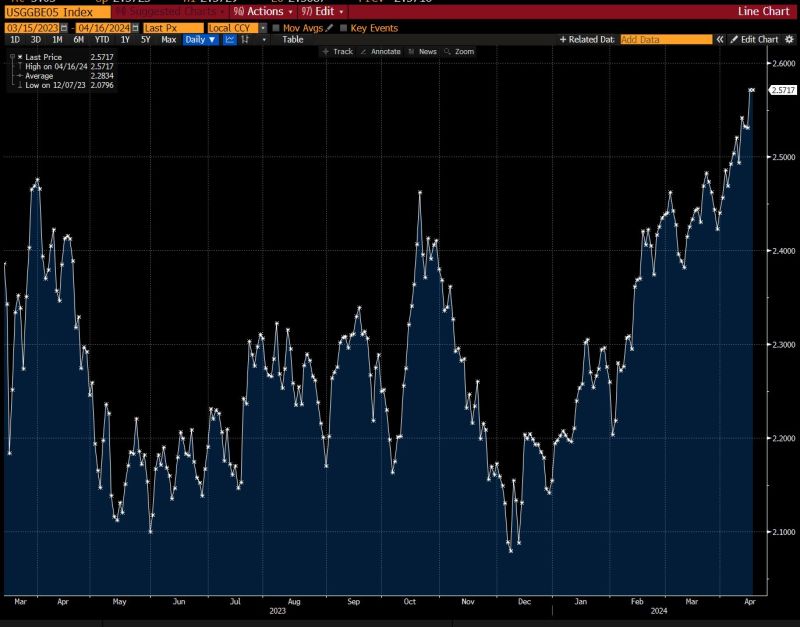

Longer-term inflation expectations are rising again.

The market's implied rate of inflation over the next five years has risen to the highest level in more than a year, at 2.6%, according to breakeven rates. Source: Bloomberg, Lisa Abramowitz

According to Alfonso Peccatiello, a $1 trillion worth liquidity wave is about to be unleashed on the US economy!

He is not talking about Powell or the Fed. He is talking about Treasury Secretary Yellen unleashing a large sum of stimulus further boosting the US economy right before elections! How? By almost emptying a $1 trillion+ Treasury General Account!

China’s economy in the first quarter grew faster than expected, official data released Tuesday by China’s National Bureau of Statistics showed.

Gross domestic product in the January to March period grew 5.3% compared to a year ago, faster than the 4.6% growth expected by economists polled by Reuters, and compared to the 5.2% expansion in the fourth quarter of 2023. On a quarter-on-quarter basis, China’s GDP grew 1.6% in the first quarter, compared to a Reuters poll expectations of 1.4% and a revised fourth quarter expansion of 1.2%. Beijing has set a 2024 growth target of around 5%. https://lnkd.in/eNZgs7zp Source: CNBC

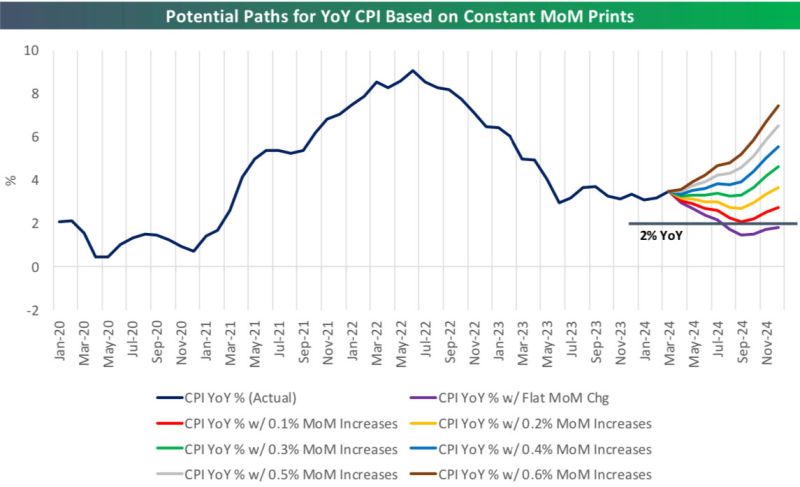

Getting to 2% YoY CPI by the end of 2024 means we need to average monthly CPI prints of 0.1% or less from here.

Source: Bespoke

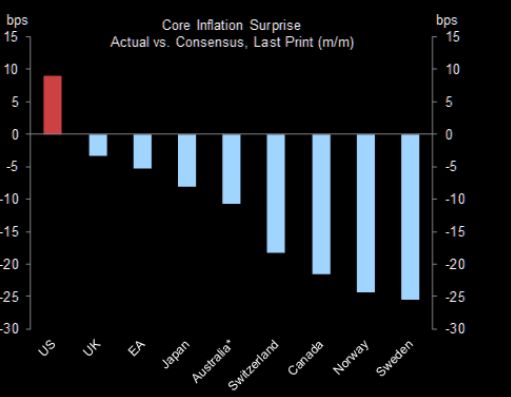

Did you know that the US is the only G10 economy where the latest core inflation print surprised to the upside?

