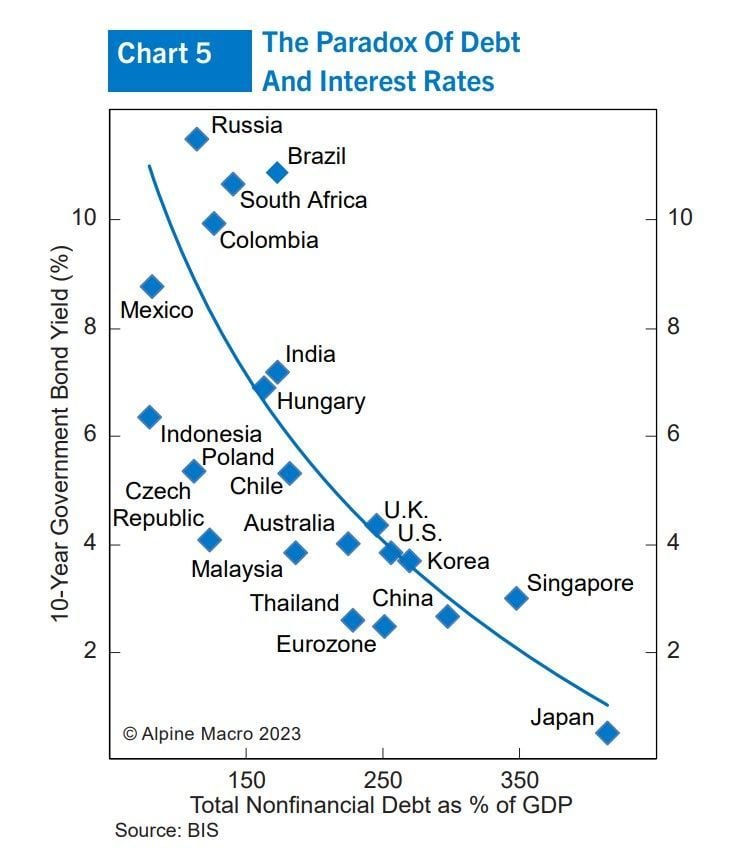

The countries that have rarely borrowed, such as Brazil or Mexico, often pay much higher interest rates than those that have much higher debt ratios, like Japan or China.

Intriguing chart by Alpine Macro

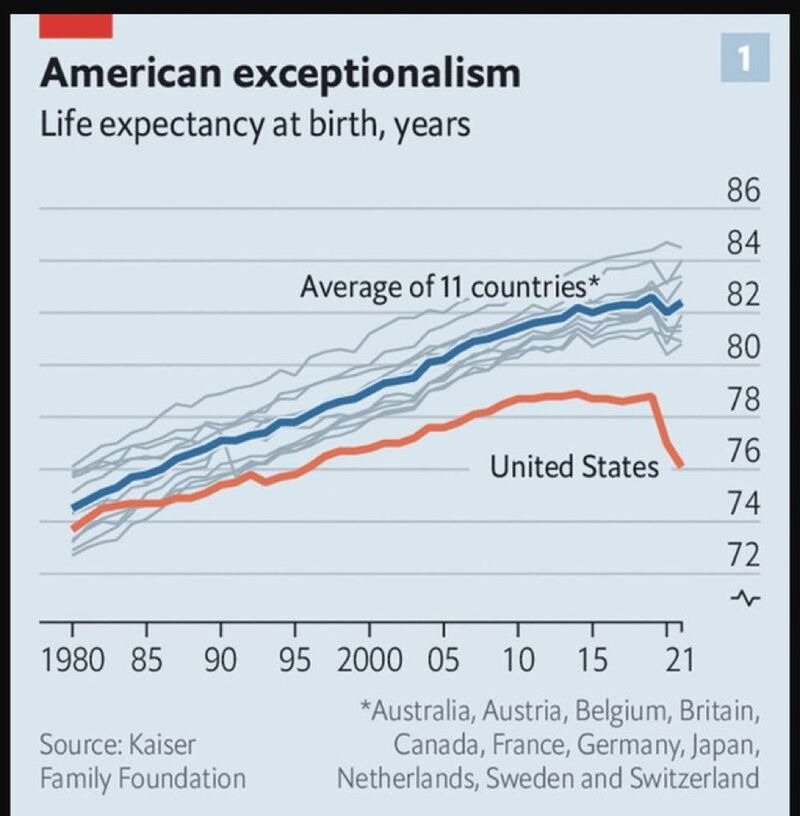

Comparable countries bounced post-COVID, but US did not

~1 million Americans have died of OD’s just since 2010; that’s more than the # of Americans that died in all wars America has ever fought in. Source: The Economist Via Dan R Dimicco thru Luke Gromen

The clearest signal that Russia is losing this war?

