+1300% in a year, easy to think the move is done.

But as Bloomberg highlights, the Breakwave Tanker Shipping ETF (BWET) reflects deeper forces. Even before the conflict: - Aging fleet - Tight capacity - Sanctions limiting supply ➡️ The war accelerated existing trends. Now the question isn’t how far it’s gone, but what’s changed. Structural tightness remains: - Longer, more complex trade routes - Sourcing shifting farther away - Rising demand for shipping capacity ➡️ That’s why gains may not fully unwind, even with peace. As John K. notes: the story may shift from war-driven to fundamentally driven. The fundamentals still point to persistence. Source. Bloomberg

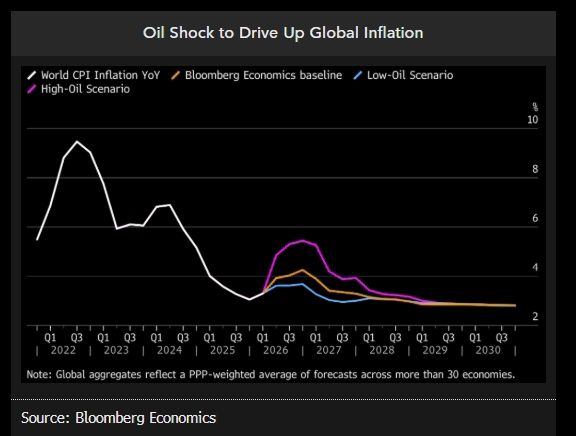

The oil shock's impact on global inflation is likely to be temporary and short-lived.

Source: Bloomberg

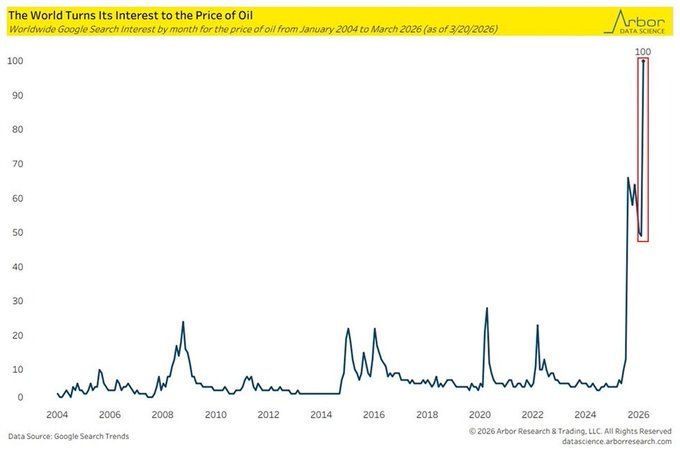

Google searches for "price of oil" just hit a record high: 300% above the 2022 Russia-Ukraine war peak and the 2008 financial crisis combined.

20 years of data. Every war, every crash, every crisis... all dwarfed by a single vertical line in 2026. The whole world is watching the pump. Source: Arbor Research, Mario Nawfal on X

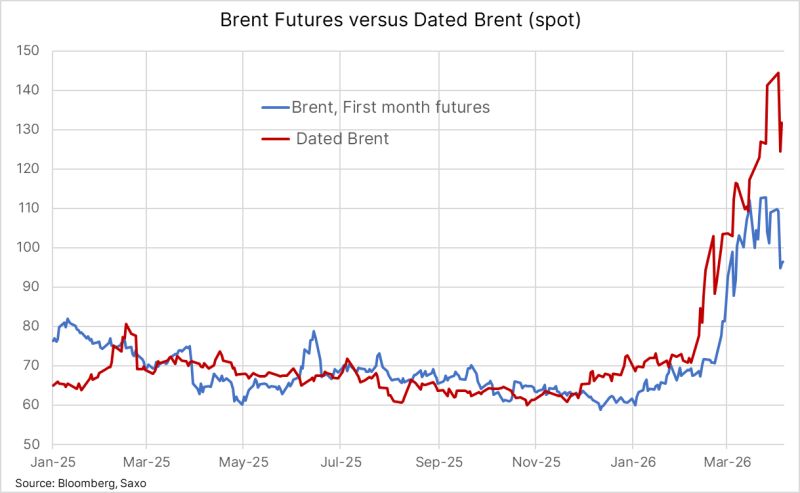

North Sea crude prices for immediate delivery continue to highlight mounting stress in the physical market

