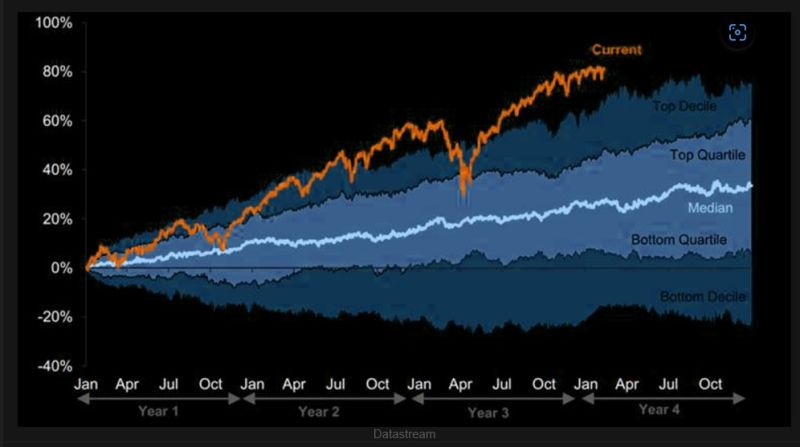

Extraordinary 3.5 years 🚀

With nearly a century of market history as the backdrop, the S&P 500's surge since late 2022 stands out as one of the more extraordinary rallies in modern market history. Source: The Market Ear

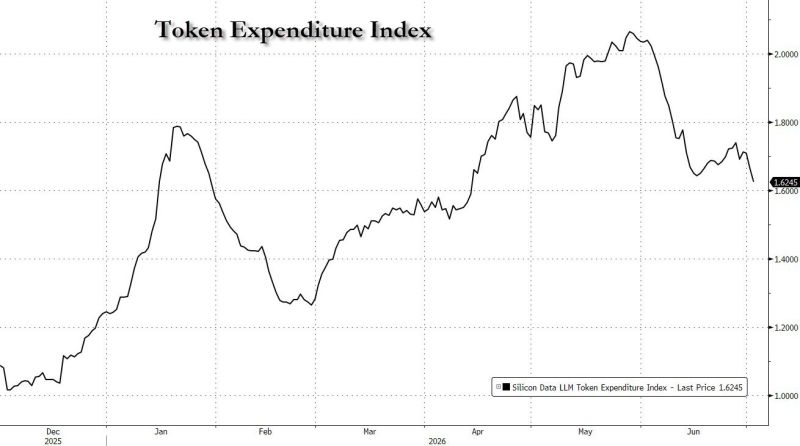

Token spending index rolling over again, down to 2.5 month low

Source: zerohedge

🚨 Markets sold off in the market as US Central Command forces have begun a series of powerful strikes on Iran in retaliation for Iranian attacks on commercial vessels in the Strait of Hormuz.

The US military called Iran's hostility "unjustified, perilous, and a clear breach of ceasefire." Iranian state media reports seven explosions in Sirik. $1 TRILLION was wiped out from stocks, precious metals, and crypto within 30 minutes after the US announced it was revoking Iran's oil export license Gold dumped -1.33% Silver dumped -2.67% Nasdaq dumped -1.87% S&P 500 dumped -0.46% Oil jumped 5% Source: Bull Theory Crypto is down $27 billion.

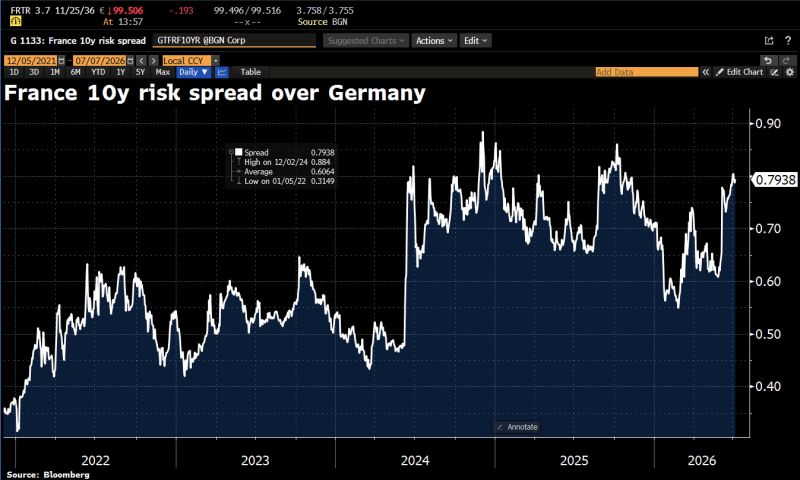

In case you missed it... France's 10y risk spread over Germany slightly rises as Le Pen cleared to run in 2027 French Presidential Election race.

