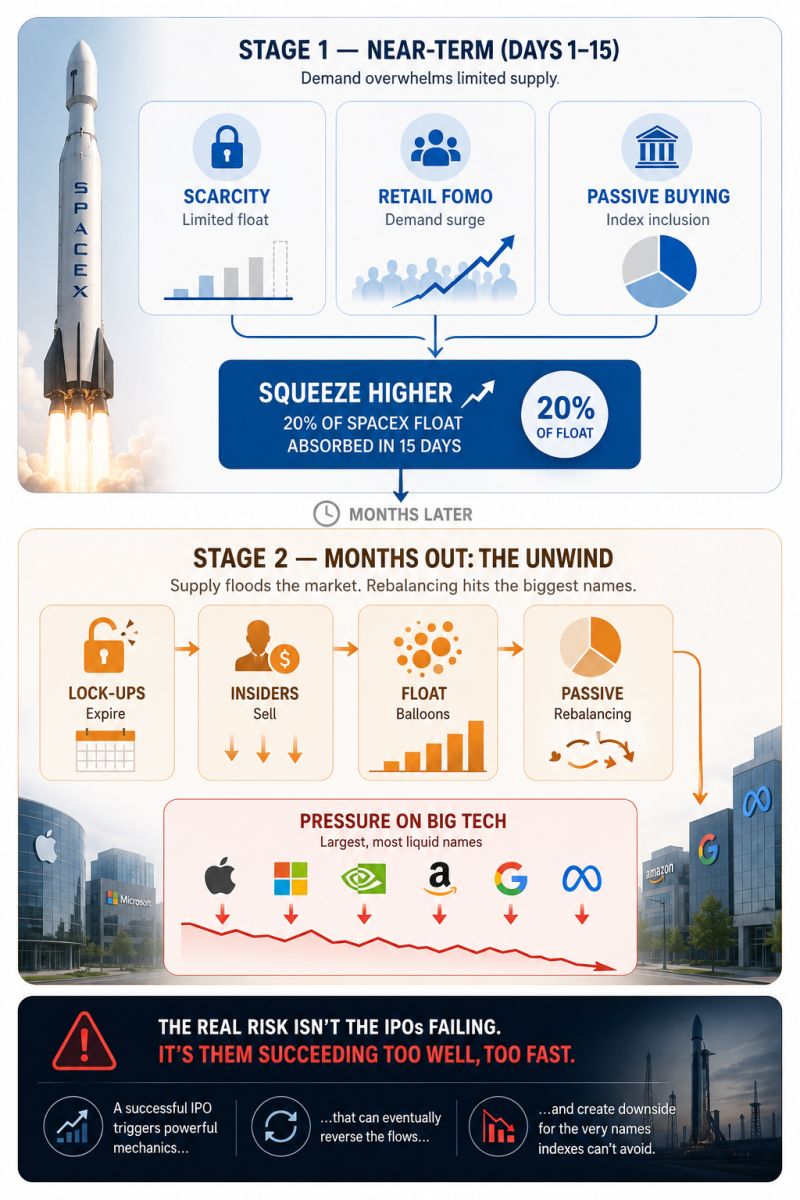

In case you missed it... SpaceX shares closed down -16.4% yesterday, wiping out over $400 billion in market value.

The decline comes after the company officially launched its inaugural offering of senior unsecured notes on June 22, seeking to raise at least $20 billion. SpaceX disclosed approximately $100.8 billion in cash and cash equivalents as of June 19, 2026. $SPCX is now down -31.3% from its all-time high, having wiped out over $927 billion in market value in just 3 days, and is trading +14.5% above its IPO price. Source: Bull Theory

MASSIVE BLOODBATH IN THE IT OUTSOURCING SECTOR.

Accenture reported earnings this morning and cut its full-year revenue forecast. Its quarterly bookings fell 2% and the stock crashed 18%. Accenture is the largest IT services company in the world, so when it reports weak demand, every other company in the sector falls with it. Cognizant fell nearly -8%. Wipro fell nearly -8%. Capgemini fell -8.4% to its lowest price in a year. IBM fell -4%. EPAM dropped to near a 52-week low. Two things are driving the selloff. Companies are spending less on IT consulting as the economy slows, and the market now believes AI is starting to do the work these companies used to charge billions for. Both pressures hit the same business model at the same time. This is a direct problem for India. Indian IT has been one of the only sectors holding up the Nifty. TCS, Infosys, HCLTech, and Wipro have been carrying the index. These companies run on the same model as Accenture and earn most of their revenue from US and European clients. Accenture's results are treated as a preview of what is coming for TCS and Infosys. Their US-listed shares already fell 3 to 5% tonight. No surprise Indian markets are getting hit... Source: Bull Theory

PRECIOUS METALS ARE CRASHING

Over $1.74 TRILLION has been wiped out from precious metals in the last 24 HOURS. Gold is down -4.75%, wiping out $1.41 trillion from its market cap. Silver is down -9%, wiping out $327 billion from its market cap. Source: Bull Theory

The dollar index $DXY bounced off a major long-term weekly trend line and is now pressing into key short-term resistance levels.

