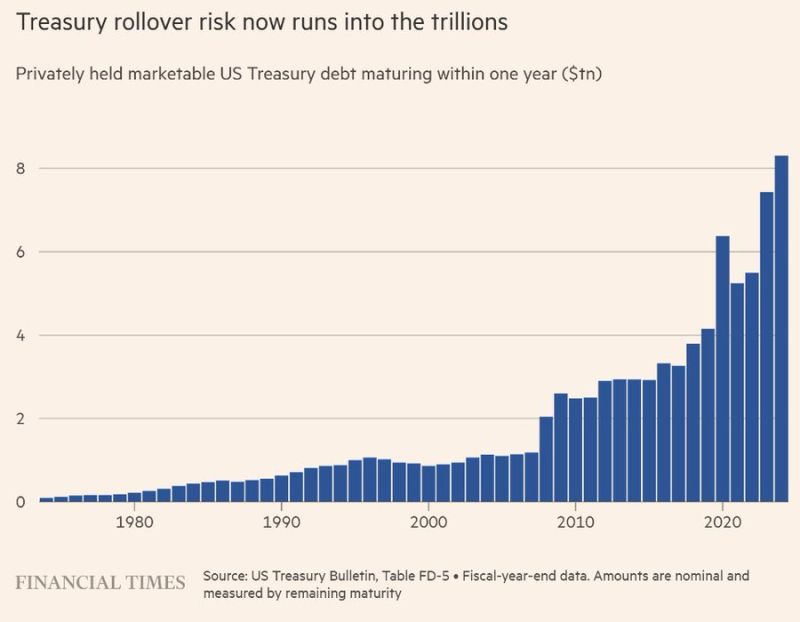

The US can't afford much higher interest rates.

Here's why: Around $8 trillion of US Treasuries must be refinanced over the next 12 months. The average coupon on that debt is roughly 3.3%. The 2-year Treasury yield is now around 4.3%. Refinancing $8 trillion at today's rates would add roughly $80 billion in annual interest costs before accounting for the financing needs of an ongoing $2 trillion annual deficit. This is why today's environment is fundamentally different from the Volcker era. In the early 1980s, inflation had already eroded the real value of government debt, helping push US debt-to-GDP down from roughly 120% after WWII to around 30%. That gave policymakers room to raise rates aggressively. Today, US debt is back near 120% of GDP. The sequence matters: inflate the debt away first, then raise rates to bring inflation under control. Doing it in reverse risks making the debt burden even harder to sustain. Source: Lukas Ekwueme, FT

Fed will deliver surprise rate hike this week, says Citadel

Source: Barchart

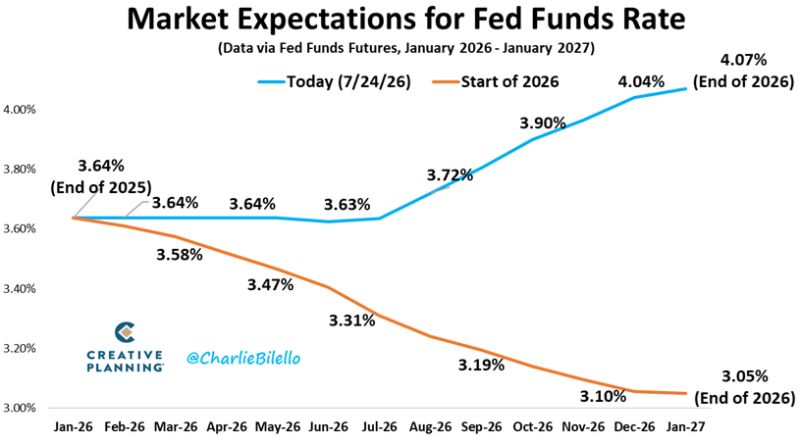

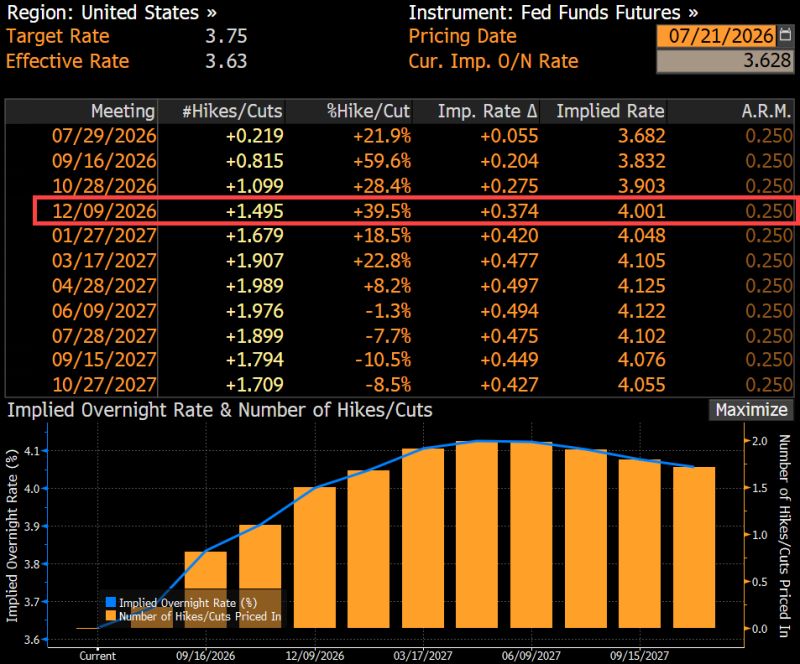

At the start of the year, the bond market was pricing in 2 Fed rate CUTS.

