America isn't retiring anymore. It's working longer than ever.

One in three Americans aged 55 and older is still working or looking for work, and that share has been climbing for nearly 40 years. The biggest change is among older workers: • Ages 65–69: participation has nearly doubled since the late 1980s, now above 30%. • Ages 70–74: from under 10% to almost 19%. • Ages 75+: participation has doubled to roughly 8%. The numbers are striking. Nearly 11.9 million Americans aged 65+ were employed last year, more than double the level of three decades ago. Between 2015 and 2024, the 65+ workforce expanded 33%, while the overall labor force grew by less than 9%. Longer life expectancy is part of the story. But so are disappearing pensions, rising living costs, and Social Security benefits that no longer stretch as far. Retirement is increasingly becoming a luxury rather than the default. Source: hedgeye

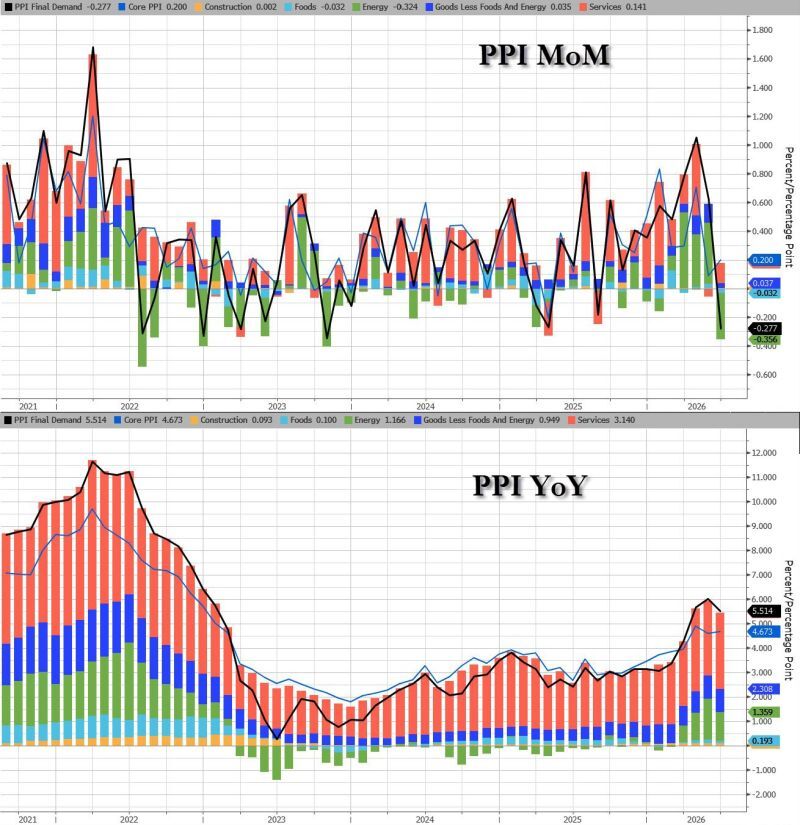

In case you missed it... Just like Tuesday’s CPI, US PPI inflation came in significantly softer than consensus forecasts, across the board.

Headline PPI moderated to 5.5% year-over-year (vs. 6.2% expected), driven by a -0.3% monthly decline (vs. 0.0% expected) The core rate fell to 4.7% yoy (on a 0.2% monthly increase). These much better-than-expected figures are set to further temper market expectations for upcoming interest rate hikes. Source: zerohedge

One-year inflation swaps fall below 2% for the first time since 2024 !!!

