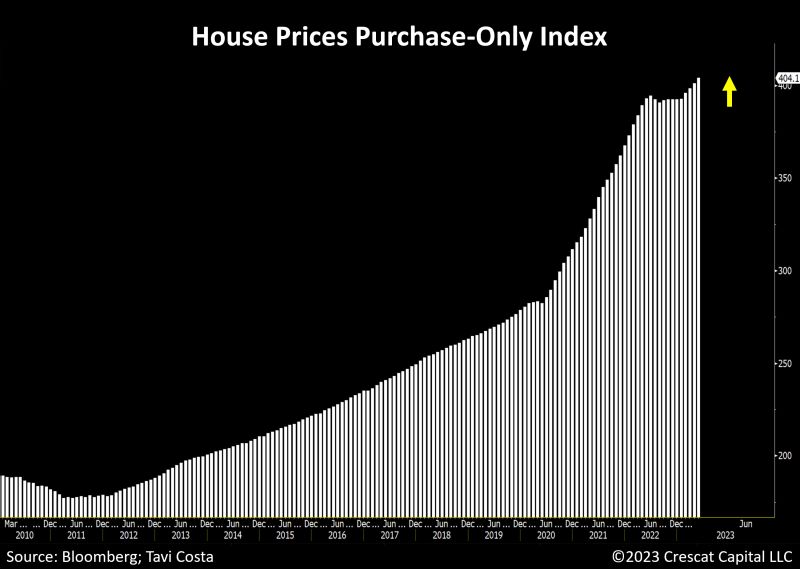

Looking at the recent sales transactions, house prices have accelerated significantly in the last 4 months to record levels, now growing at almost a 10% annualized rate

As a remainder, shelter costs / rents jave been putting upward pressure on core CPI and are expected to ease. Really? Source: Tavi Costa, Crescat Capital, Bloomberg

Soccerflation...Perks that Neymar Júnior will receive in Saudi Arabia:

• €100M-a-year salary • House with 25 bedrooms • 40x10 meter swimming pool and 3 saunas • 5 full-time staff for his house • Bentley Continental GT • Aston Martin DBX • Lamborghini Huracán • 24-hour driver • all bills for hotels, restaurants and various services during his OFF days will be sent to the club headquarters to be paid • Private plane at his disposal for his travels • €500,000 for each social media post that promotes Saudi Arabia Source: The world of Statistics

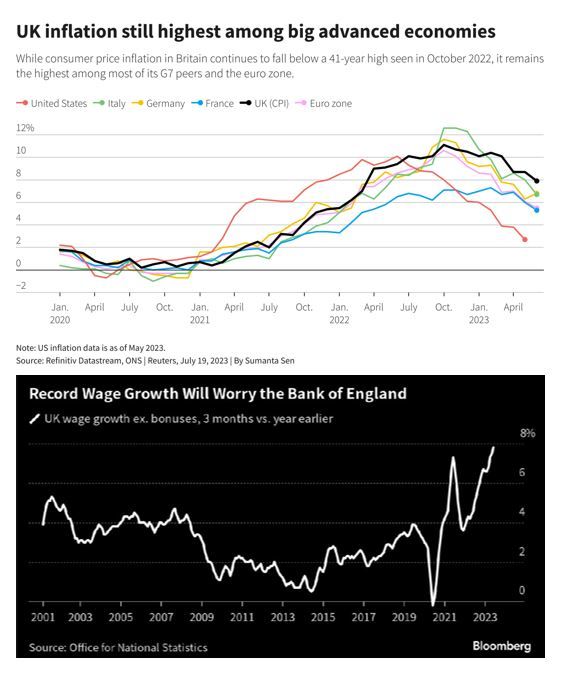

UK headline inflation cooled sharply in July to an annual 6.8%, but the core consumer price index remained unchanged, posing a potential headache for the Bank of England

The headline CPI reading was in line with a consensus forecast among economists polled by Reuters, and follows the cooler-than-expected 7.9% figure of June. Despite the decline, UK inflation is still the highest among "advanced" economies (see upper chart below). On a monthly basis, the headline CPI decreased by 0.4% versus a consensus forecast of -0.5%. However, core inflation — which excludes volatile energy, food, alcohol and tobacco prices — stayed 6.9%, unchanged from June and slightly above a consensus forecast of 6.8%.

European gas spikes on market jitters over LNG strike risk

European natural gas futures spiked for the second time in less than a week, with market tensions running high over the possibility of strikes in Australia that could severely tighten the global market.

