Bond vol matters

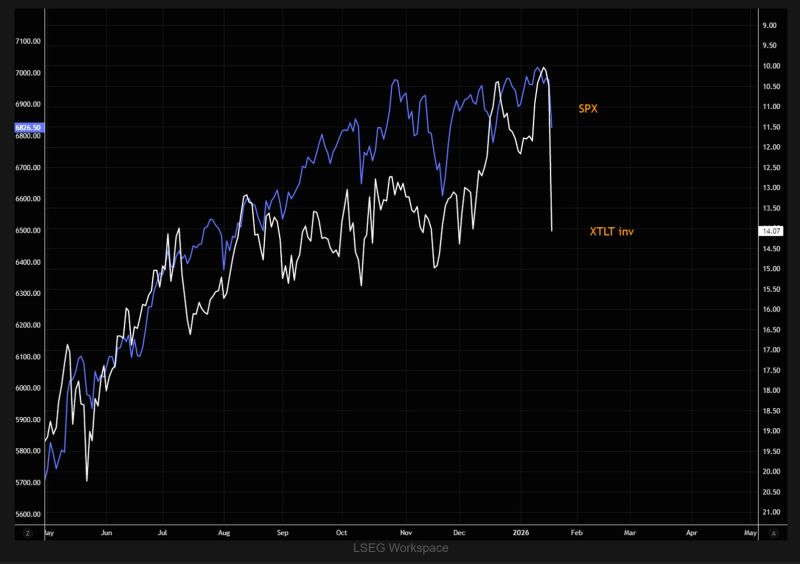

SPX vs VXTLT (inverted) needs little commenting. Source: TME

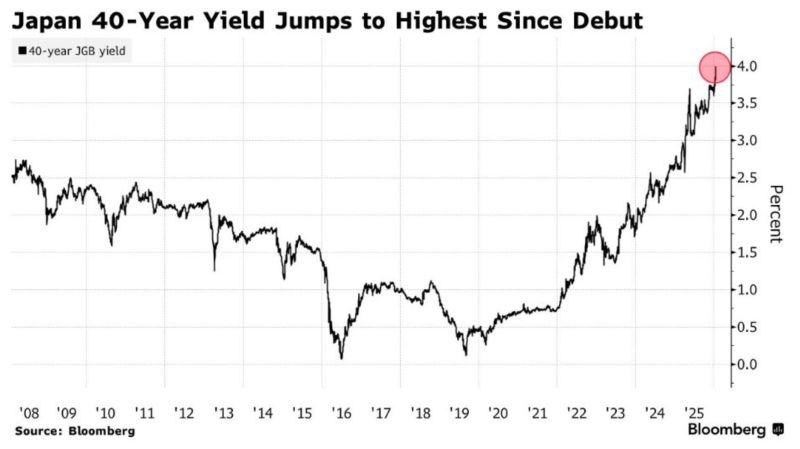

Japan's 40-year bond just hit 4% for the first time ever

Source: Joe Weisenthal @TheStalwart

U.S. Dollar Index $DXY plunging below its 200-day moving average

Source: Barchart

$7.8 Trillion is now sitting in Money Market Funds, a new all-time high

Source: Barchart

The Correlation Between Gold Prices and Japanese Bond Yields (2013–2025)

Gold (in organe) and 10-year JGB yields (in blue). Japan was always the endgame Source: www.zerohedge.com

U.S. Companies issued $95 Billion worth of bonds during the first week of the year, the highest weekly volume since Covid

Source: Barchart

Japan’s 30y govt bond yield jumped 10bps to 3.50%, its highest level since at least the 1990s.

The move comes amid growing speculation that PM Sanae Takaichi may dissolve parliament as early as next month, following reports in local media. Source: Bloomberg, HolgerZ

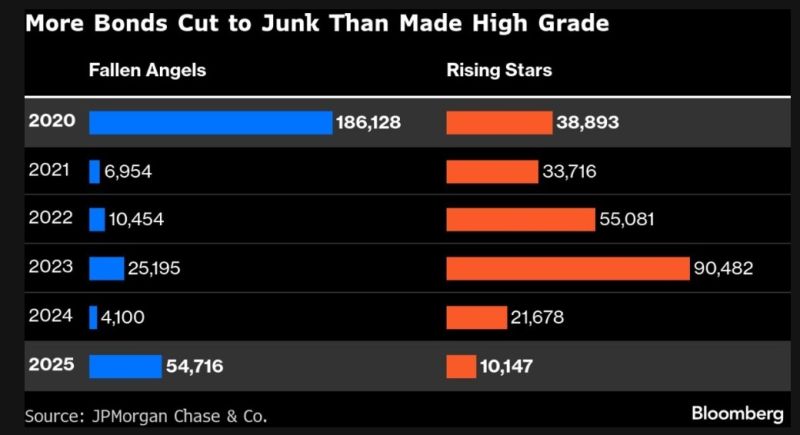

More Bonds Are Teetering on the Brink of Junk

JPMorgan doesn’t anticipate market turmoil anytime soon. Demand from investors is still strong, and earnings will probably be relatively strong in the coming weeks, leaving spreads relatively rangebound. But there are still risks in credit. About $55 billion of US corporate bonds migrated from investment-grade to junk status in 2025, becoming “fallen angels,” according to JPMorgan. That far exceeds last year’s $10 billion of “rising stars,” or firms elevated to high-grade. And the trend is set to continue, the strategists say. Source: Bloomberg, Tracy Shuchart (𝒞𝒽𝒾 ) @chigrl