Today it's pricing in 1 to 2 Fed rate HIKES. That's a 1% swing in expectations. Source: Charlie Bilello

Stephen Warsh can sound like Volcker. The US fiscal position means he can't easily govern like Volcker.

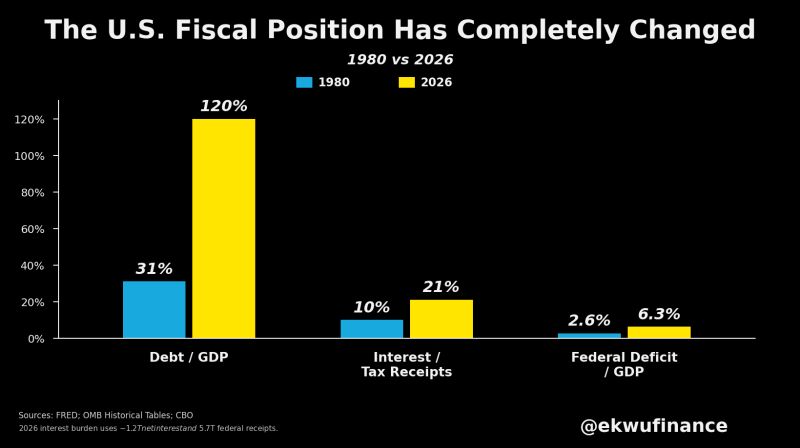

The backdrop has completely changed: • Debt-to-GDP: 31% in 1980 → ~120% today • Interest costs: 10% → 21% of federal tax receipts • Budget deficit: 2.6% → 6.3% of GDP That leaves the Fed facing a much tougher trade-off than it did in the early 1980s. Raise rates aggressively to crush inflation, and you risk destabilising the Treasury market and sharply increasing government financing costs. Prioritise financial stability instead, and inflation remains higher for longer, putting continued pressure on the US dollar. The Volcker playbook was built for a very different fiscal world. Today's debt burden makes every rate decision far more consequential. Source: Lukas Ekwueme @ekwufinance

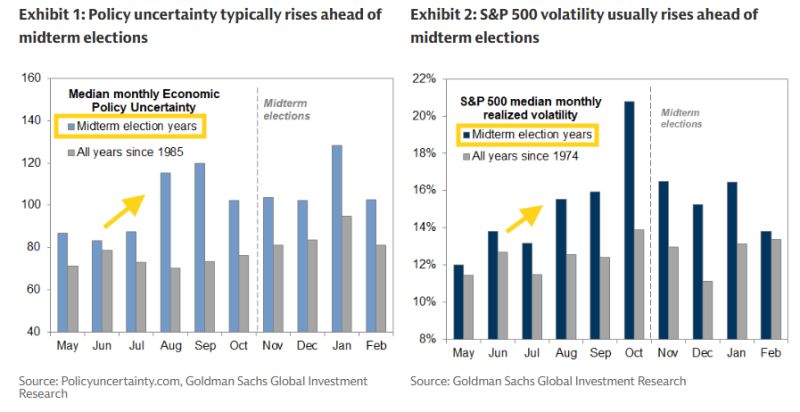

Goldman: With the 2026 midterms three months away, investor focus is likely to turn increasingly to elections in coming weeks. Midterm elections will take place this year on November 3.

During the last few decades, economic policy uncertainty and equity market volatility have typically begun to rise in the late summer ahead of midterm elections. Our economists have found the same pattern after adjusting for the economic cycle as measured by the unemployment rate. Source: Goldman Sachs, Neil Sethi on X

The futures market is now pricing 1.5 Fed rate hikes by year-end

Source: Hedgeye, Bloomberg

In Germany, factory-gate inflation offers a hopeful signal for consumers

Producer prices slowed to 1.8% YoY in June from 2.2% in May, below the June CPI of 2.3%, and fell 0.3% MoM. Crucially, German producers charged 2.2% less for consumer goods YoY, led by food prices down 4.5% YoY; a positive signal for retail inflation. Source: HolgerZ, Bloomberg

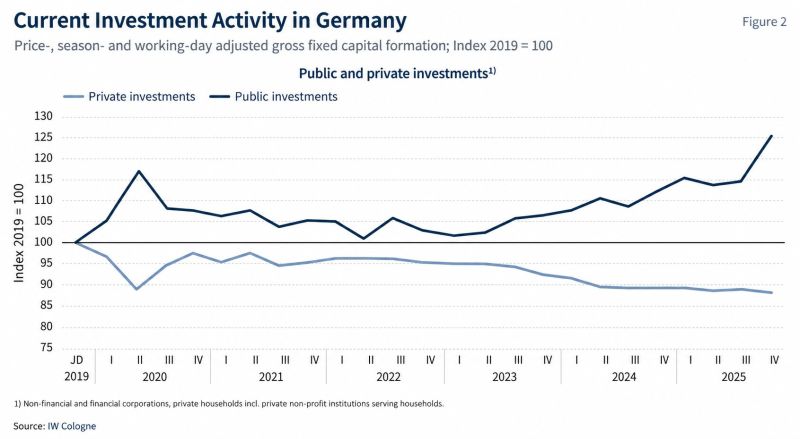

In Germany, the state is investing, but companies still aren’t.

Public investment has surged to 125% of its 2019 level, while private investment has fallen to 88%. One year after “Made for Germany,” corporate spending is rising, but far too slowly to hit the €631bn target by 2028. Germany is becoming more expensive without becoming more attractive. (HT CEO Table) Source: HolgerZ