Source: Bloomberg

Michael Burry is an outstanding contrarian investor and did exceptionally well during the 2006-2008 US housing crash

However, performance is not always repeatable and his next bets haven't paid off that well (at least the market views shared publicly - hedge fund long-term performance looks quite strong on a sharper ratio basis). Adam Khoo had a look at all of Michael Burry's recent predictions and he shared it with a chart on X. Here's a summary: In 2005, Predicted the collapse of the subprime mortgage market -> Housing market crashes in 2008, Global Financial Crisis. On Dec 2015, he predicted that the stock market would crash within the next few months. -> SPX +11% Next 12 months. On May 2017, he predicted a global financial meltdown-> SPX +19% Next 12 months. On Sept 2019, he predicted that the stock market would crash due to a bubble in index ETFs -> SPX +15% Next 12 months. Source: Adam Khoo Trader

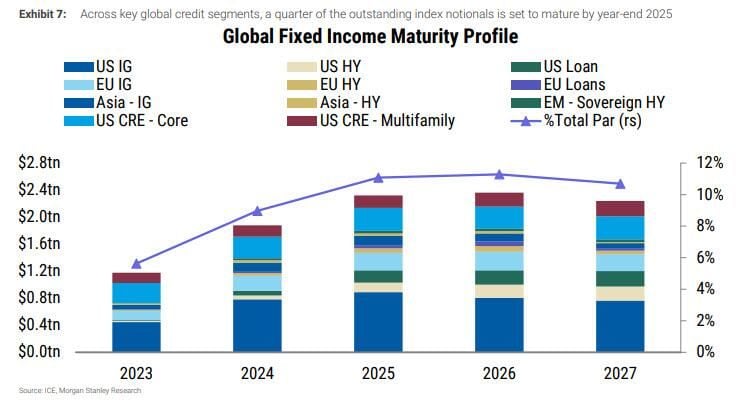

We are approaching quite a formidable global #debt maturity wall...

Source: Markets & Mayhem, Morgan Stanley

Japan GDP grew 6%, handily beating expectations on robust exports - but domestic demand disappoints

Japan Q2 GDP improves to 1.5% QoQ vs 0.8% expected and 0.1% prior, meaning Japan grows 6.0% on annualized basis, far more than expected (+2.9% yoy). However, some details of the report weren’t as impressive as the headline. As pointed out by analysts in CNBC report, nearly all of the increase in output was driven by a 1.8%-pts boost from net trade. That marked the second-largest contribution from net trade in the 28-year history of the current GDP series, with only the bounce back in exports from the first lockdown at the beginning of the pandemic providing a larger boost. Exports rebounded 3.2% from the previous quarter — largely driven by the spike in car shipments — while imports plunged 4.3% over the time period. Source: Bloomberg, HolgerZ, CNBC

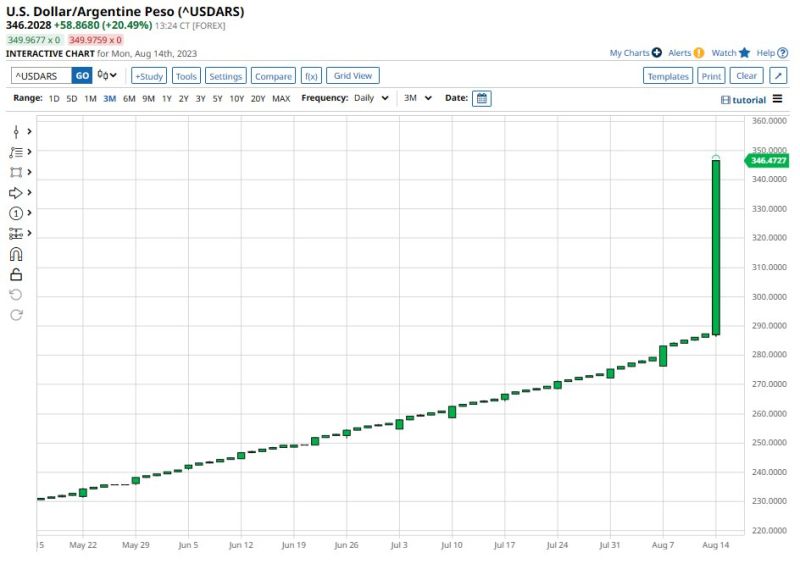

Argentine Peso having a rough day. An 18% devaluation to 350 pesos per dollar (chart) accompanied by a 21 percentage point hike in interest rates to 118% …

Source: Barchart