Source: Hedgeye

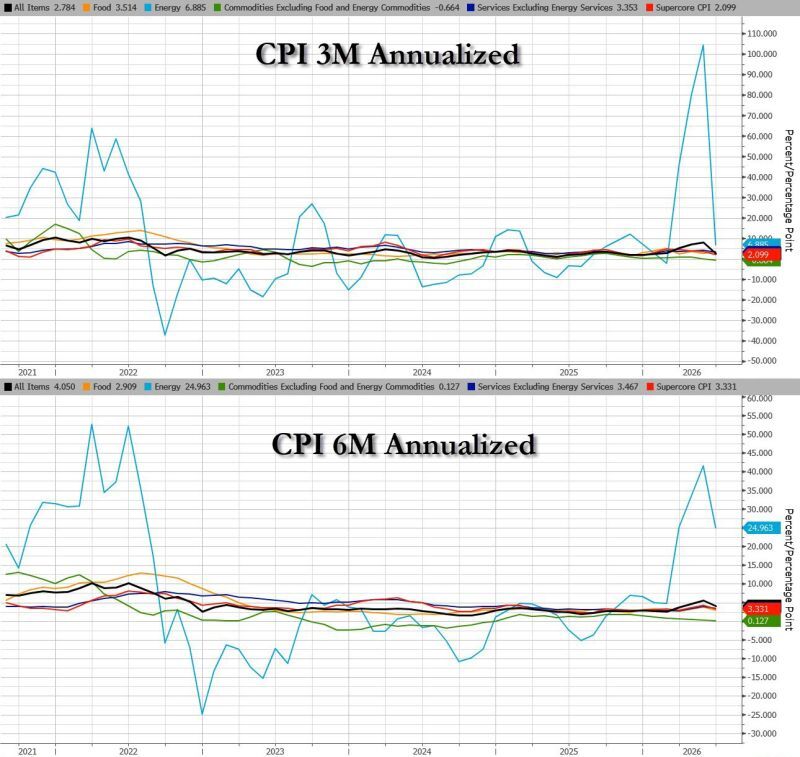

3M annualized US Headline CPI drops from 8.2% to 2.8%.

Source: zerohedge

Very cool prices in the June CPI were across the board.

US Headline inflation (CPI) comes in lower than expected, at 3.5% vs expected 3.8%. This is the biggest drop in MoM headline CPI (-0.4%) since covid crash. It is also much lower than expected (-0.1%). Core CPI is also the lowest since covid at +2.6% yoy (vs. +2.8% expected). The core CPI *declined* on a MoM basis, falling -0.02%. This is the first MoM drop since May 2020. Source: Bloomberg

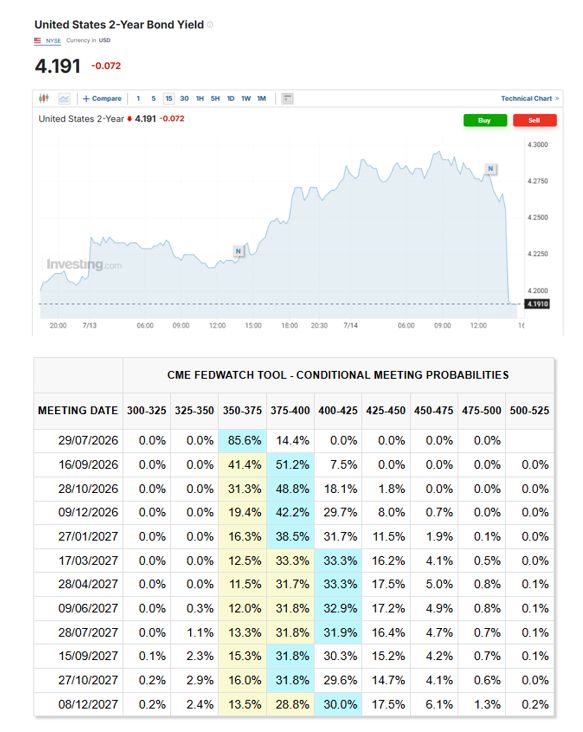

US 2 year yield is tumbling -7 basis points as US CPI number came in cooler than expected.

Odds of a July rate hike are now 14% (vs. 45% this morning). Source: www.investing.com, CME Fed Watch tool

