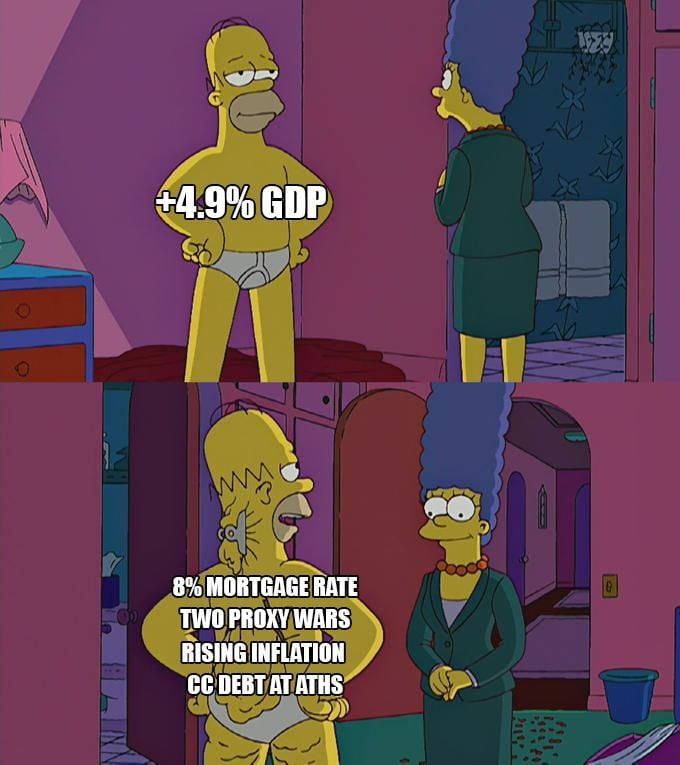

US Q3 GDP numbers summarized in one cartoon

Source: Elizabeth Oliveira Fonseca

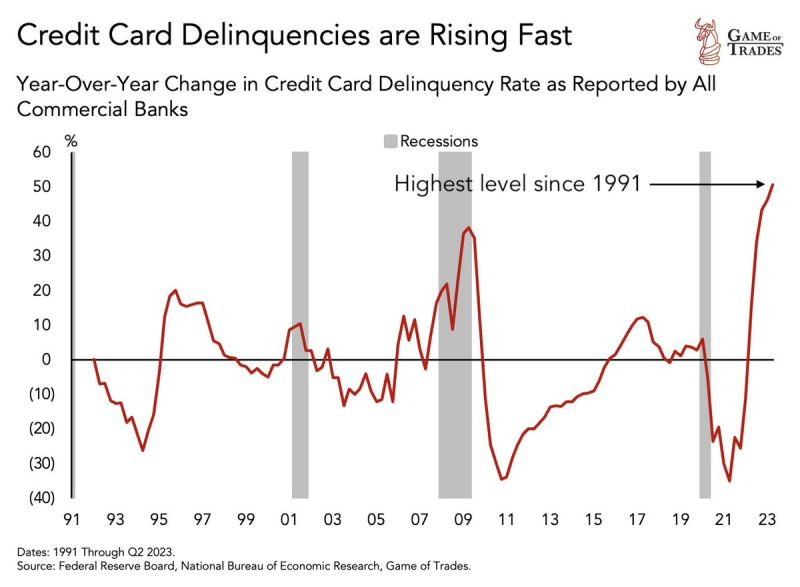

This is WORSE than the 2008 Financial Crisis. Credit card defaults are rising at levels NEVER seen in 3 decades

Source: Game of Trades

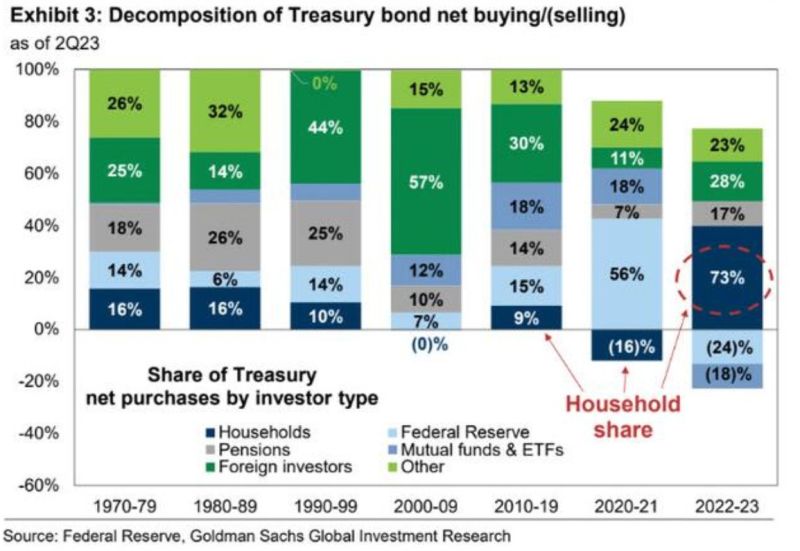

Adding to that Great Rotation theme is this chart

US households account for 73% of Treasury bond buying in 2022-2023 (so far) A lot of pain being experienced for those not willing to hold to maturity amid this bond blood bath... Source: Markets & Mayhem, Goldman Sachs