The setup has echoes of the 2020/21 consolidation, when an extended period of range trading eventually gave way to a powerful breakout higher. Importantly, the dollar is also trading comfortably above its 50-week moving average, reinforcing the improving medium-term trend. A decisive move through the 100.5 area would strengthen the breakout case. After spending more than a year coiling inside the current range, a break higher risks creating a vacuum move as traders scramble to adjust to a regime shift in the dollar. Source: TME LSEG

While financial markets have priced in the peace deal, shipping markets have not... with Freight rates still 3x pre-war levels...

Source: zerohedge

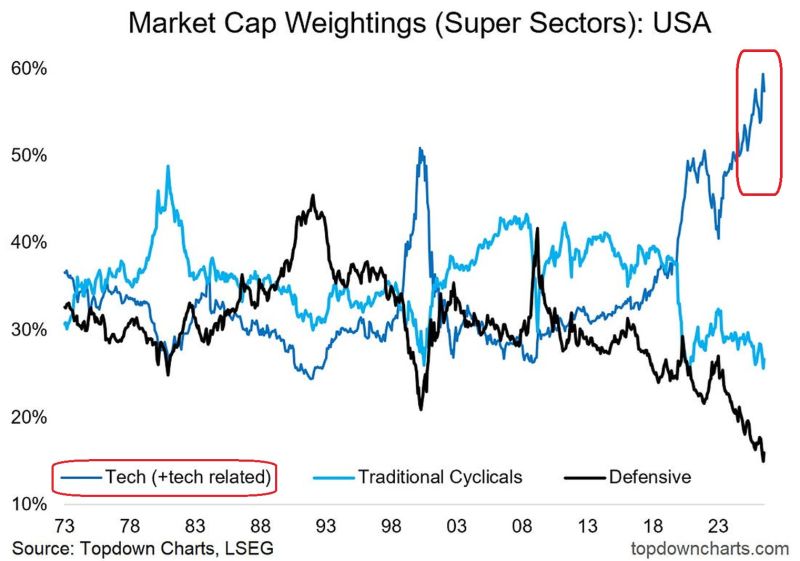

US tech and tech-related stocks now reflect nearly 60% of the total stock market cap, an all-time RECORD.

At the same time, defensive stocks account for just 15%, an all-time LOW. Not even the 2000 Dot-Com BUBBLE saw such a divergence with tech peaking at ~50% while defensives remained above 20%. Has a new era of equity market performance come, or are defensive stocks going to catch up over the years? Source: Topdown charts, Global Markets Investor @GlobalMktObserv

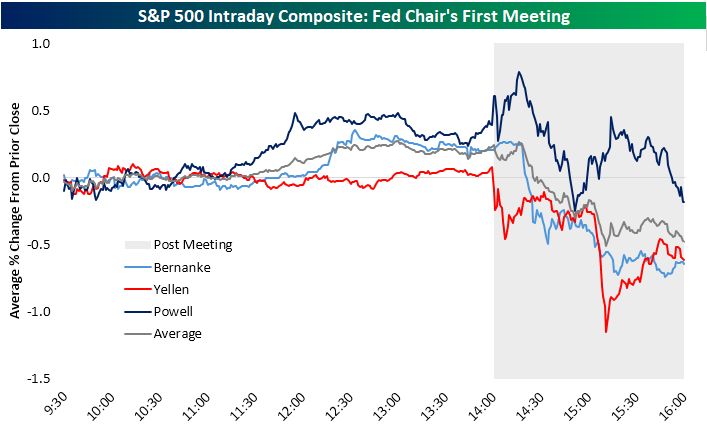

We've only had three Fed chairs experience their first "Fed Day" with markets open prior to Warsh yesterday.

All three times, the S&P was higher heading into the 2 PM rate decision only to finish in the red on the day. Warsh was no different as all main US equity indices finished in the red after his (rather hawkish) statement yesterday... Source: Bespoke

SpaceX is now the 6th largest market cap in the world ($2.64T). It is very close to Amazon and even overtook it intraday. Space X is not too far away from #4 Microsoft. What a start...

Source: www.companiesmarketcap.com