The Russian ruble slid past 100 to the U.S. dollar on Monday, nearing a 17-month low as President Vladimir Putin’s economic advisor blamed loose #monetarypolicy for the rapid depreciation. The ruble has lost around 27% against the greenback since the turn of the year. It also has lost 23% vs Chinese Yuan, which Russia is embracing for trade as it seeks to ditch Western currencies. The Bank of Russia has blamed the country’s shrinking balance of trade, as Russia’s current account surplus fell 85% year on year from January to July. This slide that threatens to stoke inflation in an economy that has been kneecapped by Western sanctions. Source: HolgerZ, Bloomberg, DJ, CNBC

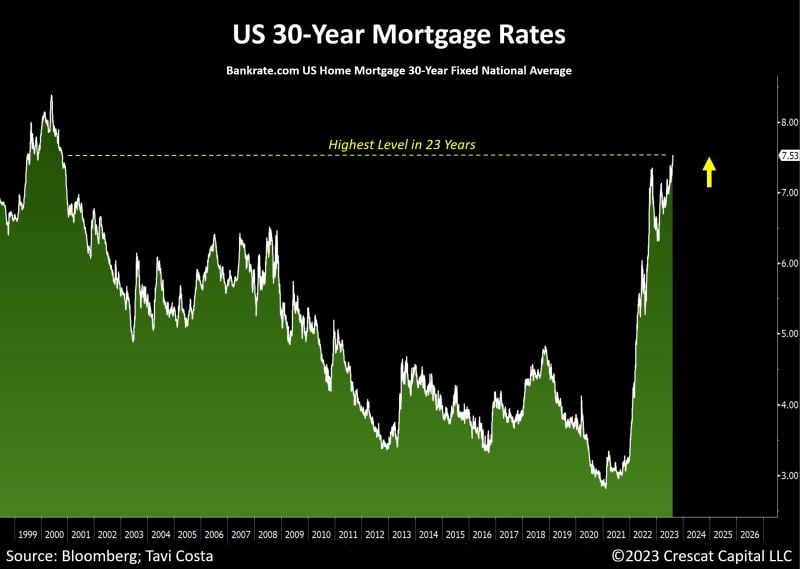

US average mortgage rates just surged above 7.5% for the first time in 23 years

There are some reasons why US house prices haven’t crashed: 1. Buyers can’t afford the rates; 2. Sellers would be insane to sell a home with a significantly lower rate to buy another at 7.5%. Market is frozen. The economy is currently experiencing a significant tightening of financial conditions, largely driven by the persisting fragility in the Treasury market. The bill will come due at some point. Source: Crescat Capital, The Wolf of All Streets

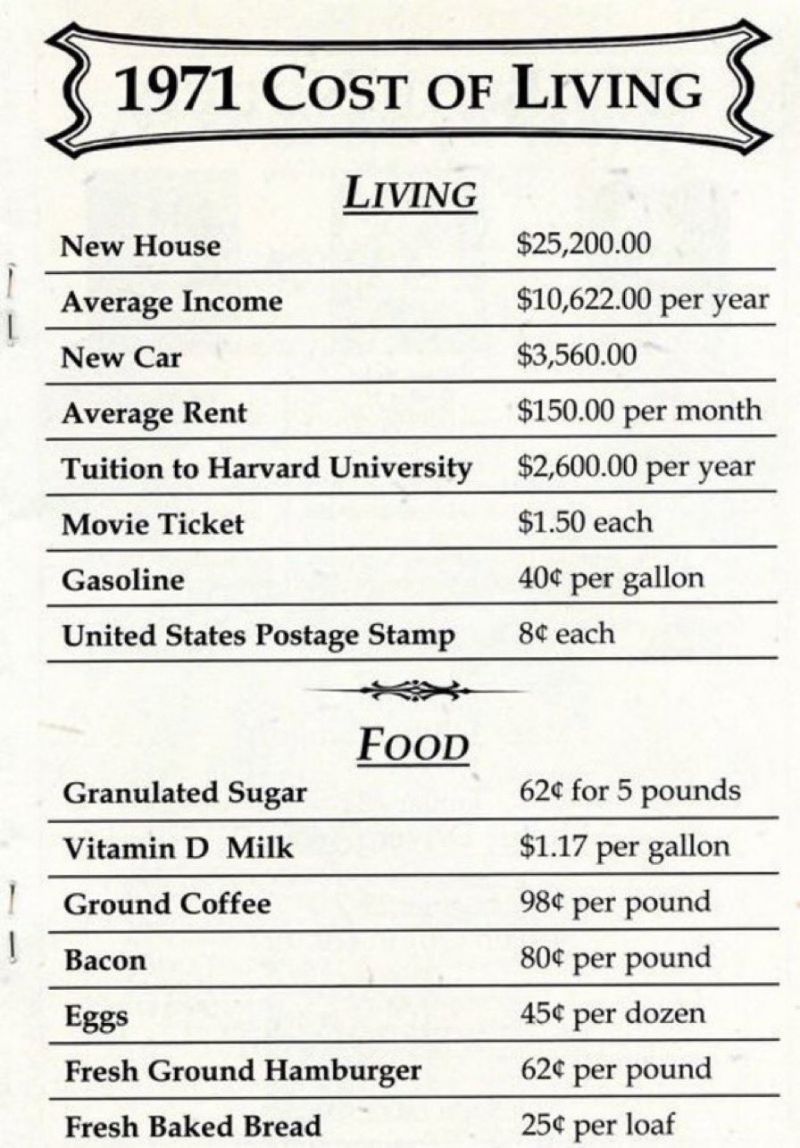

1971 vs NOW

The average U.S. annual income in 1971 paid off a house in ~2.5 years, could buy 3 new cars in a year, send 4 kids to Harvard in a year and easily afford food, shelter, necessities and entertainment. Does the older generation understand the difficulties the young face today? Source: Gabor Gurbacs