While headlines focus on futures, the real stress is building in the physical market. North Sea crude for immediate delivery is surging as European and Asian refiners scramble to replace barrels lost during the month-long Strait of Hormuz blockade. And the key signal? Dated Brent—the benchmark for physical cargoes—is telling a very different story than futures. Dated Brent jumped 7% to $132 June Brent futures are still sitting around $95 That’s not just a gap. That’s a massive dislocation between real supply and paper pricing. Meanwhile, the squeeze is getting worse: Forties Blend—another spot market indicator—traded near $147/barrel Translation: The barrels you can get today are becoming dramatically more expensive than what the market thinks oil should cost tomorrow. Why this matters: When physical markets decouple from futures like this, it often signals: Immediate supply shortages Panic buying from refiners And potential repricing across the entire energy complex Bottom line: Are Physical prices already telling us what futures haven’t caught up to yet??? Source: Ole S Hansen, Saxo Bank

The fastest oil crash since COVID just happened.

$21 gone. In hours. Here’s what the market is pricing in right now: → Hormuz reopening. Supply returns. → Strategic reserves stop draining. Pressure eases. → Saudi premium collapses. Asian refiners breathe. → LNG reroutes. Freight costs drop. Every trade that worked during the war just flipped overnight. But let’s keep in mind the full story: - The “ceasefire” is 2 weeks old. Not a peace deal. - Hormuz has real technical limitations. It doesn’t reopen like a faucet. - 11 million barrels/day of infrastructure is damaged. - Qatar LNG takes years to rebuild. Peace is harder to price than war. War gives you a narrative. Peace gives you uncertainty. The most volatile oil trade in a generation just entered its most dangerous phase — and most traders are celebrating. That’s usually when you should be careful. What’s your read? Are you buying the dip or watching from the sidelines? Source: CNBC, Jack Pradelli

Markets have historically tended to bottom well ahead of broader spillover effects.

As Andreas Steno Larsen notes, “markets typically bottom when the rate of change improves.” Source: TME

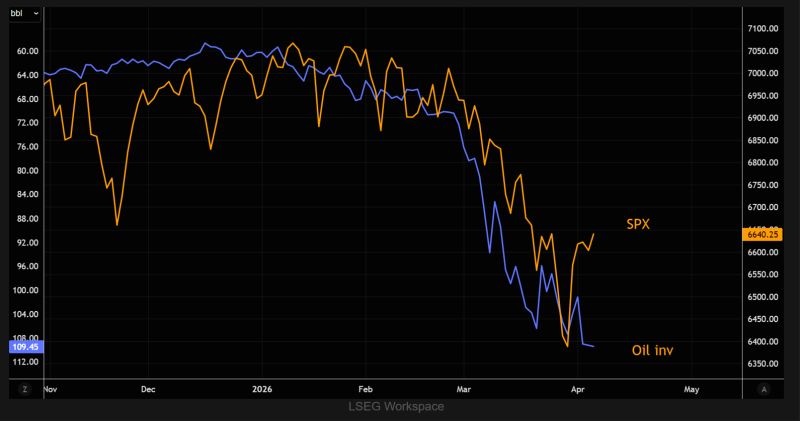

SPX has tracked oil almost tick-for-tick since the Iran war began. Now it’s starting to decouple.

