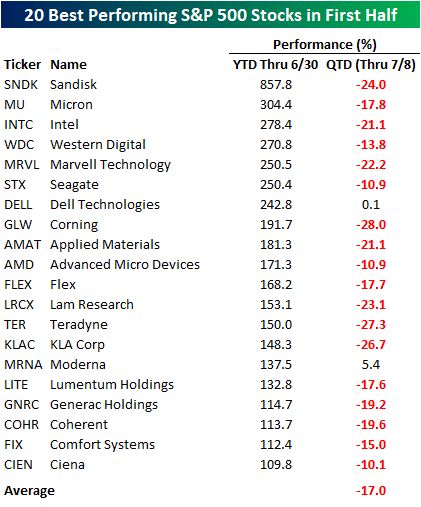

Of the 20 top performing stocks in the first half (nearly all tech), only two are up so far in Q3, and the average QTD decline is 17%.

Source: Bespoke @bespokeinvest

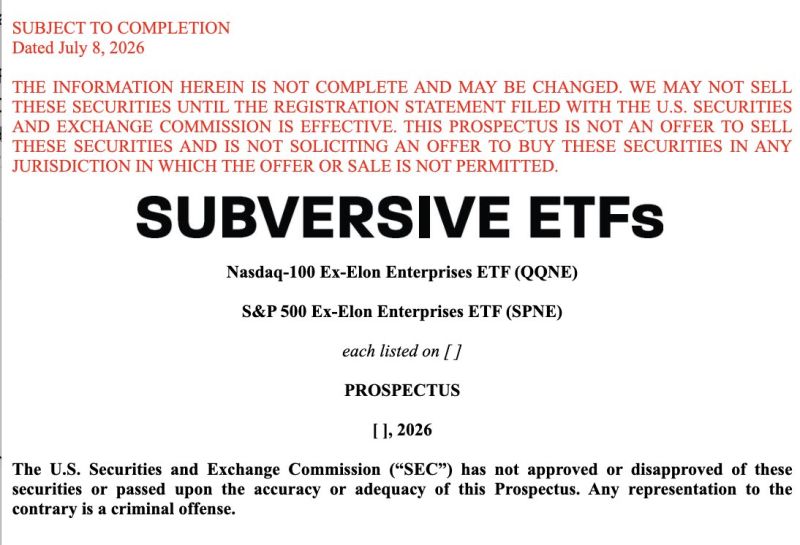

Someone just filed for a Nasdaq 100 and S&P 500 that owns everyone EXCEPT Elon Musk owned companies.

Source: Evan on X

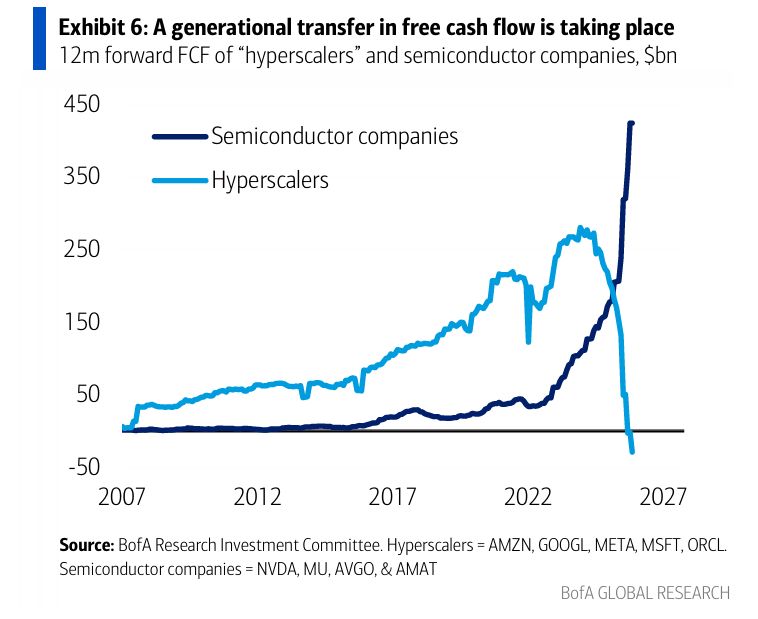

"A generational transfer in free cash flow is taking place"

