The Great American Oil Paradox

The U.S. is executing a unique energy “double-play,” exporting massive amounts of light, sweet shale crude while still importing heavy, sour oil to match its legacy refinery infrastructure. This paradox being both a top exporter and importer makes the country the central hinge of the global oil market. Far from a weakness, this interdependence gives the U.S. leverage, allowing it to balance supply and influence prices worldwide as we head into 2026. Source: Jack Prandelli

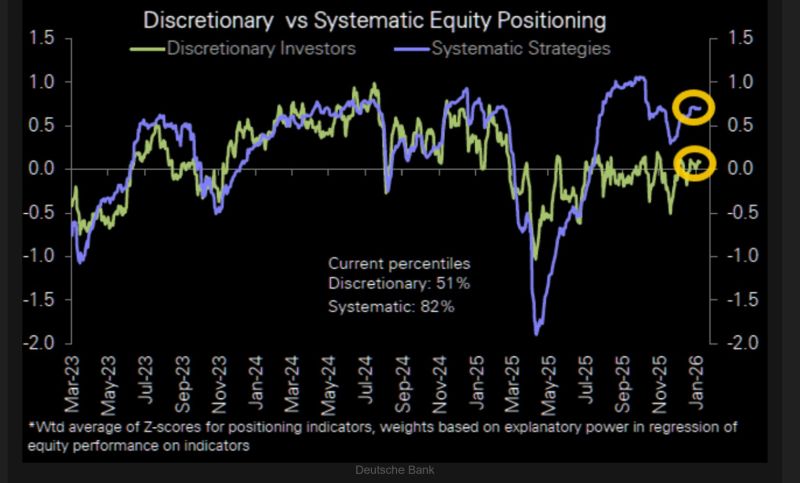

Believe it or not, investor's positioning on equities is still not over-extended.

Deutsche Bank: "Notably, while investor sentiment has risen meaningfully over the last 6 weeks, positioning in our reading has not yet followed, with discretionary investors are still holding cautiously near neutral (0.09sd, 51st percentile). Systematic strategy positioning though is higher (0.71sd, 82nd percentile)." Source: DB, TME

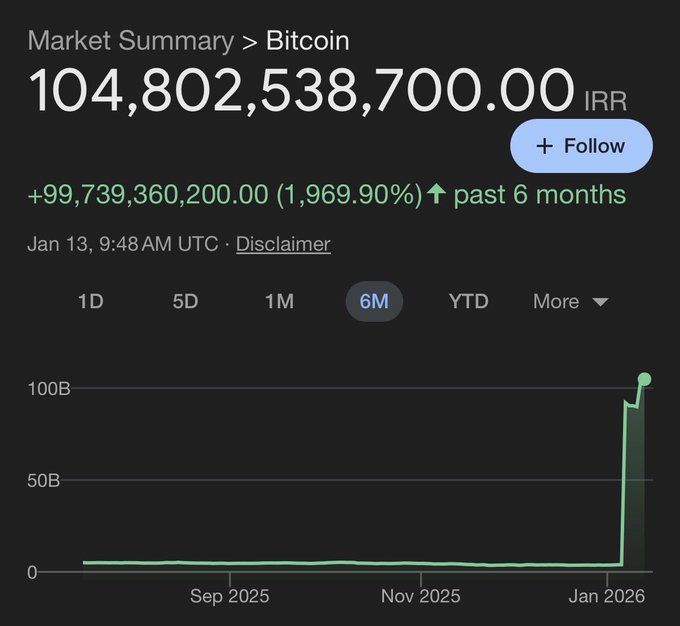

Bitcoin becomes King in Iran

As Iran’s currency collapses, Bitcoin is shifting from a theoretical hedge to a practical necessity. Hyperinflation in the rial is pushing citizens toward BTC as a store of value, while sanctions have made crypto an effective alternative to the traditional banking system. At the same time, Iran’s extremely cheap energy makes Bitcoin mining highly profitable, sustaining local supply that feeds sanction-bypassing channels. The combination of fiat collapse, sanctions, and energy arbitrage is driving a sharp surge in Bitcoin adoption and pricing relative to the rial. Source: Mario Nawfal