Do you trust forward-looking equities, or oil stuck at extremes? Source: TME

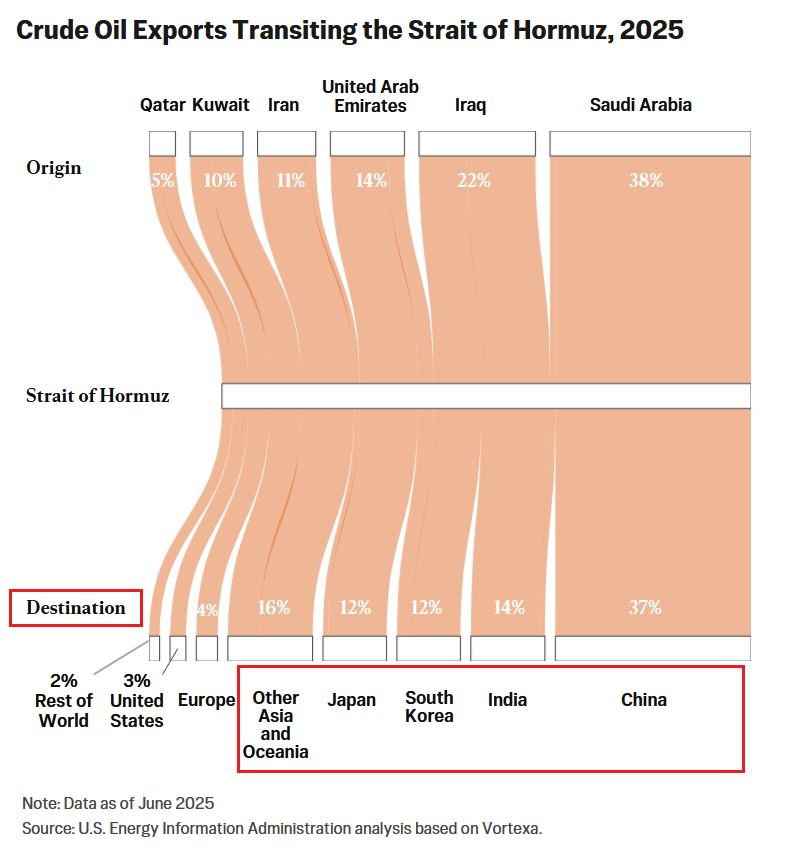

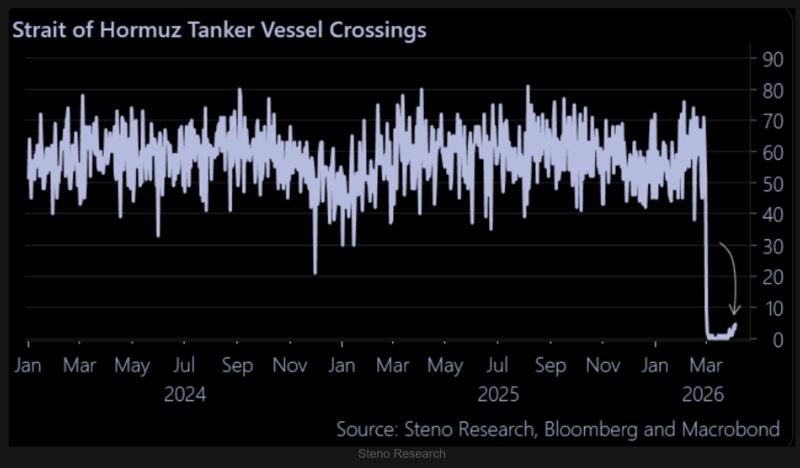

The Strait of Hormuz is the lifeline of the global economy: Saudi Arabia is the largest source of crude oil transiting the Strait at 38%, followed by Iraq at 22% and the UAE at 14%.

Iran, Kuwait, and Qatar follow at 11%, 10%, and 5%, respectively. On the destination side, China receives the largest portion at 37%, followed by India at 14%, Other Asia and Oceania at 16%, South Korea at 12%, and Japan at 12%. This means ~75% of all crude oil passing through the Strait flows to Asia, making the region overwhelmingly the most exposed to the current disruption. Saudi Arabia and Iraq alone represent 60% of all crude transiting the chokepoint, meaning any prolonged closure disproportionately impacts their export revenues and Asian buyers simultaneously. The Strait of Hormuz is the most critical chokepoint in global energy flows. Source: Global Markets Investor