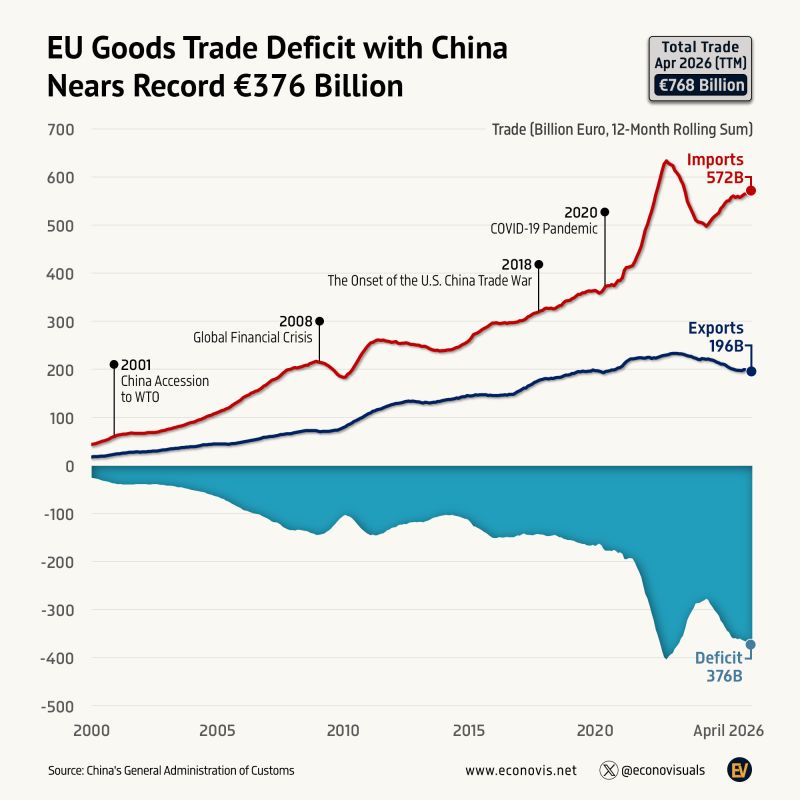

EU Goods Trade Deficit with China Nears Record €376 Billion

The European Union's goods trade with China totaled €768 billion in the twelve months ending April 2026, with €572 billion in imports and €196 billion in exports. The resulting €376 billion trade deficit was the second largest on record, underscoring Europe's continued dependence on Chinese manufactured goods despite efforts to diversify supply chains and reduce strategic vulnerabilities. Source: Econovis

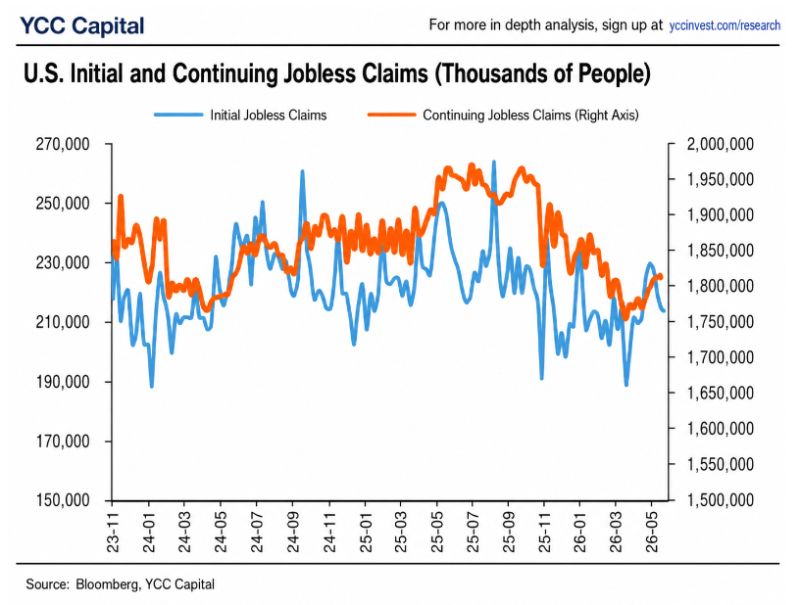

🚨 The labor market still refuses to crack.*

Initial jobless claims remain stuck in a remarkably stable range of 200,000–230,000, while continuing claims are hovering around 1.8 million. For more than two years, recession fears have dominated headlines. Yet the one indicator that typically flashes red before a downturn still isn't doing it. Yes, workers who lose their jobs are taking longer to find new ones, pushing continuing claims higher. But companies are not laying off employees at the pace you would expect ahead of a recession. That's the key distinction. 📌 The labor market is cooling, not collapsing. For the Federal Reserve, that's an important signal. As long as layoffs remain contained, policymakers can stay focused on inflation instead of rushing to support the economy. Jobless claims remain one of the strongest pieces of evidence that the U.S. economy is slowing—but not yet heading into an imminent recession. Source: YCC Macro