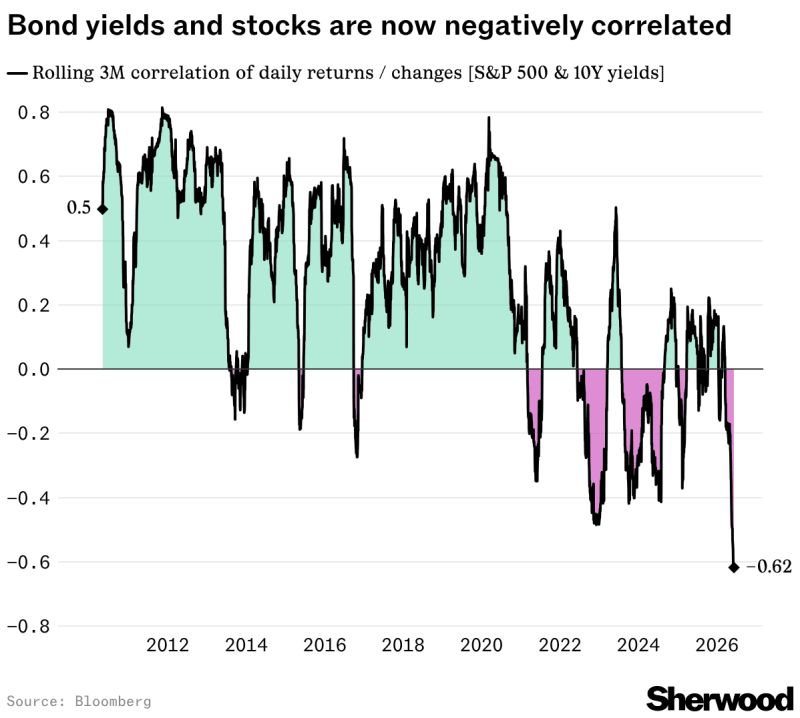

"The relationship between what the US government's debt is doing and stock prices has flipped in a big way. In fact, this is the most extreme yields-stocks relationship this entire market cycle."

Source: Daily Chartbook

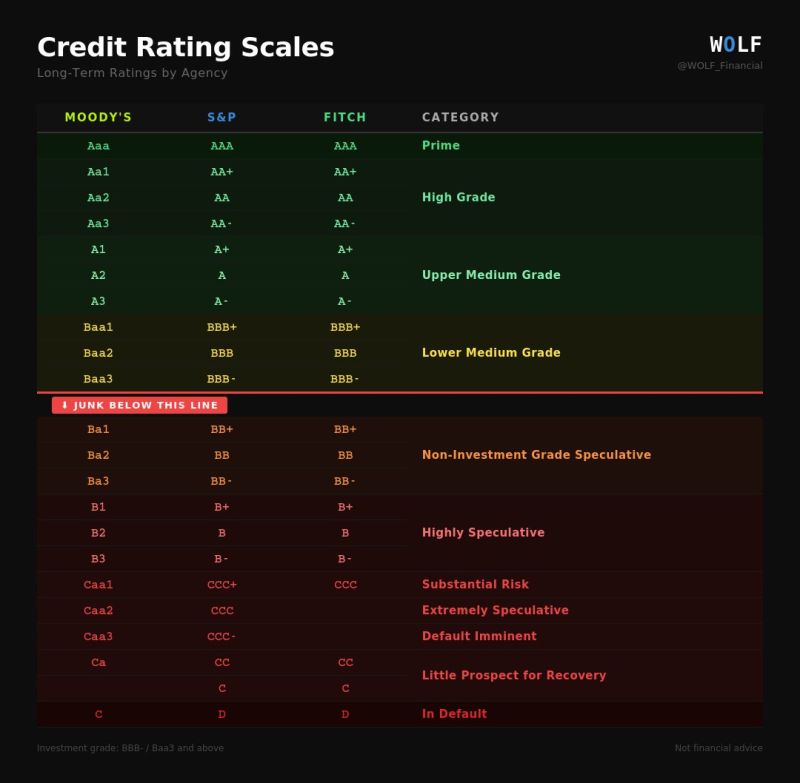

JUST IN: SPACEX HAS REPORTEDLY LINED UP INVESTMENT-GRADE CREDIT RATINGS FROM ALL THREE MAJOR AGENCIES

Per Bloomberg, citing sources: - Moody's, Fitch, and S&P Global all have SpaceX at investment grade - The ratings are reportedly being communicated privately ahead of Friday's $SPCX IPO debut - All three agencies publicly say they have not issued ratings The backing: - Google $GOOGL cloud services deal: $30B through mid-2029 - Anthropic compute deal: ~$45B over the next 3 years - Combined contracted revenue: $75B The Q1 financials: - Revenue: $4.69B (vs $4B a year earlier) - Net loss: $4.28B (vs $528M loss a year earlier) CreditSights expects SpaceX to issue investment-grade debt shortly after the IPO. The company has a $20B bridge loan due September 2027. Per CreditSights' Zachary Griffiths: "Negative earnings are not typically associated with an investment-grade company, but nothing about this is typical." Source: Evan, IPO Newsroom