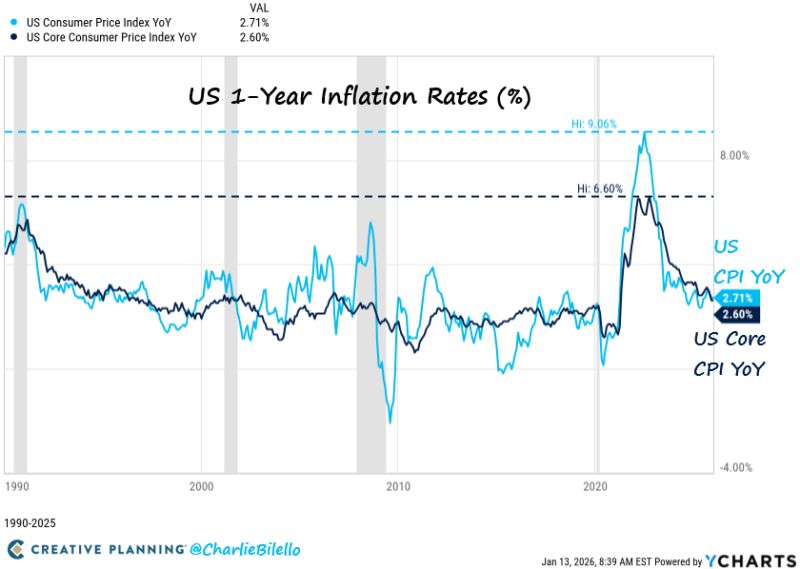

CPI Holds at 2.7% YoY as December Rebound Falls Short of Fears

The headline CPI print rose 0.3% MoM (vs +0.3% MoM exp) driving prices up 2.7% on a YoY basis (vs +2.7% YoY exp). Many expected a December pickup due to the unwinding of distortions from data-collection disruptions during the government shutdown, which amplified seasonal discounting in November. So the headline number is basically below most of “Whisper” numbers. Source: Charlie Bilello

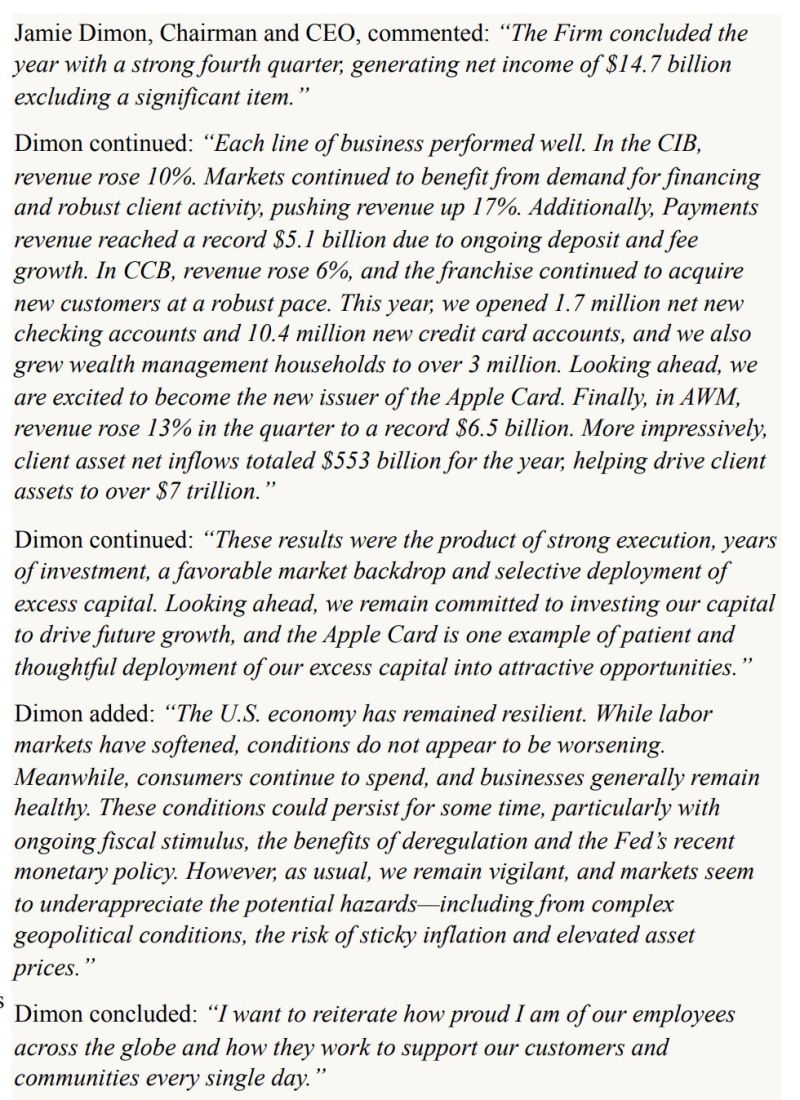

Jamie Dimon: U.S. Economy Remains Resilient Despite Softer Labor Markets

$JPM JP Morgan CEO Jamie Dimon: "The U.S. economy has remained resilient. While labor markets have softened, conditions do not appear to be worsening. Meanwhile, consumers continue to spend, and businesses generally remain healthy. These conditions could persist for some time..." Source: The Transcript

