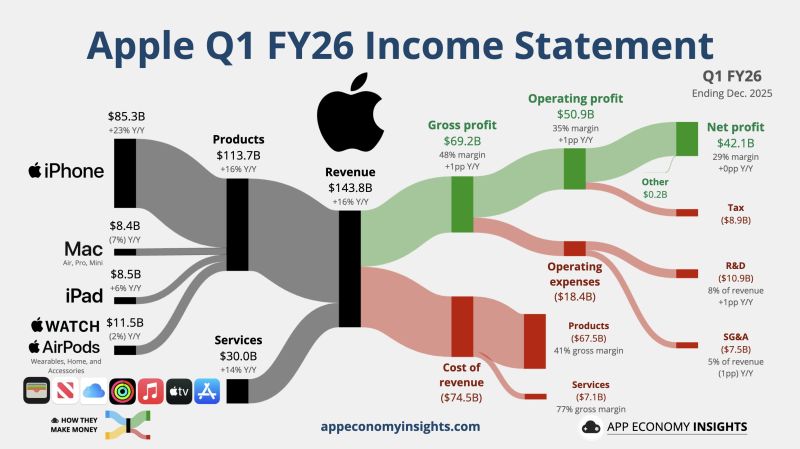

📢 Apple reported fiscal first-quarter earnings on Thursday that surpassed expectations, with revenue soaring 16% on an annual basis.

📌 The company reported $42.1 billion in net income, or $2.84 per share, versus $36.33 billion, or $2.40 per share, in the year-ago period. 🚀 Apple saw particularly strong results in China, including Taiwan and Hong Kong. Sales in the region surged 38% during the quarter to $25.53 billion. Apple quarterly results by App Economy Insights $AAPL Apple Q1 FY26 (Dec. quarter): 📱 Products +16% Y/Y to $113.7B. 💳 Services +14% Y/Y to $30.0B. • Revenue +16% Y/Y to $143.8B ($5.2B beat). • Operating margin 35% (+1pp Y/Y). • EPS $2.84 ($0.17 beat).

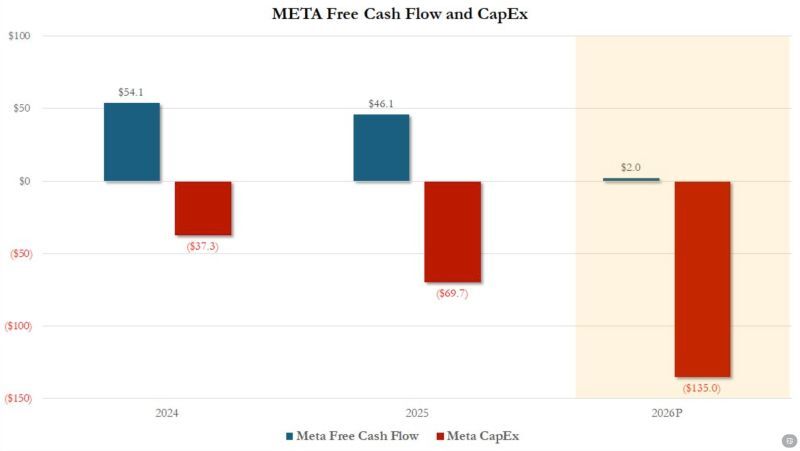

At the high end of its capex forecast ($135BN), META free cash flow in 2026 will be $0

Source: zerohedge

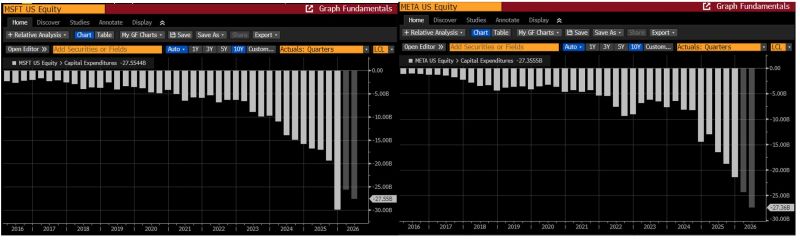

Microsoft and Meta quarterly CAPEX -realised and projected

These aren’t the old MSFT and META... Source: Bloomberg, RBC

MSFT and META quarterly results (and capex projections) confirm our thesis: these are not your "old" Mag 7.

