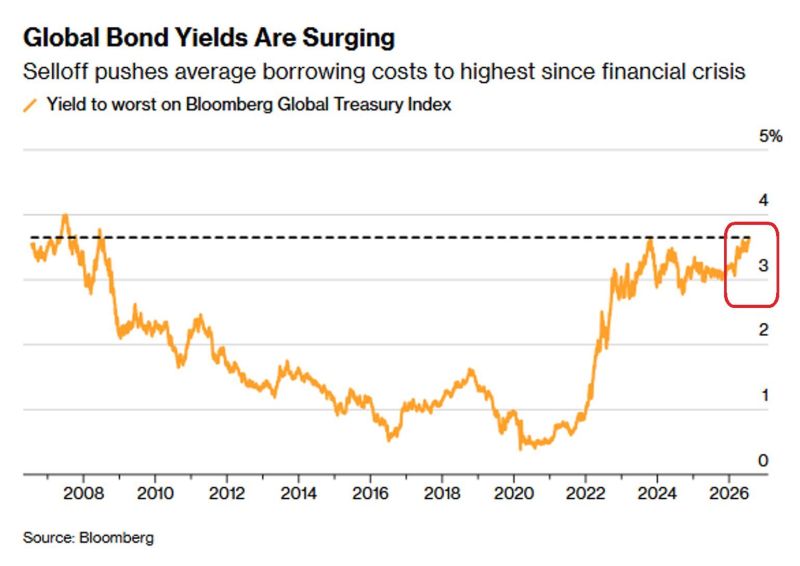

Global bond yields hit highest level since 2008

Source: Hedgeye, Bloomberg

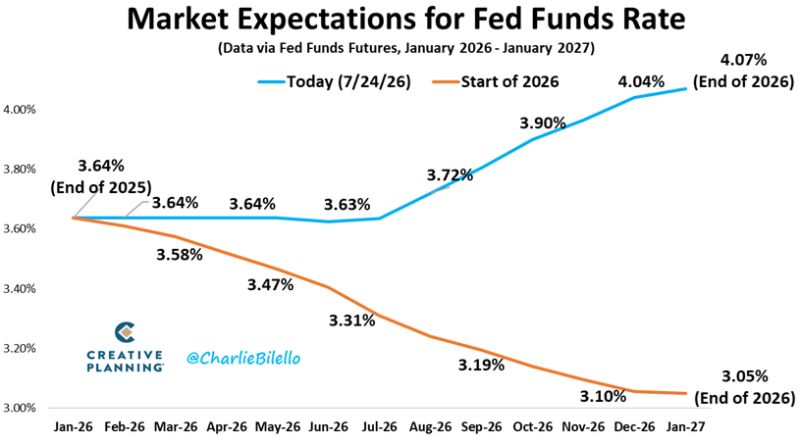

At the start of the year, the bond market was pricing in 2 Fed rate CUTS.

Today it's pricing in 1 to 2 Fed rate HIKES. That's a 1% swing in expectations. Source: Charlie Bilello

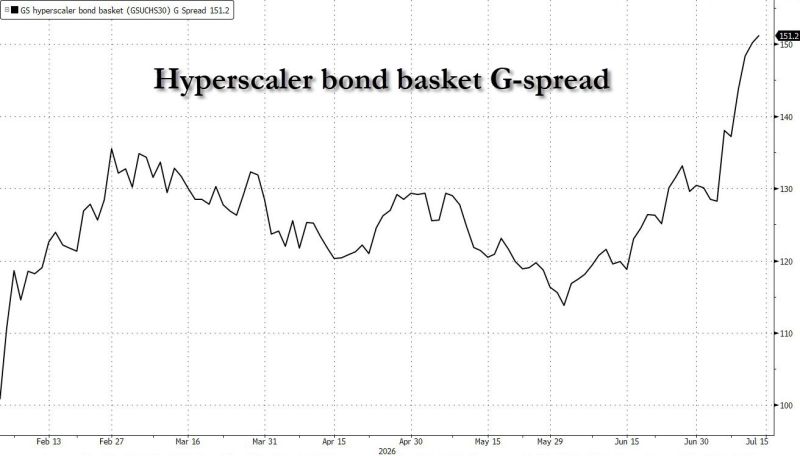

Carnage in hyperscaler bond land:

Investment Grade bond spreads for hyperscalers are exploding every day, as credit investors refuse to fund memory chip purchases any longer. CDS (inverted in red on the chart below) are following. How long will it take for the hyperscaler stocks (in blue) to follow ? Source: zerohedge

