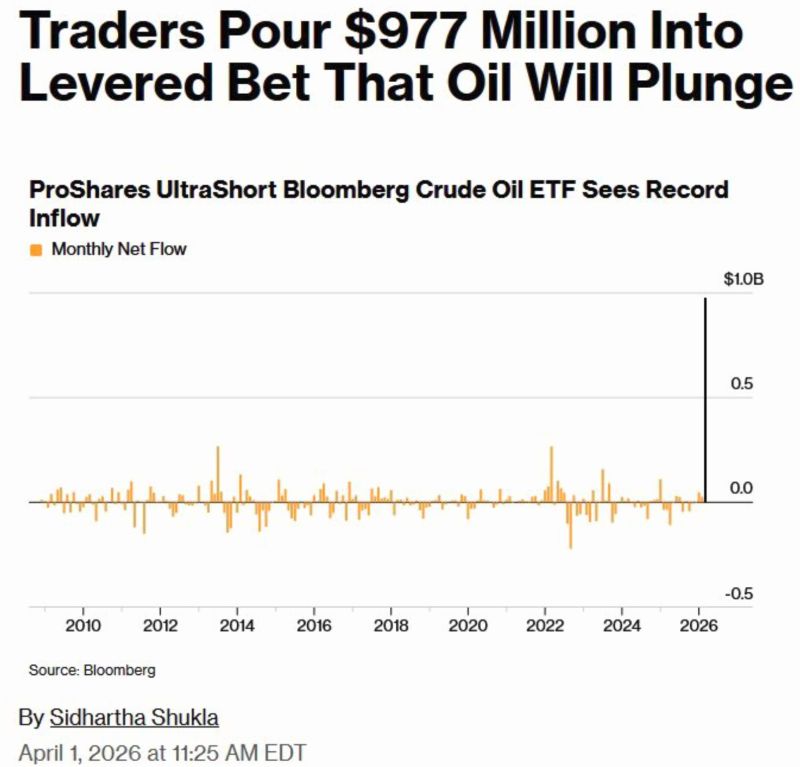

A record short bet against oil as TRADERS POUR $977 MILLION INTO LEVERED BET THAT OIL WILL PLUNGE

Just before Trump sent oil prices surging higher... Oil traders made a big leveraged bet that prices would fall from war-driven highs — but many are losing badly. Investors poured $977M into the inverse oil ETF (SCO) in March, its biggest monthly inflow ever. The fund aims to profit when oil drops, but instead plunged 41% as crude surged. The bet hinges on a quick end to conflict. While the fund briefly jumped 8% after signals of de-escalation, oil prices remain elevated — rising as high as $119 and still around $102, well above February levels. Ongoing supply disruptions, especially around the Strait of Hormuz, could keep prices high for months. Even a ceasefire may not be enough for short traders to recover. Bottom line: this is a high-risk “war ends soon” trade — and so far, it’s backfiring. Source: Markets & Mayhem, *Walter Bloomberg @DeItaone

Here are the current sensitivity measures to the oil price

Source: David Ingles, Bloomberg

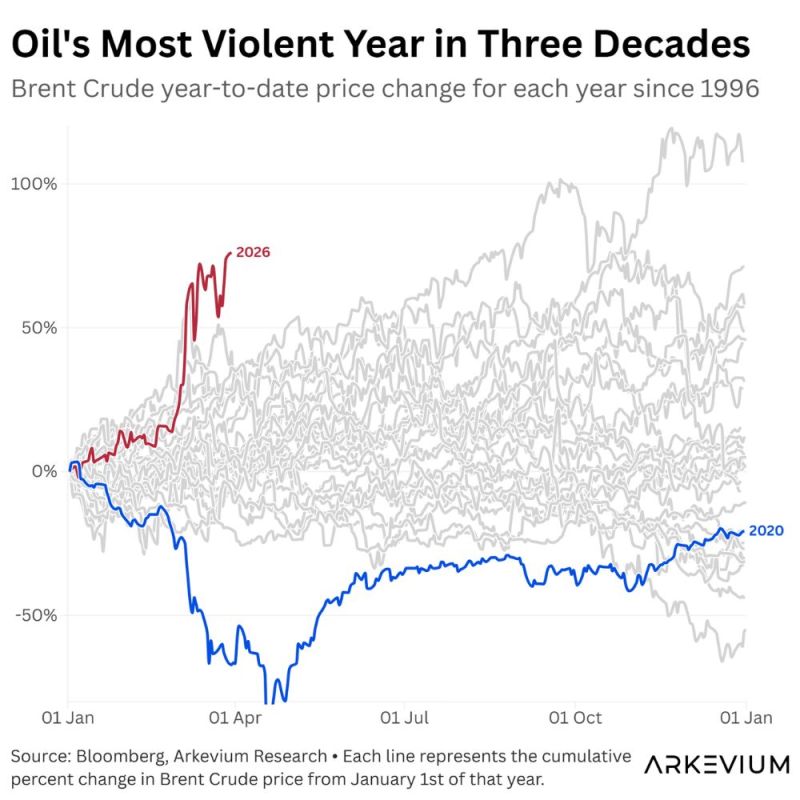

Oil is up 70% in five weeks. The last time crude moved this violently was 2020. Back then the problem was too much supply. Now it's the opposite.

