1.2 million Korean investors were hit with margin calls in a single market crash.

That's roughly 1 in every 30 working-age adults in the country. As the KOSPI plunged 8.95%—its third-worst session since Lehman—more than 1.2 million leveraged retail accounts triggered margin calls. Around 320,000–360,000 accounts were fully liquidated, with some investors left owing money even after their positions were sold. The damage was brutal: SK Hynix: -15.4% (largest daily drop on record) Samsung: -10.7% Meanwhile, retail brokerage cash balances have fallen by ₩30 trillion to their lowest level since February. And here's the key point: forced-selling data lags by two days. The full impact of Monday's liquidation wave has **not even appeared in the official figures yet. Source: Bull Theory

JP MORGAN $JPM

Q2’26 EARNINGS HIGHLIGHTS 🔹 Revenue: $58.02B (Est. $51.39B) 🟢; +27% YoY 🔹 EPS: $7.70 (Est. $5.72) 🟢; incl. $1.56/share from significant items 🔹 NII: $25.62B (Est. $25.64B) 🟡; +10% YoY 🔹 Net Charge-Offs: $2.37B (Est. $2.62B) 🟢 🔹 Investment Banking: $3.9B (Est. $3.06B) 🟢; +45% YoY 🔹 Equities S&T: $6.03B (Est. $3.98B) 🟢; +86% YoY 🔹 FICC S&T: $6.05B (Est. $6.29B) 🔴; +6% YoY Other Metrics: 🔹 Loans: $1.54T (Est. $1.52T) 🟢 🔹 Total Deposits: $2.71T (Est. $2.69T) 🟢 🔹 AUM: $5.1T; +18% YoY Segment Performance: 🔹 Consumer & Community Banking Revenue: $20.27B; +8% YoY 🔹 Commercial & Investment Bank Revenue: $24.85B; +27% YoY 🔹 Asset & Wealth Management Revenue: $6.85B; +19% YoY Financials: 🔹 Net Income: $21.2B; +41% YoY 🔹 Provision for Credit Losses: $2.52B 🔹 ROE: 24% (Est. 18%) 🟢 🔹 ROTCE: 29% 🔹 Standardized CET1 Ratio: 14.1% Capital Return: 🔹 Dividend: $1.50/share 🔹 Buybacks: $6.2B of common stock net repurchases 🔹 Authorization: New $50B buyback program effective July 1, 2026 Source: Wall St Engine

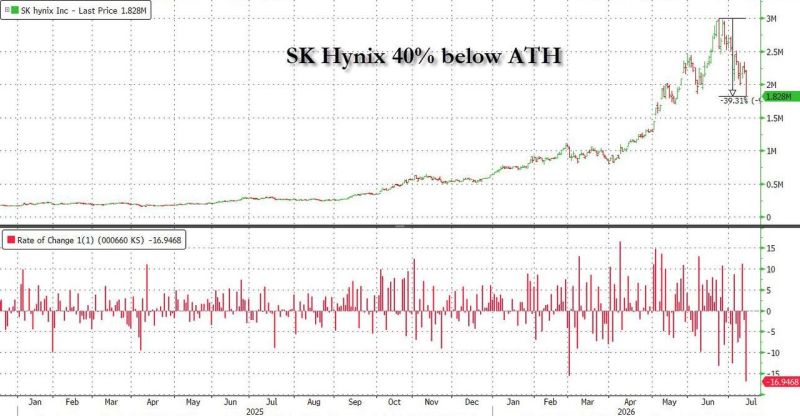

SK Hynix has now plunged 40% from its all-time high just a few weeks ago

Source: zerohedge

South Korea's KOSPI stock market trading has been halted for 20 minutes after crashing -8%.

Over ₩488,000,000,000,000 ($328 BILLION) has been wiped out from South Korean stocks today. Source: Bull Theory

This is how leverage turns a pullback into a wipeout.

The 2x leveraged SK Hynix ETF listed in Hong Kong has plunged 64% from its June peak after SK Hynix shares fell more than 35%, including a record 15% one-day drop on Monday. Many South Korean retail investors rushed into these leveraged ETFs after their launch, expecting to amplify AI-driven gains. Instead, extreme volatility and daily rebalancing accelerated losses, with reports of forced liquidations already emerging. The lesson is simple: leverage doesn't just amplify returns—it magnifies mistakes. In volatile markets, it can destroy capital far faster than most investors expect. Source: Global Markets Investor

Healthcare Stocks just formed a Golden Cross for the first time since October 2025

The last one sent prices higher by 10% over the next 10 weeks Source: Barchart

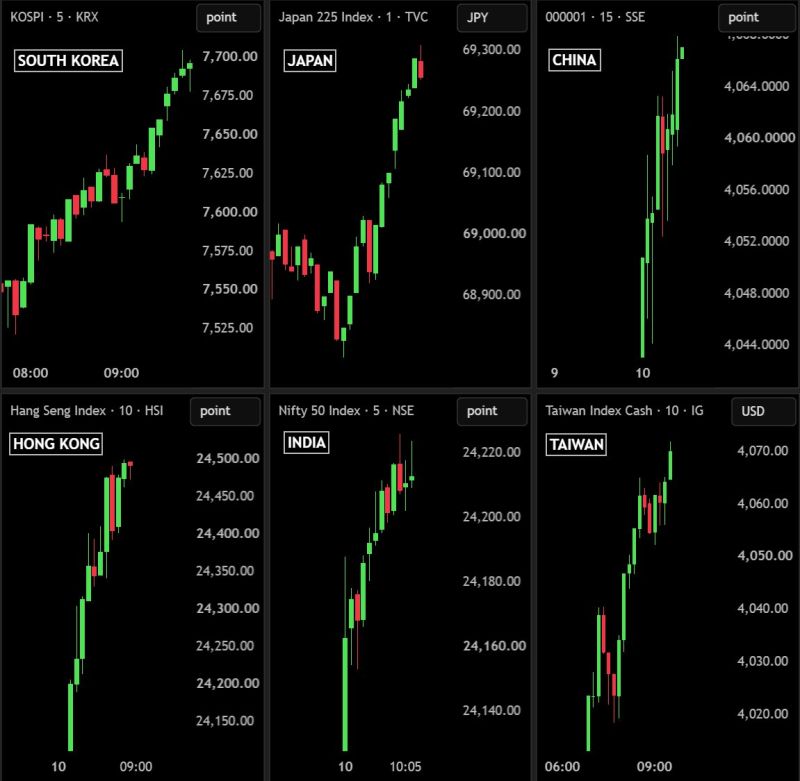

Massive Reversal in Asian Markets

Over $500 BILLION has been added to Asian stocks today as semiconductor and AI stocks rebounded after the recent sell-off, following a strong close on U.S. stocks. South Korea's KOSPI is up +4.6%, adding ₩280.6 trillion ($189B). Japan's NIKKEI is up +1.6%, adding ¥22.9 trillion ($139B). Taiwan is up +1.2%, adding NT4.1 trillion ($50B). China's SSE is up +0.8%, adding ¥520 billion ($73B). Hong Kong's HSI is up +1.5%, adding HK$131.6 billion ($17B). India's NIFTY is up +1.0%, adding ₹4.9 trillion ($57B). Source: Bull Theory

To put things into perspective: The Nasdaq 100 is currently trading at ~23x NTM P/E

which is broadly inline with its 10y average multiple and towards the lower end of its 3-4y range, Goldman says, Source: HolgerZ, Bloomberg