Yields on 10y gilts have risen well above 5%, reaching their highest level since 2008 due to the UK government crisis.

Keir Starmer's premiership appears to be hanging by a thread after his much-anticipated policy reset speech on Monday - in response to the Labour Party's poor performance in recent local elections - failed to deliver the shift many MPs demanded. Starmer said on Tuesday that he wasn't going anywhere, but with calls for his departure mounting, he looks to be fighting a losing battle. Source: HolgerZ, Bloomberg

Japan's 20Y bond yield rises as high as 3.511%, highest since 1996 as global interest rates go vertical

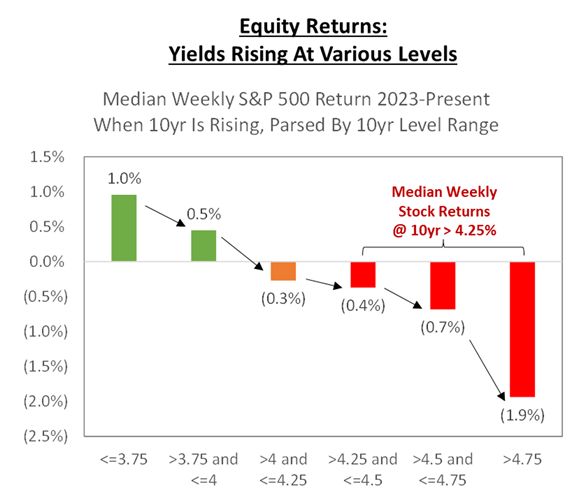

With the long bond over 5% and the 10yr dancing around 4.50%, maybe it is worth to have a look at it again... Kantro had nice look back at the median weekly stock returns versus yields - see chart below. Source: Kantro, RBC

How does the sp500 perform when the US 10 year yield crosses key levels?

With the long bond over 5% and the 10yr dancing around 4.50%, maybe it is worth to have a look at it again... Kantro had nice look back at the median weekly stock returns versus yields - see chart below. Source: Kantro, RBC

The bond market’s inflation outlook just collapsed from over 5.3% to 3.0% over the next twelve months.

Source: Hedgeye, Bloomberg

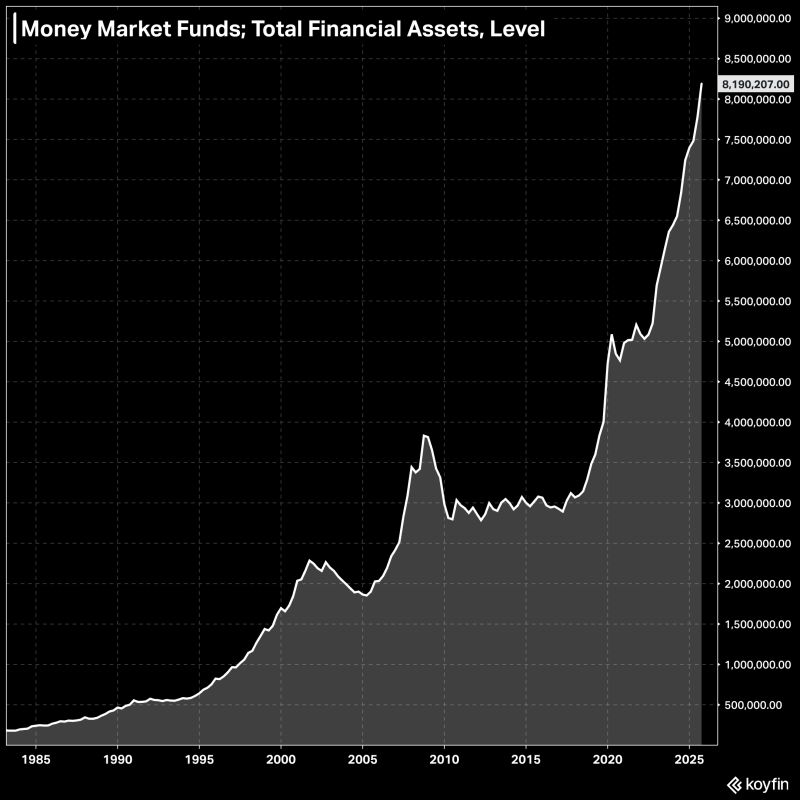

There is a record $8.19 trillion in money market funds right now.