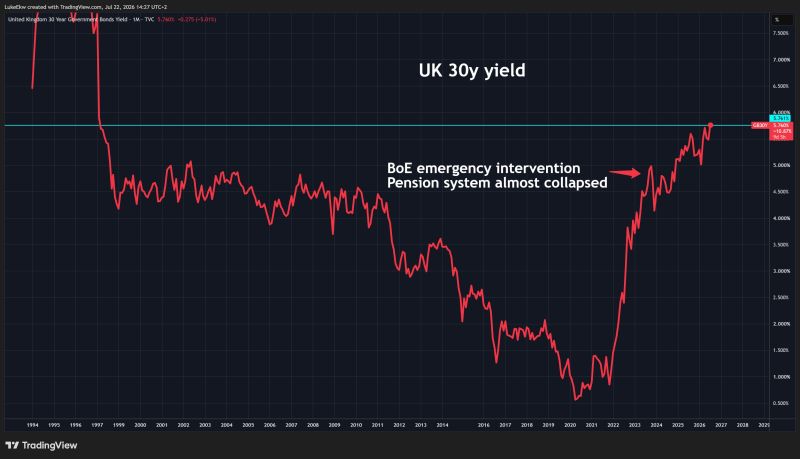

UK 30-year government bond yields have risen to the highest level in 3 decades.

From 2020-2026, they surged from 0.5% to 5.7%... UK pension funds are heavily exposed to Gilts and are suffering heavy paper losses Source: Lukas Ekwueme, Bloomberg

Hyperscaler bond basket: another day, another record wide

Source: zerohedge

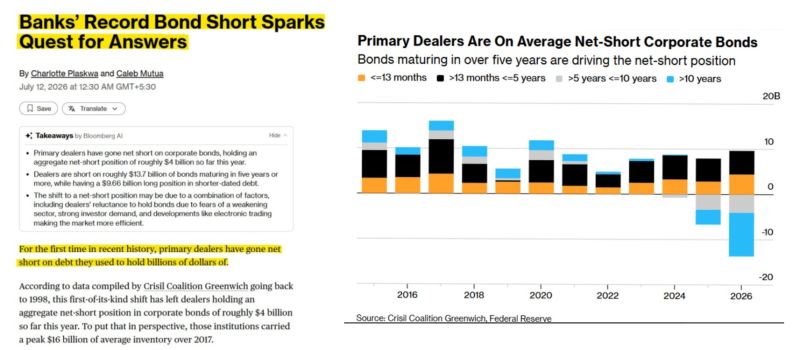

For the first time since 1998, primary dealers are net short corporate bonds.

They've sold more credit exposure than they actually own—a dramatic shift from holding an average $16B of inventory in 2017. Most of the short position is in longer-dated bonds, where rising yields hurt the most. With credit spreads near multi-decade lows, the reward for taking that risk is minimal. If yields keep rising, dealers look well positioned. But if bonds rally, they could be forced to cover into a market with limited supply, accelerating the move. One thing history shows: credit markets often crack—or recover—before equities do. Source: Bull Theory

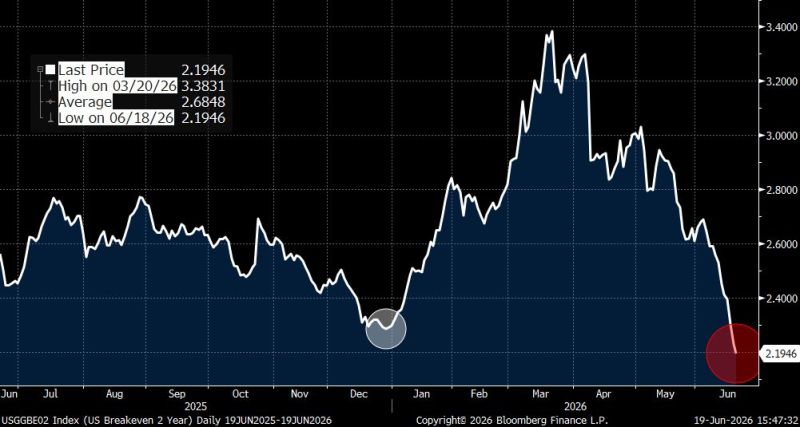

The bond market is sending a clear message: inflation fears are fading.

The 2-year breakeven inflation rate is now lower than it was at the start of the year, signaling that investors expect less inflation over the next two years. With oil prices continuing to soften, markets are increasingly pricing in disinflation, not a resurgence in inflation. Forget headlines and forecasts—breakeven inflation reflects where investors are putting real money. The narrative is shifting from inflation panic to lower inflation expectations. Are markets right, or are they underestimating inflation risks? Source: Bloomberg, Manish Singh

Nvidia is planning to sell at least $20bn of investment-grade debt in the US its first bond sale in more than five years in a test of investor appetite for further exposure to the AI sector.

Source: FT