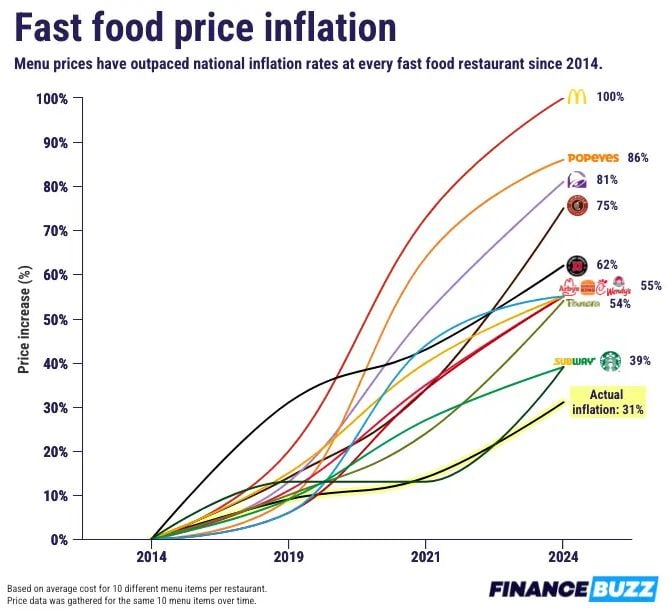

Price increases over last decade...

McDonald's: +100% Popeyes: +86% Taco Bell: +81% Chipotle: +75% Jimmy John's: +62% Arby's: +55% Burger King: +55% Chick-fil-A: +55% Wendy's: +55% Panera: +54% Subway: +39% Starbucks: +39% US Government Reported Inflation (CPI): +31% Source: Charlie Bilello

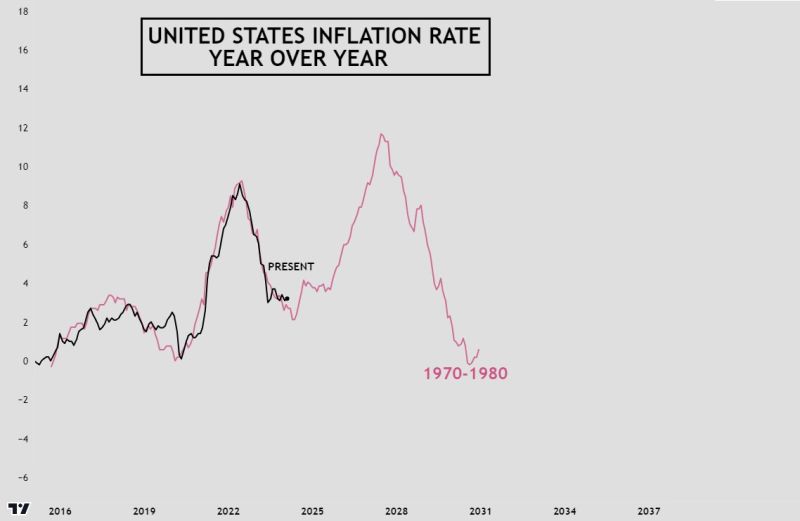

In our 2024 "10 surprises 2024" (see link below), we had surprise #6: "What if inflation rises again?"

The idea here was that inflation could experience a second wave similar to that seen in the 70s and 80s. And this would lead inflationary assets (e.g., cyclical stocks) to catch up with deflationary assets (e.g. technology stocks). Below an uopdate chart (courtesy of HZ on X) taking into account yesterday's US cpi print... Has a second inflationary wave begun? https://lnkd.in/eDPyFa_9

The Federal Reserve's next move might be to raise interest rates warns Former Treasury Secretary Larry Summers.

Source: Barchart

JP Morgan and BlackRock were given insider information about Wednesday's inflation numbers by the Bureau of Labor Statistics 🚨

Source: Barchart

US inflation continues to rise, with no decrease in sight according to Zerohedge.

Since January 2021, inflation has not fallen in a single month, leading to an overall increase of 19% in less than four years. Additionally, the US has not seen a year-over-year inflation print below 3% in 36 consecutive months. The Fed's 2% target has also been surpassed for 37 straight months. This compounding inflation may have long-term impacts on the economy. Source: The Bobeissi Lezzer

