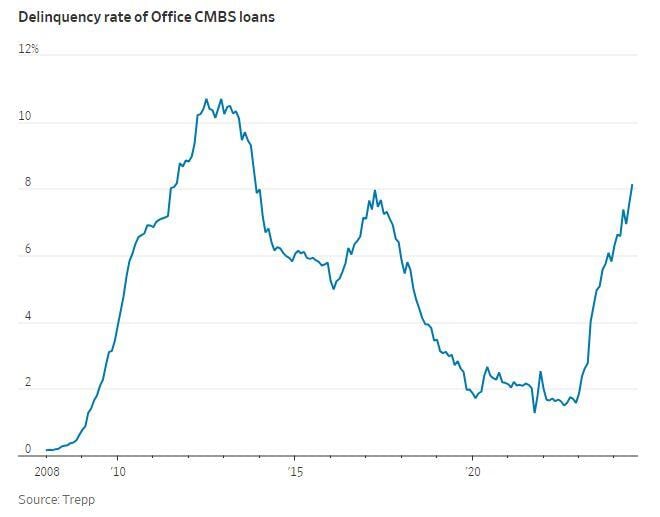

Delinquency rates on Office building loans hit 8.11%, the highest in more than a decade 🚨

Source: Barchart

📢 One out of every 15 Americans is a millionaire according to a UBS Wealth Report

Source: UBS, Barchart

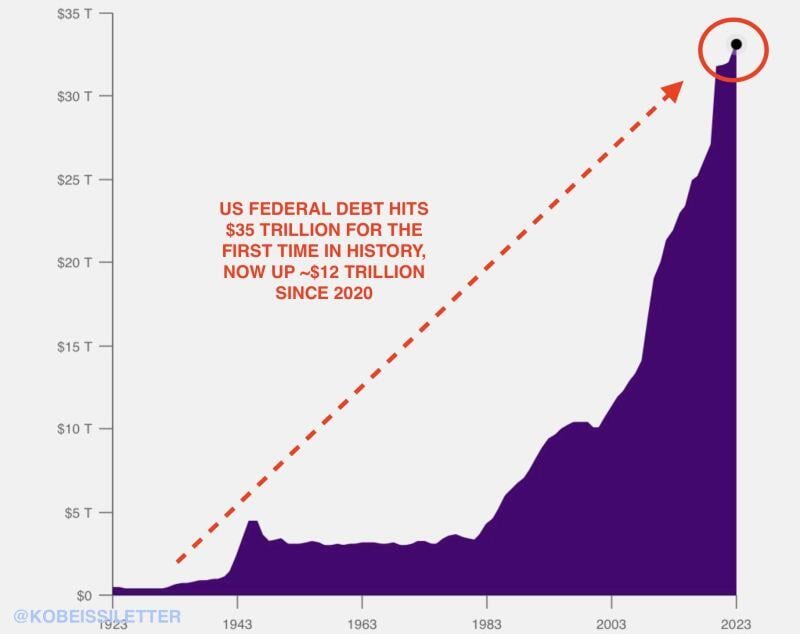

Total US Federal debt has officially hit $35 trillion for the first time in history.

Since 2020, the US has now added ~$12 TRILLION in Federal debt. In other words, the US has added an average of ~$280 BILLION of Federal debt EVERY MONTH since January 2020. This means that the US now has ~$105,000 in Federal debt for every person living in the country. All while deficit spending as a percentage of GDP is currently at World War 2 levels. Source: The Kobeissi Letter

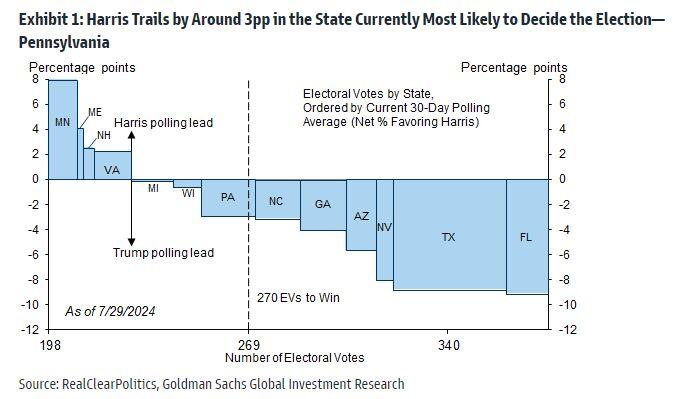

Goldman: Harris Trails by Around 3pp in the State Currently Most Likely to Decide the Election—Pennsylvania