P/E Forward for the largest US companies - Magnificent 7

$TSLA Tesla 62 $AMZN Amazon 58 $NVDA NVIDIA 40 $MSFT Microsoft 30. $AAPL Apple 28 $GOOGL Alphabet 24 $META Meta 23 Source: Vlad Bastion

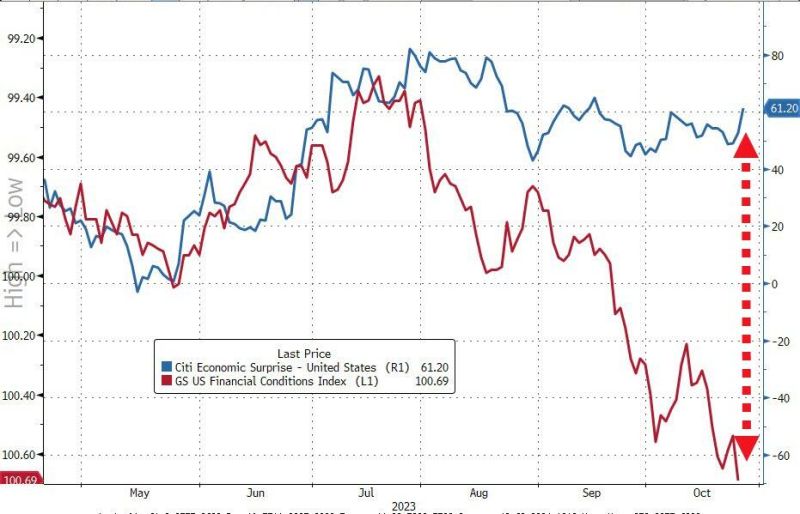

For now, the monetary policy transmission route of tightening US financial conditions are NOT reaching the economy...

Indeed, an avalanche of US macro data on Thursday presented a positive blend of updates across growth (better), inflation (lower), and labor markets (looser/worse). - Economic Growth: Real GDP rose 4.9% in 3Q (consensus 4.5%) driven by strong demand across consumer and federal/state government, and inventories. However, a major contribution from inventories could in turn weigh significantly on growth in 4Q - Manufacturing: Orders for Durable and core capital goods also grew by more than expected... thanks to a massive surge in non-defense aircraft orders (so don't expect it to last). - Housing: Pending home sales rose 1.1% month over month in September, above expectations for a decline... but brace for October to be a bloodbath as mortgage rates re-accelerated. - Inflation: Core PCE prices component of the GDP report rose less than expected. - Labor: Initial and continuing jobless claims both increased by more than expected -- a positive for markets which are focused on labor market re-balancing (i.e., could benefit from less wage inflation).

US GDP grew 4.9% in Q3 QoQ annualized, way faster than +4.3% expected

However, bond yields dropped in the afternoon session. This Bloomberg US GDP chart shows why. Indeed, US GDP growth in Q3 was mainly driven by private consumption & inventories. This may not last. Source: Bloomberg, HolgerZ

US stocks now account for 61% of the $60 Trillion MSCI All-Country World Index, the highest level in history

Source: FT, Barchart, Bloomberg

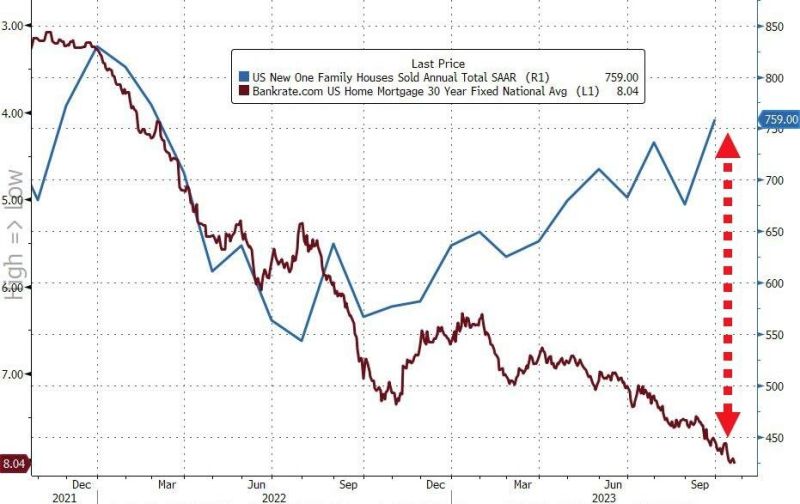

The US housing market conundrum ->

New home sales just surged 12.3% month-over-month in September, the largest jump since August 2022. Even as mortgage rates push above 8% for the first time in 23 years, new home sales are surging. The gap between new home sales and mortgage rates has never been wider. Why is this happening? Explanation by The Kobeissi Letter: -> Homebuilders are taking on some of the cost of higher mortgages AND existing home sales are at their lowest since 2010. New homes are the only option for buyers and homebuilders are helping pay for it. Source: The Kobeissi Letter, www.zerohedge.com