Oil falls. Yields rise. Something has shifted

Oil down 15% in three weeks. The two-year yield up 15bps last week to 4.15% - its highest since early 2025. For the first time in months, US macro is back in the driving seat. Source: Jonny Matthews | SuperMacro

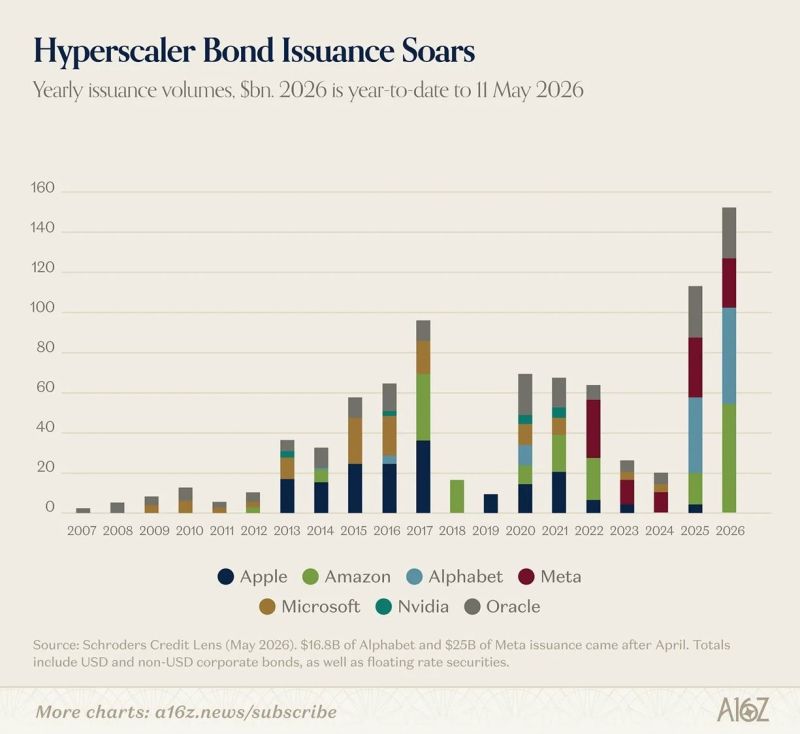

Breaking: Hyperscaler Bond Issuance Soars

In 4+ months in 2026 it is already more than in 2025, and several times more than the average of previous years. Their Free Cash Flow is dropping to 0. -> They must sell stocks, or slow down AI CAPEX. Source: BraVoCycles Newsletter

When rates start to matter... NASDAQ versus inverse US 10-year yields remains one of the biggest macro dislocation charts out there.

Let's keep in mind that bond volatility is exploding higher JUST AS hyperscalers enter the most capital-intensive spending cycle in modern tech history. Source: The Market Ear