- BofA Source: zerohedge

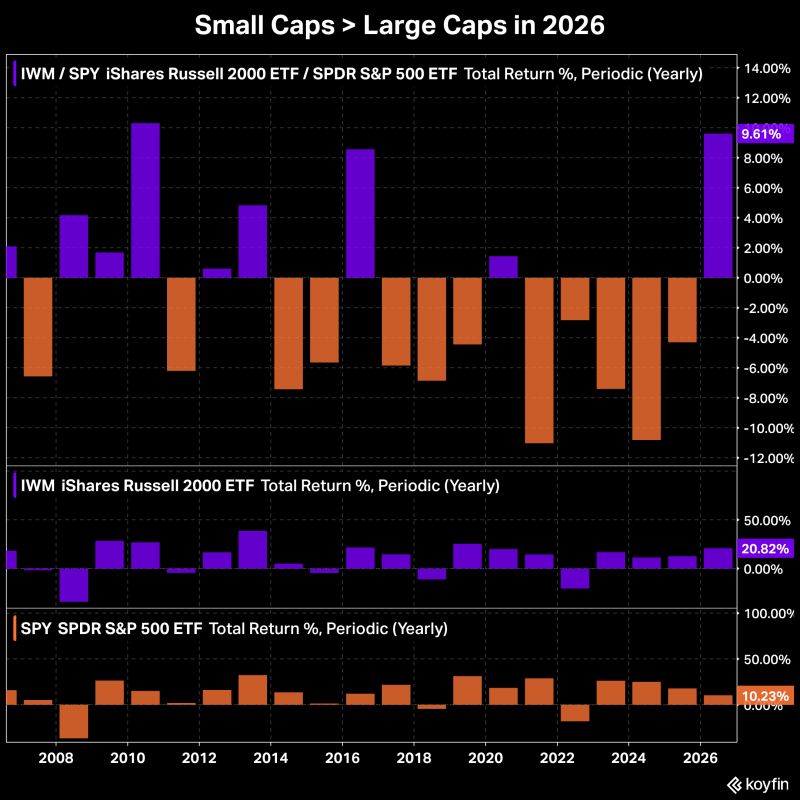

As somewhat of a rarity this decade, small caps (Russell 2000) are outperforming large caps (S&P 500) so far in 2026.

If sustained to the end of the year, it would end 5-years of consecutive annual outperformance by large caps. Source: Koyfin

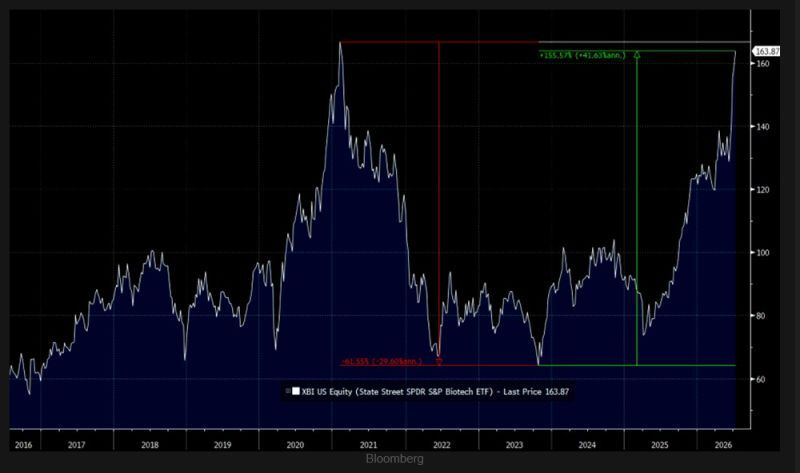

Biotech bull

After enduring a 62% collapse, biotech has come roaring back. A combination of M&A optimism and positive clinical news has propelled XBI 156% off its 2023 lows, putting the ETF within touching distance of its 2021 highs. Source: TME

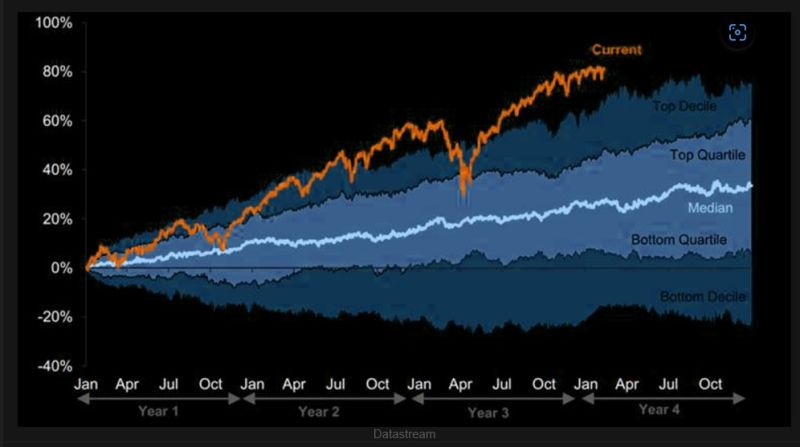

Extraordinary 3.5 years 🚀

With nearly a century of market history as the backdrop, the S&P 500's surge since late 2022 stands out as one of the more extraordinary rallies in modern market history. Source: The Market Ear