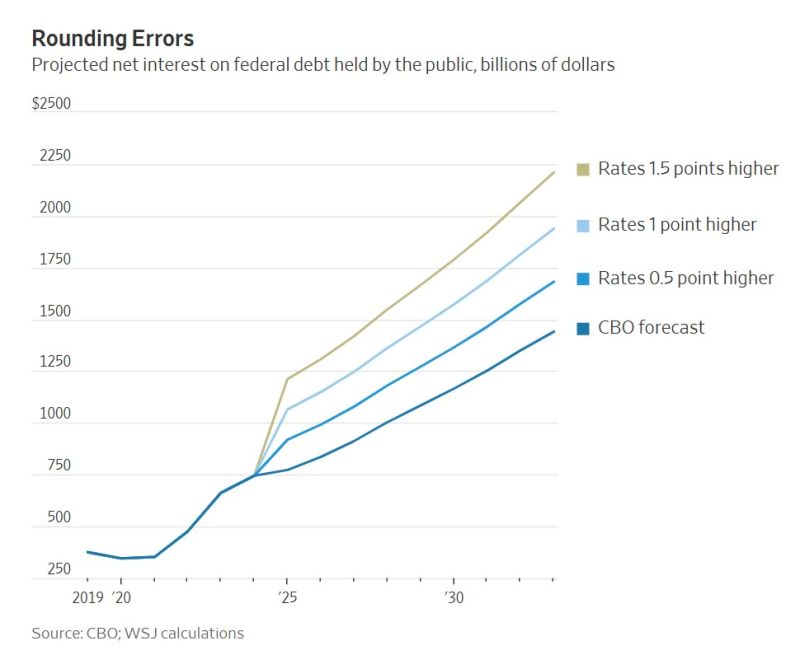

Very interesting WSJ article: "The Scary Math Behind the World’s Safest Assets. Washington has laid the seeds of a crisis that Wall Street can no longer ignore"

Here's an extract: "Consider that around three-quarters of Treasuries must be rolled over within five years. Say you added just 1 percentage point to the average interest rate in the CBO’s forecast and kept every other number unchanged. That would result in an additional $3.5 trillion in federal debt by 2033. The government’s annual interest bill alone would then be about $2 trillion. For perspective, individual income taxes are set to bring in only $2.5 trillion this year. Compound interest has a way of quickly making a bad situation worse—the sort of vicious spiral that has caused investors to flee countries such as Argentina and Russia. Having the world’s reserve currency and a printing press that allows it to never actually default makes America’s situation far better, though not consequence-free. Just letting rates rise high enough to attract more and more of the world’s savings might work for a while, but not without crushing the stock and housing markets. Or the Fed could step in and buy enough bonds to lower rates, rekindling inflation and depressing real returns on bonds".

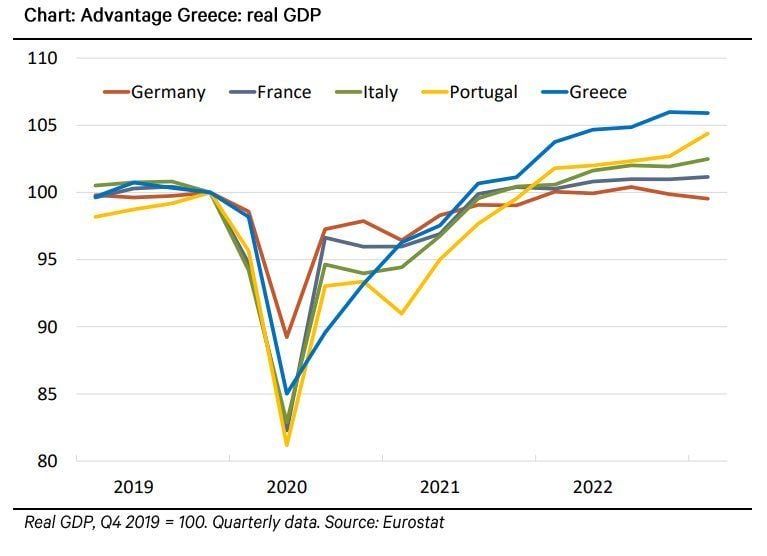

Advantage greece... A decade ago, Germany was giving lessons to Greece how to run its economy. Things can quickly change.

Source: Michael A.Arouet

Many are concerned that higher rates will hurt growth, but it turns out that a lot of S&P 500 companies have locked in debt at much lower rates until 2030

Source: Bloomberg, Goldman Sachs