Source: HolgerZ, Bloomberg

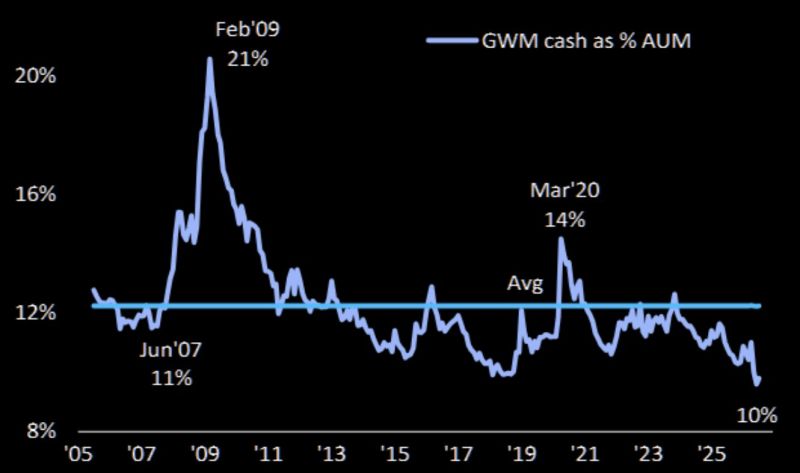

Fund Managers are now sitting on the lowest cash allocation in history 🚨

Source: BofA

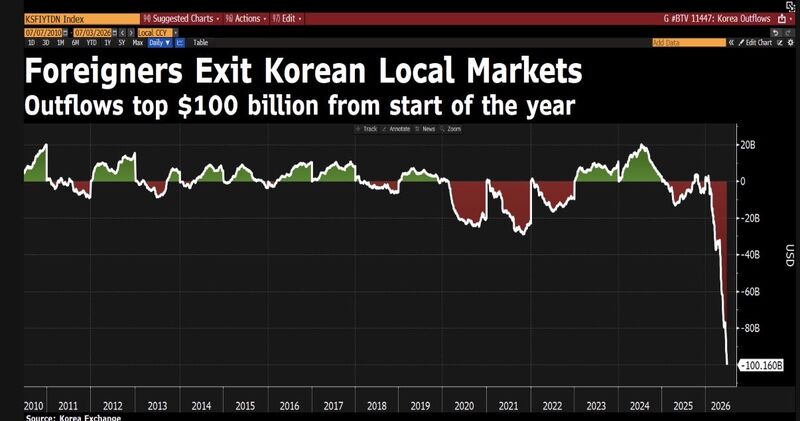

Foreign funds have now pulled $100B from Korean local stocks this year

Source: David Ingles @DavidInglesTV Bloomberg

🚨 BLOODBATH continues in South Korean and Japanese markets.

Over $400 BILLION has been wiped out from South Korean and Japanese stock markets today as the sell-off in semiconductor and tech stocks continues. South Korea's KOSPI closed down -5.35%, wiping out ₩326,350,000,000,000 ($219 BILLION). Japan's NIKKEI closed down -2.11%, wiping out over ¥30,173,000,000,000 ($184 BILLION). Over $850 BILLION has been wiped out from both markets in just two days. Source: Bull Theory @BullTheoryio

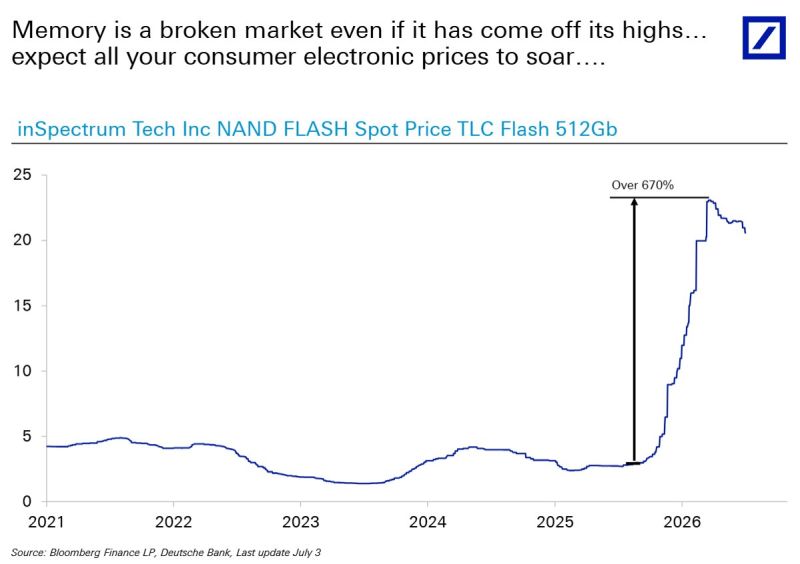

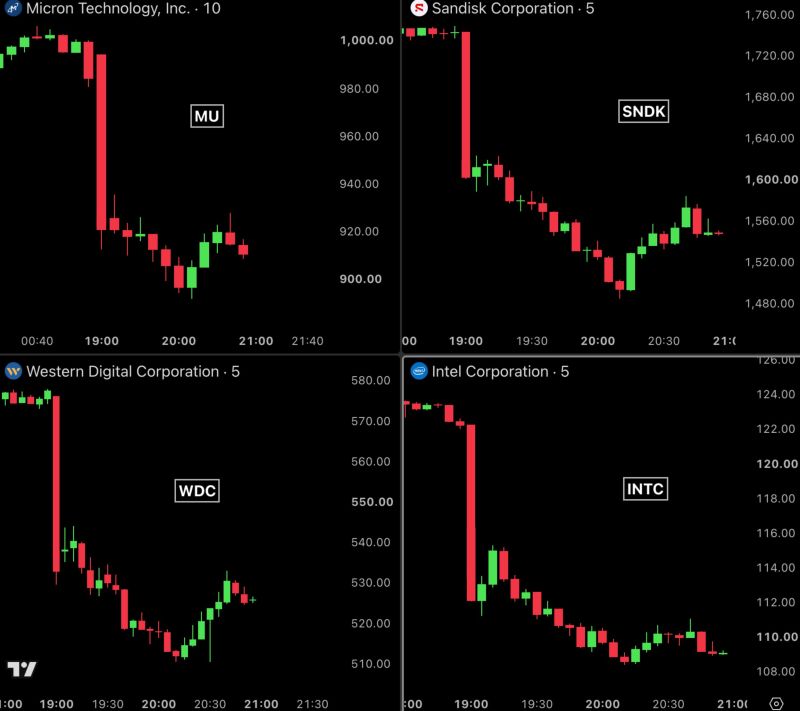

Deutsche Bank: "Memory is a broken market even if it has come off its highs... expect all your consumer electronic prices to soar"

Source: zerohedge