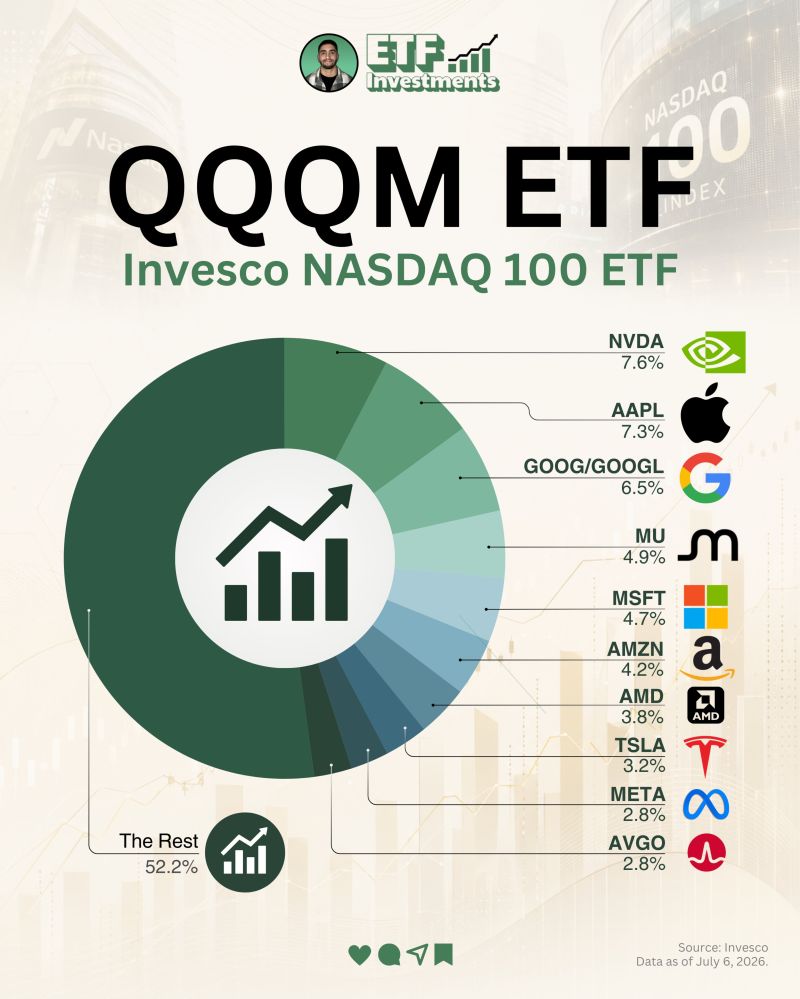

Inside $QQQM, Invesco's take on the Nasdaq-100

It holds around 100 of the largest nonfinancial companies listed on the Nasdaq, tilted heavily toward tech and growth names. $NVDA: 7.6% - designs the GPUs powering AI and gaming $AAPL: 7.3% - makes the iPhone, Mac, and a growing services business $GOOG/$GOOGL: 6.5% - runs Google Search, YouTube, and Google Cloud $MU: 4.9% - builds memory and storage chips for computers and data centers $MSFT: 4.7% - sells Windows, Office, and Azure cloud services $AMZN: 4.2% - runs the largest US online store plus AWS cloud $AMD: 3.8% - makes processors and graphics chips for PCs and servers $TSLA: 3.2% - builds electric vehicles and energy storage systems Source: ETF Investments

🚨 Markets sold off in the market as US Central Command forces have begun a series of powerful strikes on Iran in retaliation for Iranian attacks on commercial vessels in the Strait of Hormuz.

The US military called Iran's hostility "unjustified, perilous, and a clear breach of ceasefire." Iranian state media reports seven explosions in Sirik. $1 TRILLION was wiped out from stocks, precious metals, and crypto within 30 minutes after the US announced it was revoking Iran's oil export license Gold dumped -1.33% Silver dumped -2.67% Nasdaq dumped -1.87% S&P 500 dumped -0.46% Oil jumped 5% Source: Bull Theory Crypto is down $27 billion.