🚨 Very interesting note by Eric Balchunas: Has the US stock market become "too important to fail"?

More than 55% of Americans now own stocks, the highest participation rate in the world. With new retirement programs bringing millions more investors into the market, Wall Street is becoming deeply intertwined with household wealth, retirement security, and even politics. The implication is profound: future policymakers may face overwhelming pressure to prevent prolonged bear markets. Some believe that, in the next major crisis, the Federal Reserve could even follow Japan and China by purchasing equity ETFs to stabilize markets. Whether or not that happens, one thing is clear: the growing financialization of the US economy is reshaping how investors think about downside risk—and may help explain why markets continue to recover so quickly after every sell-off. Source: Eric Balchunas, Bloomberg

🚨 Donald Trump has escalated pressure on Europe, warning that the US could withdraw all American troops from the continent unless allies do more on defense.

He also renewed his demand for US control of Greenland, arguing the Arctic island is strategically vital against growing Chinese and Russian influence. The remarks revive one of the biggest sources of tension within NATO, as European leaders fear a weakening of the US security commitment. With around 80,000 US troops stationed across Europe, any significant withdrawal would mark a historic shift in transatlantic security and reshape the continent’s defense landscape. Source: FT

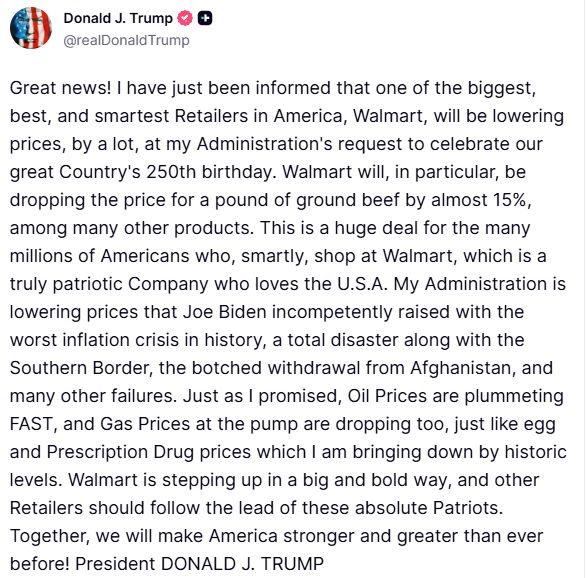

*TRUMP: WALMART WILL DROP PRICE FOR GROUND BEEF BY ALMOST 15%

*TRUMP: OTHER RETAILERS SHOULD FOLLOW WALMART'S LEAD Source: zerohedge

BREAKING: Bitcoin reclaims $64,000 after the White House confirms the U.S. strategic Bitcoin reserve, and Trump says he is a "Big Fan of Crypto."

$360 million in short positions were liquidated today. Source: Bull Theory

🚨 BREAKING: The US is officially building its Strategic Bitcoin Reserve.*

The White House confirmed it is now putting the legal and operational framework in place to formally manage the reserve. The US already holds 328,372 Bitcoin worth roughly $25 billion—about 1.56% of Bitcoin's circulating supply—making it the world's largest known government holder. What's remarkable? None of it was purchased. Every Bitcoin was seized through criminal and civil asset forfeitures, and the government has pledged not to sell a single coin. Meanwhile, a separate Digital Asset Stockpile will hold seized cryptocurrencies such as Ethereum and XRP. The bigger story is what comes next. Congress is considering the American Reserves Modernization Act, which would authorize the Treasury to acquire 1 million Bitcoin over five years with a minimum 20-year holding period. If approved, it would mark the first time a nation actively accumulates Bitcoin as a strategic reserve asset. Source: Bull Theory on X

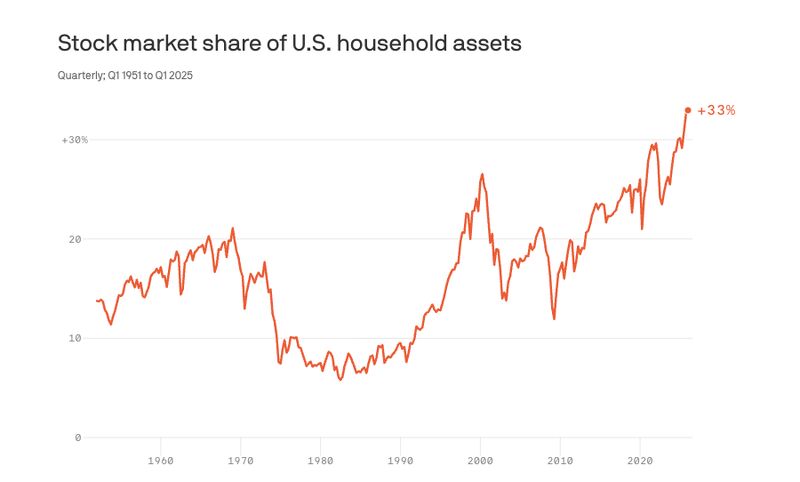

AMERICAN HOUSEHOLDS ARE MORE INVESTED IN STOCKS THAN EVER

Stocks now make up a record-high share of U.S. household assets, Axios reports. American household wealth is now more tied to equities than ever before, making consumers more exposed to market swings. Source: Coin Bureau