Indeed, the AI revolution has hit a major turning point as the largest U.S. tech companies embark on unprecedented AI infrastructure spending. The Magnificent 7 are now turning from Asset light to Asset Heavy. Although markets have so far rewarded this surge in investment, history shows that capex booms often lead to overbuilding, intensified competition, and disappointing stock performance. From Magnificent 7 to Magnificent risks ???

ASML just dropped their Q4-25 earnings, and the market is absolutely electric. ⚡️

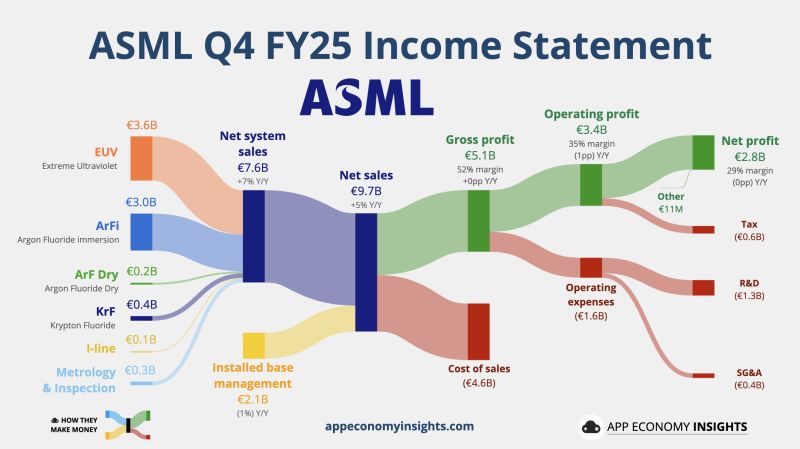

Shares jumped 7%, and it’s not hard to see why. While the world was debating an "AI bubble," ASML’s customers just placed a record-breaking bet on the future. The headline? A massive demand explosion. 🚀 The Numbers You Need to Know: Net Bookings: €13.2B (Massive beat vs. €7B estimate). The demand isn't just there; it’s doubling expectations. Revenue: €9.7B (Beating the €9.58B estimate). Backlog: A staggering €38.8B. ASML has years of work already sold. 2026 Guidance: Revenue projected between €34B - €39B (Top end well above the €35B consensus). The "AI Realism" Shift 🧠 CEO Christophe Fouquet’s statement is the real kicker. He noted a "notably more positive assessment" from customers regarding the sustainability of AI-related demand. This isn't hype. This is capacity planning. This is the "picks and shovels" of the AI revolution being bolted into factories right now. Two High NA systems (the most complex machines humans have ever built) were officially recognized in Q4 revenue. The future is being shipped. Shareholder Value 💰 ASML isn't just growing; they are rewarding. A new €12B share buyback program through 2028 shows massive confidence in their long-term cash flow. The Verdict: ASML remains the ultimate bottleneck of the digital age. If you want AI, you need chips. If you want chips, you need ASML. Period. Is the semi-cycle just getting a second wind? 🌬️ Below the numbers and breakdown by App Economy Insights @EconomyApp · $ASML ASML Q4 FY25: • Net bookings €13.2B (€6.9B beat). • Net sales +5% Y/Y to €9.7B (€0.1B beat). • Gross margin 52% (+0pp Y/Y). • Operating margin 35% (-1pp Y/Y). • EPS €7.35 (€0.23 miss). • FY26 Net sales ~€36.5B (€1.4B beat).

THE MASTER EARNINGS CALENDAR

Here are the most popular stocks that report earnings this week January 26th - January 30th Source: Earnings Hub

Q4 earnings season officially kicks off yesterday.

Source: Brew markets