Source: Mike Z., Goldman Sachs

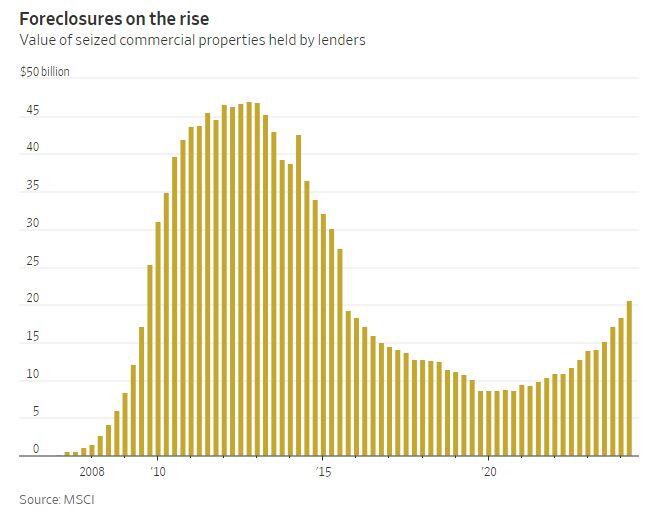

US Commercial Property Foreclosures jump to more than $20 billion during the 2nd quarter, the most in nearly a decade 🚨

Source: Barchart

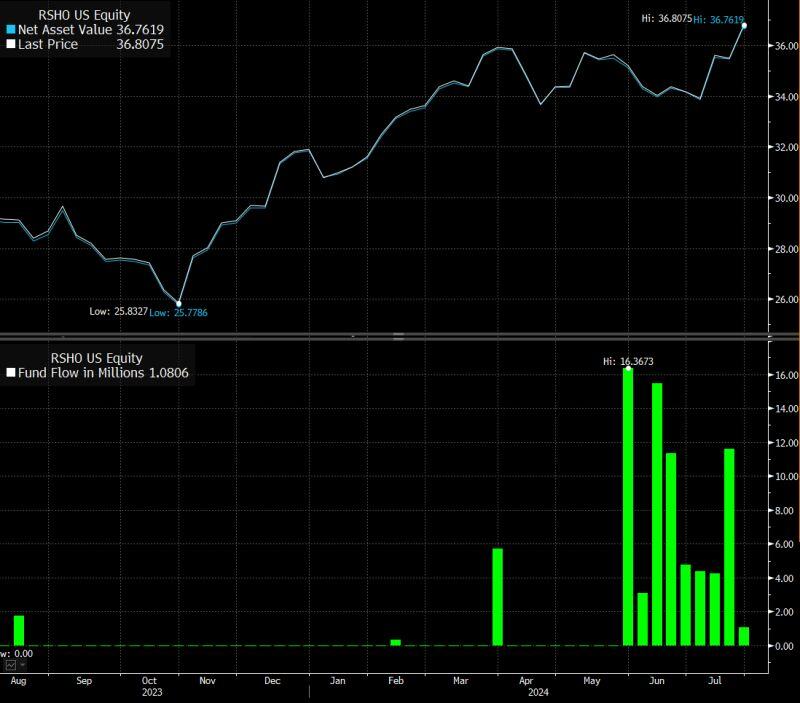

As highlighted by Eric Balchunas

The Reshoring ETF $RSHO is quietly nursing a 9-week flow streak (after being ignored since birth) which boosted its assets under management 7x this year. The American Industrial Renaissance ($AIRR) 3ETF also saw AuM jump by $800m YTD. BlackRock noticed this and launched iShares US Manufacturing ETF $MADE. All these ETFS are exposed to Trump Trade 2.0 but this theme spans beyond politics. Source: Bloomberg, Eric Balchunas

US Presidential elections >>> Are we back to square one?

Source: PredictIt, Bloomberg, www.zerohedge.com

The US government just moved $2 billion of seized bitcoin $BTC, two days after Trump's speech 👀

Source: Joe Consorti