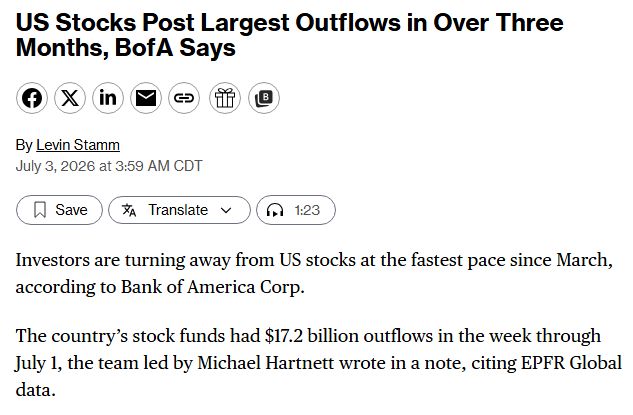

Investors dumped Stocks last week at the fastest pace since March

Source: BofA, Barchart

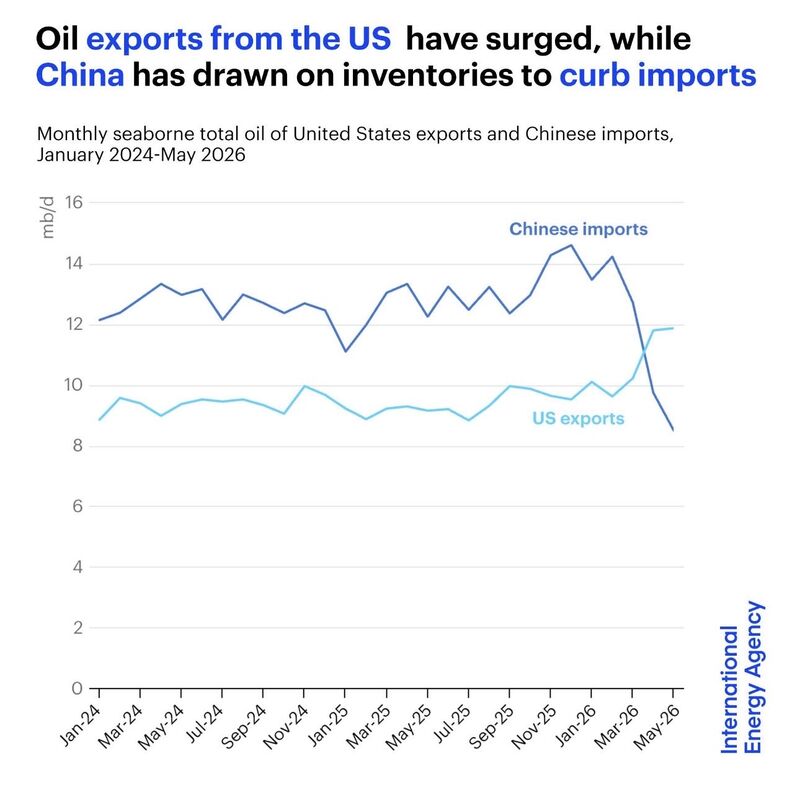

One chart may have just revealed a major shift in the global energy order.

For the first time in history, U.S. oil exports have surpassed China's crude oil imports. At first glance, it looks like just two lines crossing on a chart. In reality, it could mark a profound structural change. For two years, China's crude imports hovered around 12–14 million barrels per day. Then they suddenly plunged to roughly 8.5 million. At the same time, U.S. oil exports, long stuck around 9–10 million barrels per day, surged above 12 million. Why? China didn't stop buying oil because demand disappeared. It stopped because supply became constrained. • Nearly 38% of China's crude imports depended on the Strait of Hormuz. • Gulf producers faced major disruptions. • Russia was already exporting at full capacity. • U.S. light sweet crude isn't an ideal substitute for many Chinese refineries. With few alternatives, China began drawing down strategic inventories instead of importing. That collapse in imports isn't necessarily a sign of weaker demand. It may be evidence of a country relying on its emergency reserves to navigate one of the biggest supply shocks in years. Meanwhile, U.S. exporters stepped in to replace part of the missing Gulf supply. Sometimes, the most important geopolitical shifts don't make the front page. They simply appear when two lines cross on a chart. Source. Jack Prandelli on X, IEA