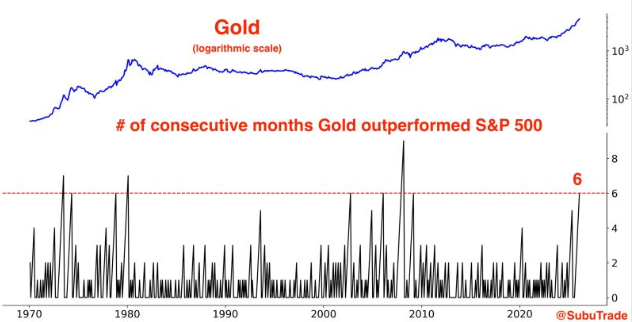

Gold has now outperformed the S&P 500 for 6 consecutive months, the longest streak since the Global Financial Crisis

Source: Barchart

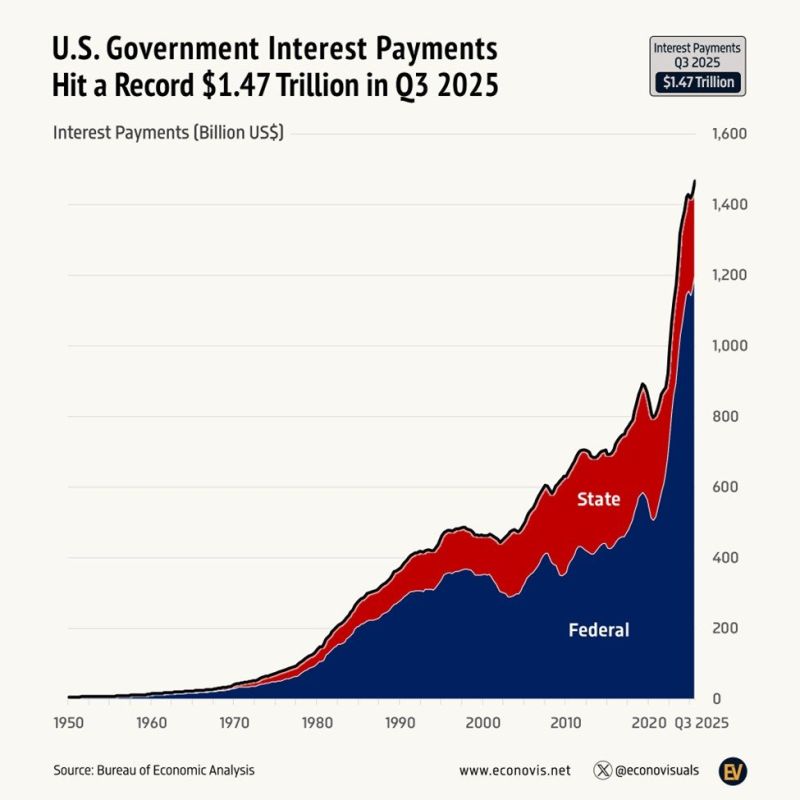

US government interest payments are now up to an annualized record of $1.47 trillion.

The Sovereignty Trap: By offshoring industry to China for higher margins, the West traded its independence for cheap labor; China now controls the minerals essential for Defense, EVs, and tech. Resource vs. Currency: The ability to print money is irrelevant if China refuses to sell the raw materials required for survival and industry. The Great Rebuild: To regain independence, Western nations are aggressively reshoring industry, stockpiling minerals, and rebuilding infrastructure. The Irony of Tech: Building the "New Economy" (Silicon Valley, AI, Green Tech) is impossible without massive amounts of "Old Economy" materials like copper, lithium, and steel. Source: Topdown charts, LSEG, Lukas Ekwueme @ekwufinance

CPI: 2.7% YoY vs. 2.7% expected Core CPI: 2.6% YoY vs. 2.7% expected

Core U.S. consumer prices rose less than predicted in December, reinforcing hopes that inflation is tempering as the Federal Reserve contemplates its next move on interest rates. The consumer price index, a broad measure of the costs for goods and services across the sprawling U.S. economy, posted an increase of 0.3% for the month, putting the headline all-items annual rate at 2.7%. Both were exactly in line with the Dow Jones consensus estimate. At the same time, core inflation, which excludes volatile food and energy prices, showed a 0.2% gain on a monthly basis and 2.6% annually. Both were 0.1 percentage point below expectations. Source: CNBC Peter Tuchman, @EinsteinoWallSt