Source: KoyfinCharts

WTI crude hits session highs, pushing 10Y yields to dangerous territory: 4.35% any second

Source: zerohedge

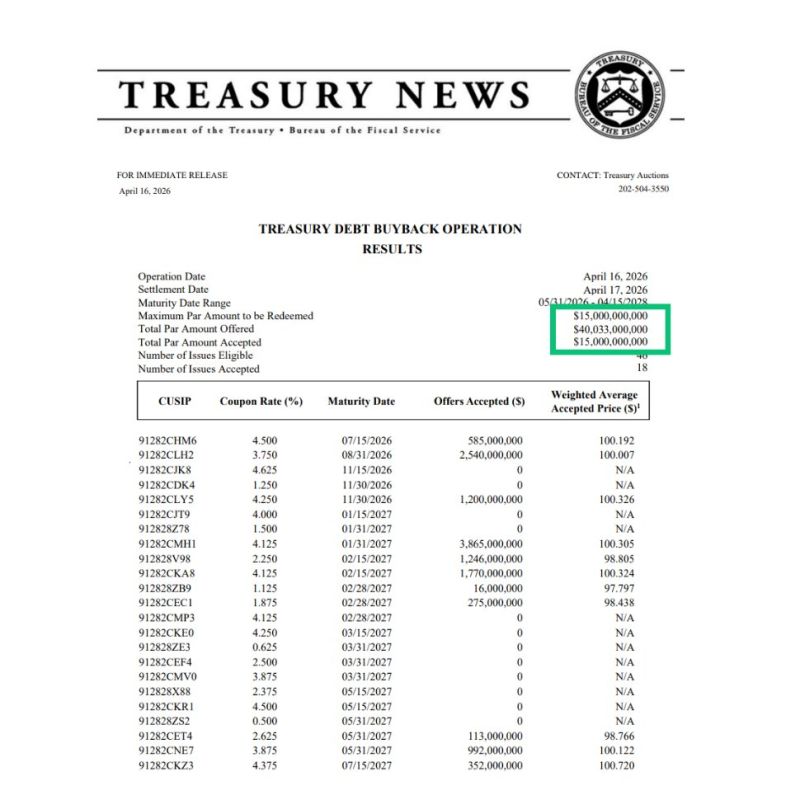

US Treasury just did the largest Treasury buyback in HISTORY.

Treasury bought back $15,000,000,000 of its own debt to improve liquidity. Source: Bull Theory

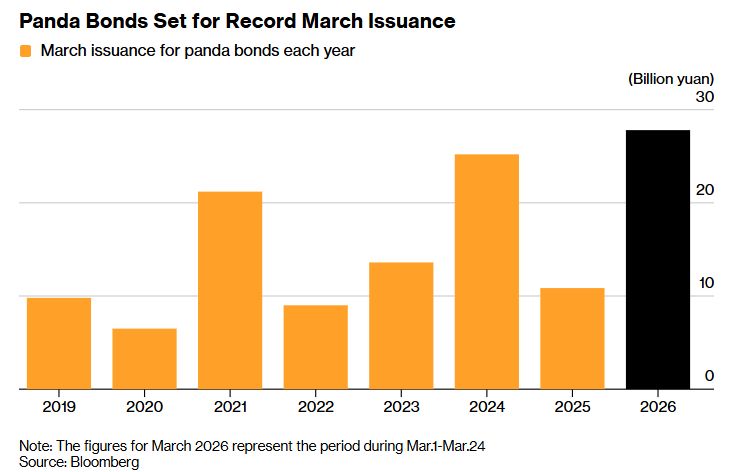

Forget US Treasuries, Chinese bonds are the new safe-haven trade

Since the start of the war, foreigners have: - Dumped $82B of Treasuries - Piled into panda bonds And this has nothing to do with China paying higher yields… - US 10-year yield: 4.4% - China 10-year yield: 1.8% In the midst of the biggest energy crisis, foreigners are choosing panda bonds over USTs. Source: Bloomberg, Lukas Ekwueme