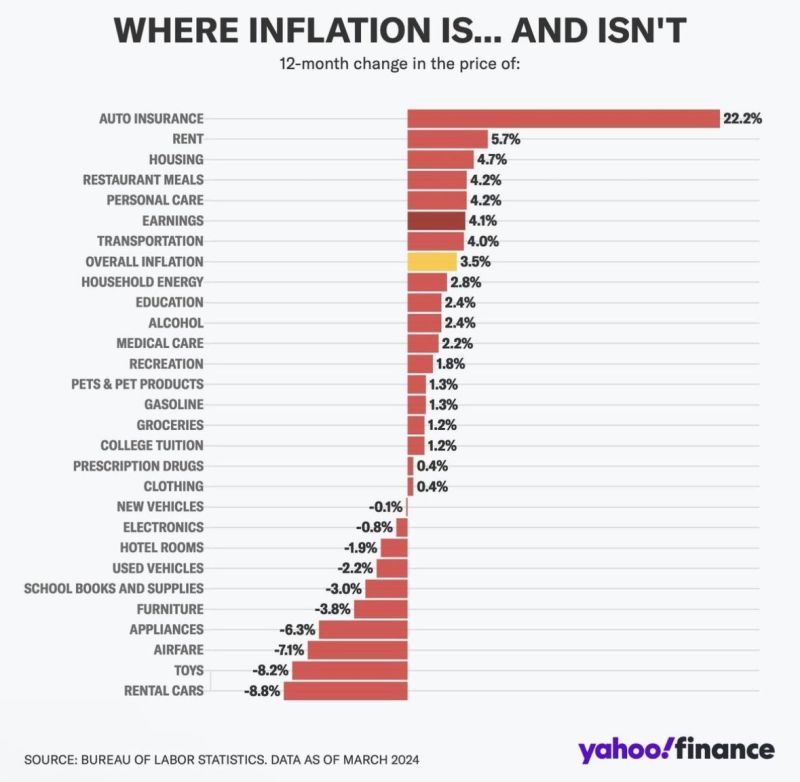

Where US inflation is and where it isn’t 👀

Source: Yahoo Finance, Evan

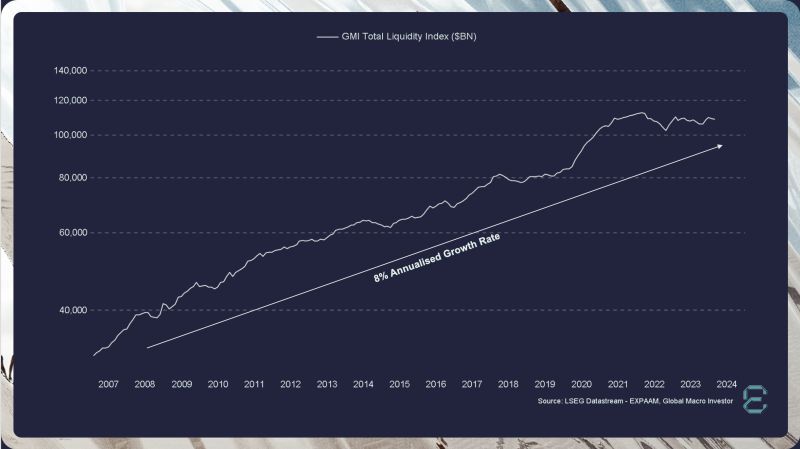

Raoul Pal - Global Macro Investors (GMI) has shared this chart on X showing Global liquidity growing at a CAGR of 8%.

His view: "While everyone is worried about 3.5% inflation, the real issue is the ongoing 8% per annum debasement of currency, on top of inflation. Your hurdle rate to break even is around 12%, which is the 10-year average returns of the S&P 500...just to keep your purchasing power". Key takeaway: if you want to protect your purchasing power in a global monetary debasement, you have 3 choices: 1/ spend; 2/ invest into risk assets; 3/ invest into store of values

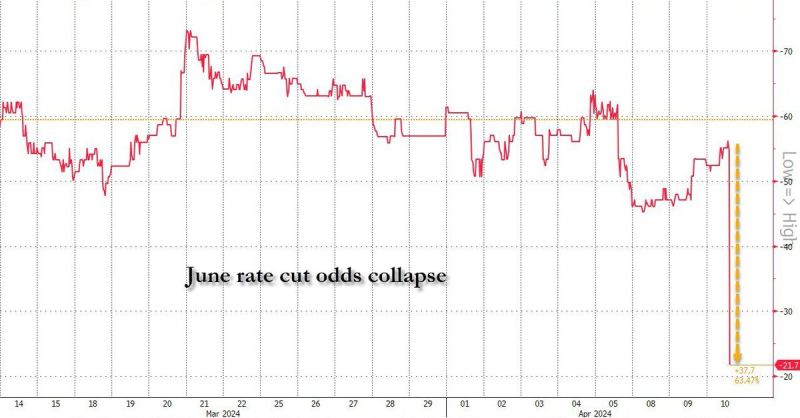

BREAKING: Interest rate futures are now pricing in just 2 interest rate cuts for the entire 2024.

This is the first time that markets are pricing-in LESS rate cuts than Fed guidance. Just 4 months ago, markets saw 6-8 rate cuts in 2024 with cuts beginning in March. Odds of a rate cut in June are down from ~60% before the CPI report to ~22% now. Source: The Kobeissi Letter, www.zerohedge.com