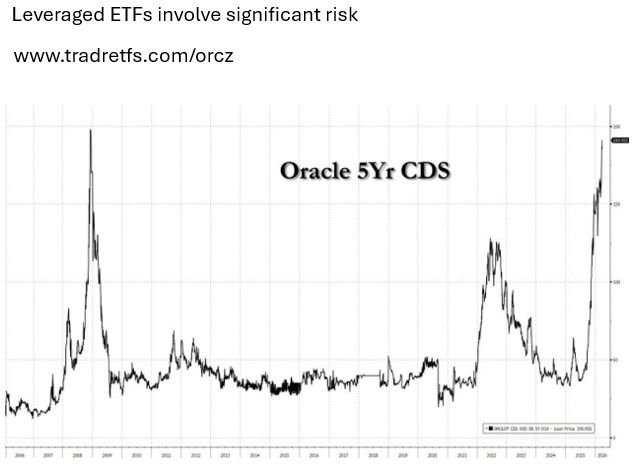

Oracle's credit risk soared earlier this year to its highest level since the Dot Com Bubble

Source. zerohedge, Barchart

Cheapest bubble to burst ever?

If Korea's equity market was in a bubble this year and if that bubble had in fact just burst, would be the cheapest bubble to burst ever.. went from 8x earnings to 5x earnings now. Source: David Ingles @DavidInglesTV

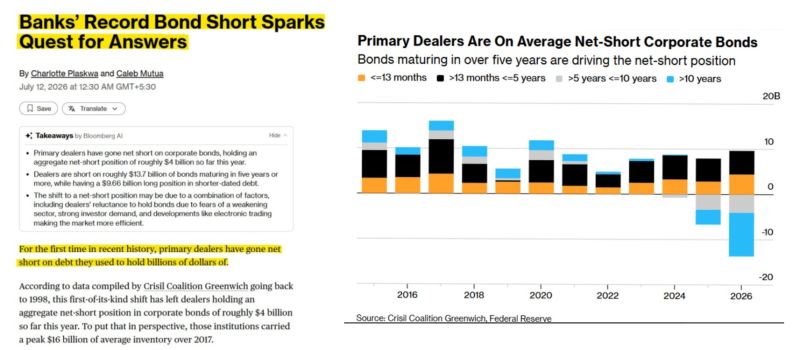

For the first time since 1998, primary dealers are net short corporate bonds.

They've sold more credit exposure than they actually own—a dramatic shift from holding an average $16B of inventory in 2017. Most of the short position is in longer-dated bonds, where rising yields hurt the most. With credit spreads near multi-decade lows, the reward for taking that risk is minimal. If yields keep rising, dealers look well positioned. But if bonds rally, they could be forced to cover into a market with limited supply, accelerating the move. One thing history shows: credit markets often crack—or recover—before equities do. Source: Bull Theory

1.2 million Korean investors were hit with margin calls in a single market crash.

That's roughly 1 in every 30 working-age adults in the country. As the KOSPI plunged 8.95%—its third-worst session since Lehman—more than 1.2 million leveraged retail accounts triggered margin calls. Around 320,000–360,000 accounts were fully liquidated, with some investors left owing money even after their positions were sold. The damage was brutal: SK Hynix: -15.4% (largest daily drop on record) Samsung: -10.7% Meanwhile, retail brokerage cash balances have fallen by ₩30 trillion to their lowest level since February. And here's the key point: forced-selling data lags by two days. The full impact of Monday's liquidation wave has **not even appeared in the official figures yet. Source: Bull Theory

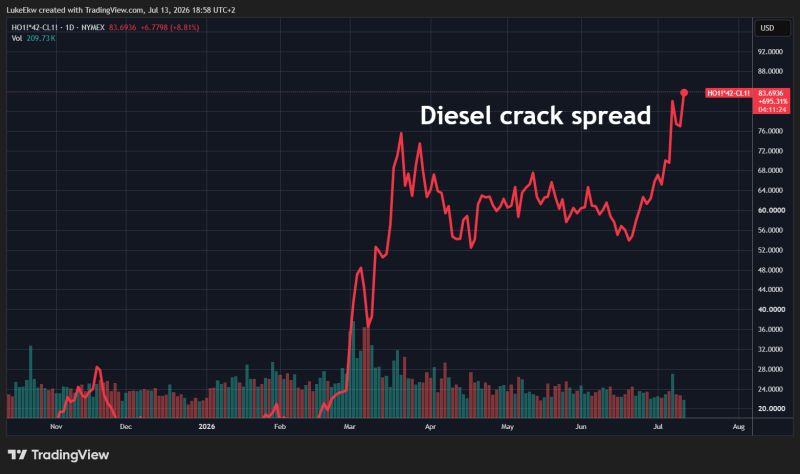

The diesel market is sending a warning that the oil market isn't.

Diesel crack spreads jumped another ~9% today, extending an already powerful rally. Why does it matter? Crude oil can be influenced by headlines, geopolitics and strategic reserves. Diesel reflects the real economy. It powers trucks, trains, ships, construction equipment and mining operations. When diesel crack spreads rise, refiners are signaling that distillate demand is outpacing supply. In other words, the market for one of the world's most important industrial fuels remains exceptionally tight. You can suppress the price of crude for a while. But it's much harder to hide what's happening in the fuel that keeps the global economy moving. Source: Lukas Ekwueme

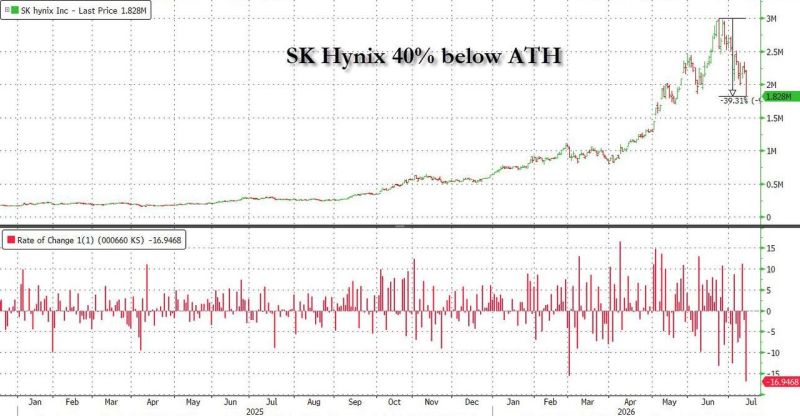

SK Hynix has now plunged 40% from its all-time high just a few weeks ago

Source: zerohedge

Healthcare Stocks just formed a Golden Cross for the first time since October 2025

The last one sent prices higher by 10% over the next 10 weeks Source: Barchart

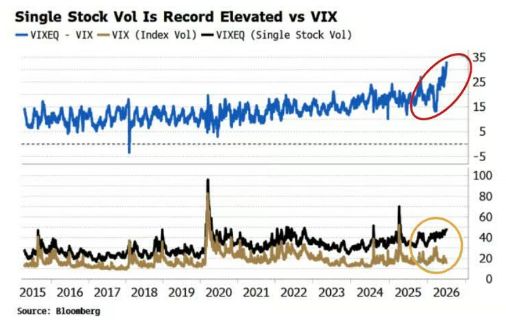

Single Stock Volatility relative to the CBOE Volatility Index $VIX has reached its largest gap in history

Source: Bloomberg, Barchart