Source: Maxence Visseau - Arkevium Capital & Arkevium Research

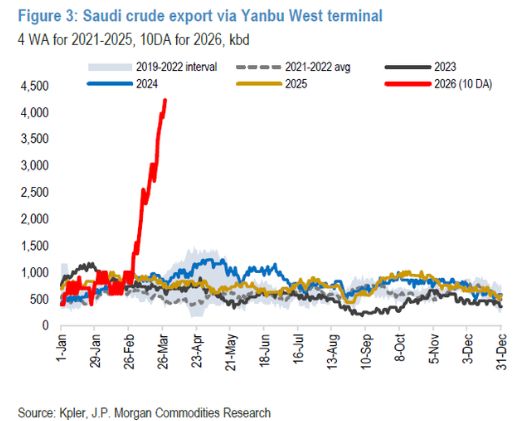

Saudi oil export through Yanbu West Terminal are skyrocketing. The next target for Iran?

The Houthis’ involvement adds a second maritime pressure point in the Red Sea, with the ability to threaten Saudi Arabia’s Yanbu export hub and disrupt traffic through the Bab al-Mandeb. This puts ~5 mbd of Saudi bypass capacity at risk, potentially adding around $20/bbl to oil prices, writes JPM's Kaneva. Workarounds exist, but longer routes could extend Asia shipping times by up to 40 days and require 130+ additional tanker voyages. Source. JP Morgan, RBC, TME

While the market panics, Buffett is raking.

Occidental Petroleum $OXY Source: Trend Spider

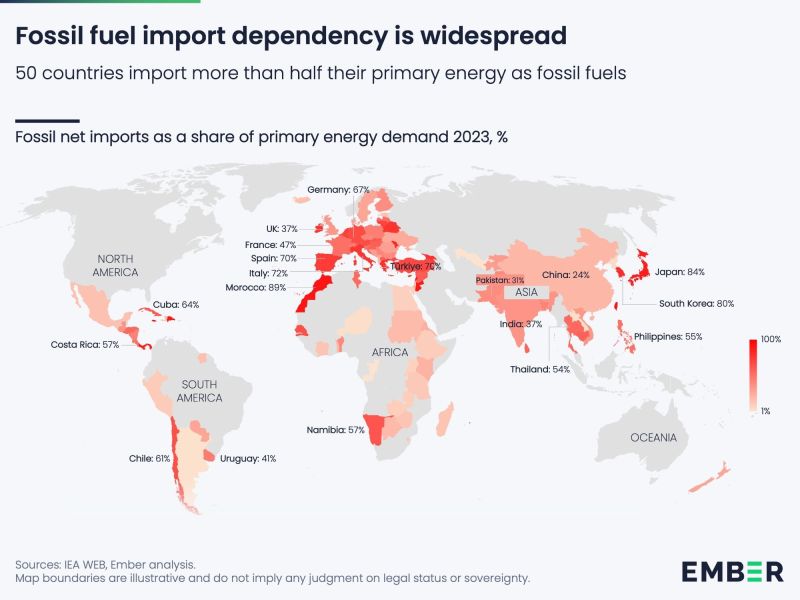

50 countries rely on imported fossil fuels for more than HALF their energy.

The Strait of Hormuz is a critical global chokepoint: disruption would hit energy-dependent economies like Japan, South Korea, and Germany. Despite shifts after past crises, reliance on fossil fuels remains high and concentrated in volatile regions. The energy transition is progressing, but too slowly to mitigate immediate geopolitical and supply risks. Source: Jack Prandelli on X, Ember

Russian oil export revenues are at their highest since the 2022 invasion of Ukraine

Gross income from seaborne crude exports surged to $2.46 billion for the week ending March 22, the highest since March 2022. The 4-week average is up to $1.71 billion per week, up from $900 million in January. This comes as the value of Russian crude exports has DOUBLED over the last 3 weeks, rising from an average of $135 million per day in January to $270 million per day now. The surge is being driven by soaring global oil prices and a US tariff waiver allowing buyers to purchase Russian crude loaded before March 12, boosting sales to India significantly. Years of Western sanctions pressure have been undone in a matter of weeks. Source: Global Markets Investors, Bloomberg

Is the petrodollar era starting to erode?

A Deutsche Bank report questions the future of the petrodollar system, where oil trade in USD underpins global demand for the currency. Emerging shifts Middle Eastern oil flowing to Asia, countries like Russia and Iran trading outside the dollar, and Saudi Arabia considering alternatives are increasing pressure. Geopolitical tensions and risks to Gulf supply routes could accelerate change. Combined with the rise of renewables and energy independence, a gradual decline in USD dominance may reshape global financial power.Source: ZeroHedge, Deutsche Bank