Source: Goldman Sachs, TME

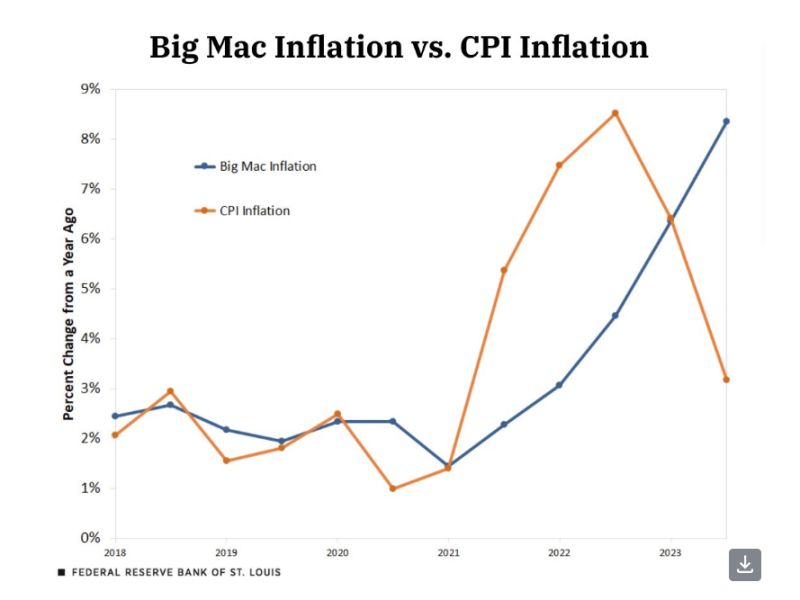

Big Mac inflation vs. CPI... which one is right?

While many investors are more confused than ever looking at "CPI", whatever that is, the real inflation gauge is giving off a serious warning. Source: J-C Parets

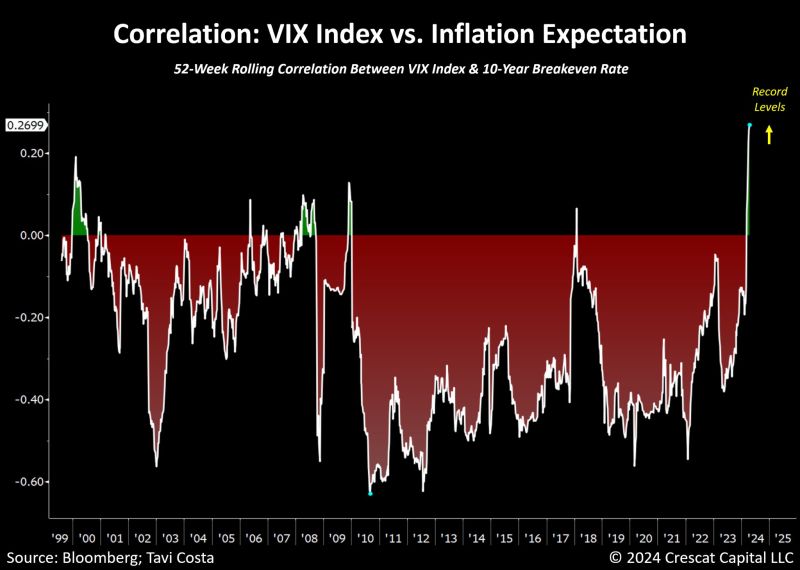

The correlation between equity market volatility and inflation expectations is at the highest level we've seen in decades.

Although the chart below doesn't extend as far back, a similar phenomenon occurred in 1973-1974 as markets faced difficulties whenever inflation reaccelerated. This is especially pertinent now, with energy prices, agricultural commodities, precious metals, copper, global freight costs, and other inflation indicators showing significant resurgence. Source: Tavi Costa, Crescat Capital, Bloomberg

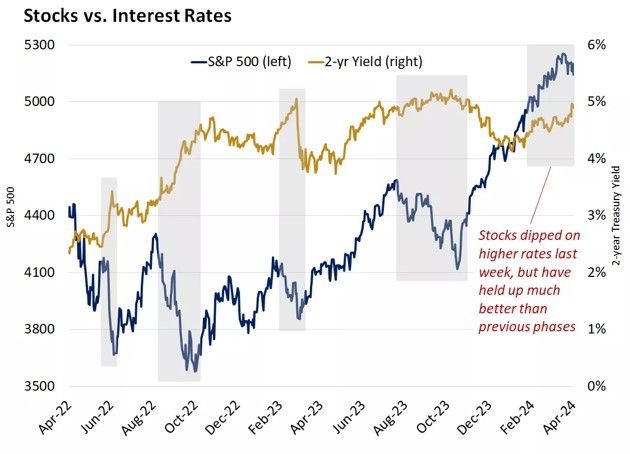

Yes, this week was painful for stocks.

But putting things into perspective, equities have been more resilient to higher rates recently versus previous periods of rising rates. Source: Edward Jones