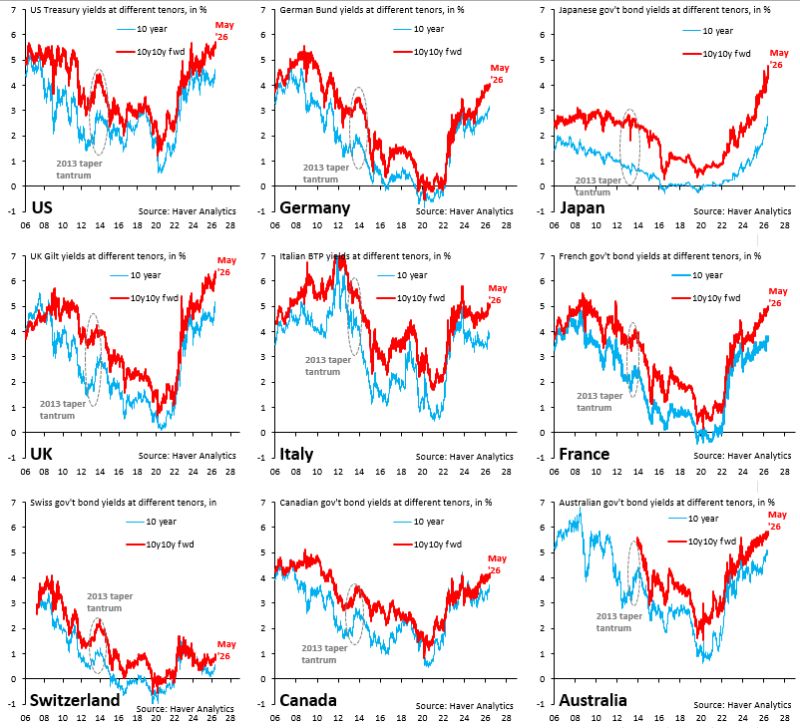

We've officially reached the "brutal" stage in the global bond market sell-off. The 10y10y forward yield (red) is making new highs all over the place.

Japan's 10y10y forward has risen 30 basis points in just a few days. Even Swiss 10y10y forward is rising. Source: Robin Brooks

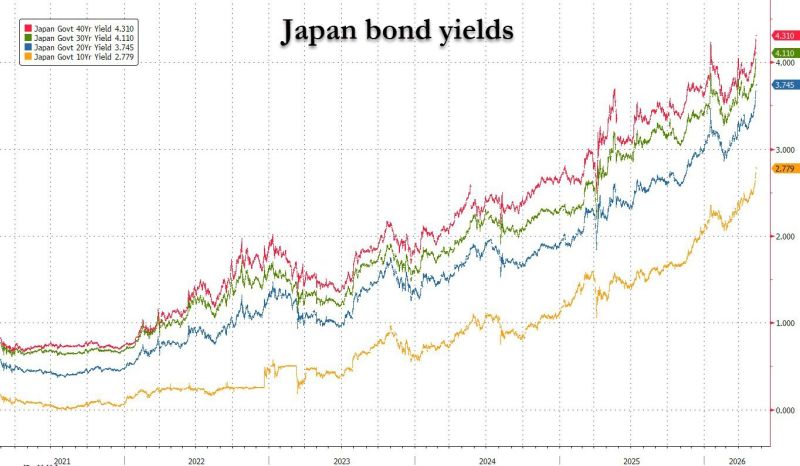

Another day, another new high for JGBs yields... Countdown to more BOJ QE as JGBs go bidless.

Source: zerohedge

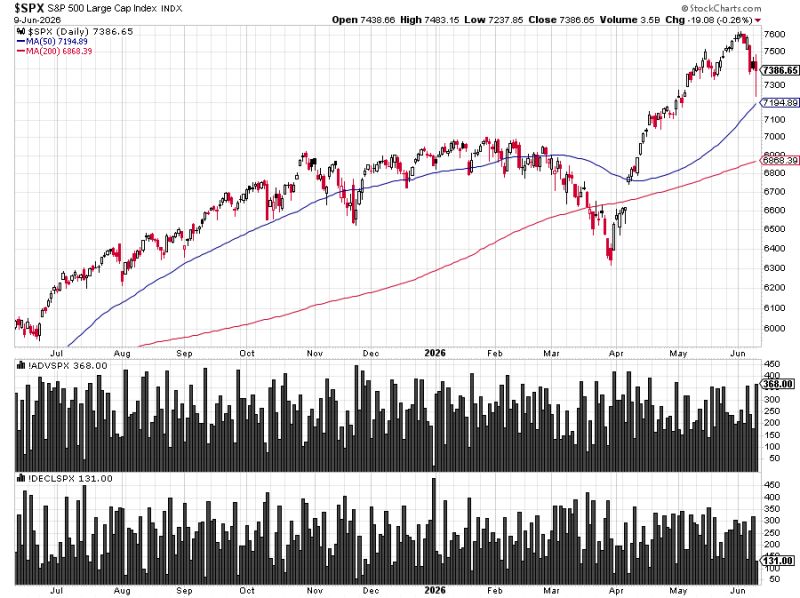

U.S. TREASURY YIELDS ARE HITTING KEY LEVELS

While the S&P 500 just hit a fresh record high of 7,501, the bond market is pricing in higher interest rates for longer. The 30 year yield is at 5.085%. The 20 year is at 5.092%. The 10 year is at 4.538%. Every maturity is rising at the same time. Stocks are at all time highs because the AI boom is driving earnings and the market is pricing in years of continued growth. Bond yields do not care about AI. They care about a $2 trillion annual deficit, oil at $100, persistent inflation and a government borrowing more money every single day to fund a war. Can the equity markets bull run if bond yields keep rising? What's your take? Source: Bull Theory