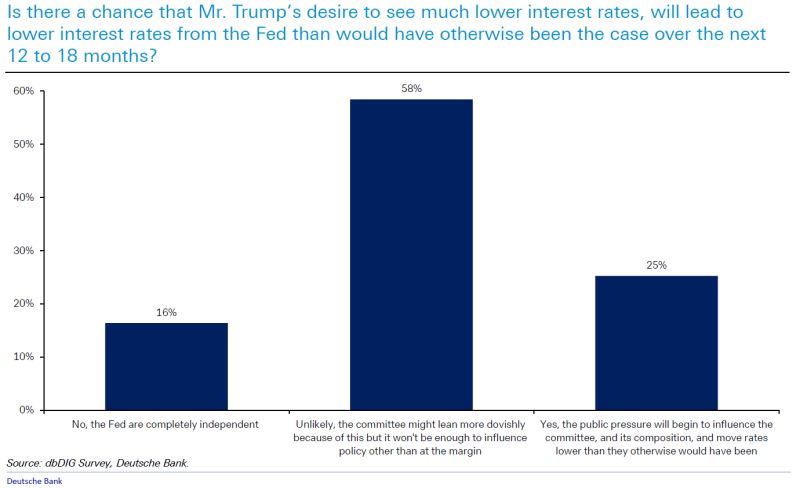

Only 16% of respondents in a recent Deutsche Bank survey believe the Fed is completely independent, with 25% seeing political pressure leading to lower rates.

Source: DB thru Liz Abramowicz

Notable: Coming back to yesterday's US non farm payrolls

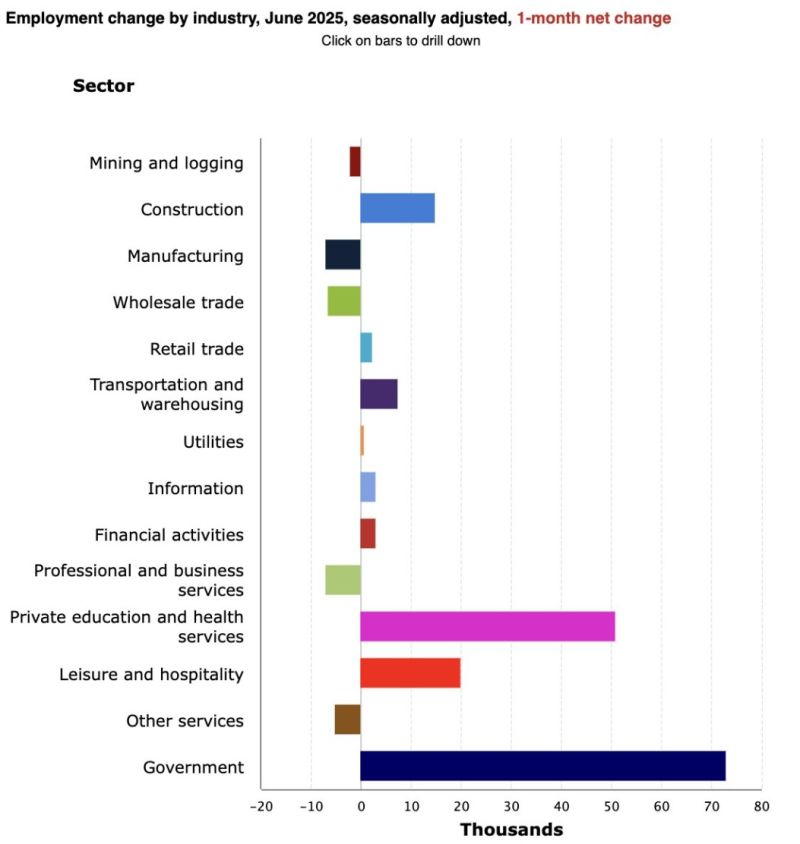

-> The 147,000 job gains in June were almost all (over 75%) in healthcare and government. Government: +73,000 Healthcare: +39,000 The government job gains looked like this: State gov't education +40,000 State gov't non-education +7,000 Local gov't education +23,000 Local gov't non education +10,000 Federal gov't -7,000 Source: Heather Long on X

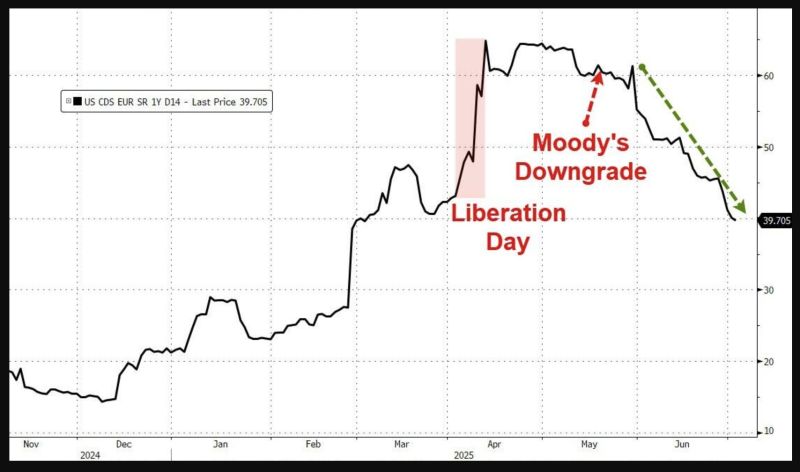

It seems the world is becoming MORE comfortable with USA sovereign risk once again...

(below US CDS) Source: Bloomberg, www.zerohedge.com

Key U.S. Economic Indicators Hitting New Highs

1. Stocks: all-time high 2. Home Prices: all-time high 3. Bitcoin: all-time high 4. Money Supply: all-time high 5. National Debt: all-time high 6. CPI Inflation: 4% per year since Jan 2020, 2x the Fed's "target" 7. Fed: expected to cut rates between 1x and 2x this year 8. The US Treasury is skewing issuance further to bills (Fiscal QE) Source. Charlie Bilello

Happy Independence Day!

Source: hedgeye

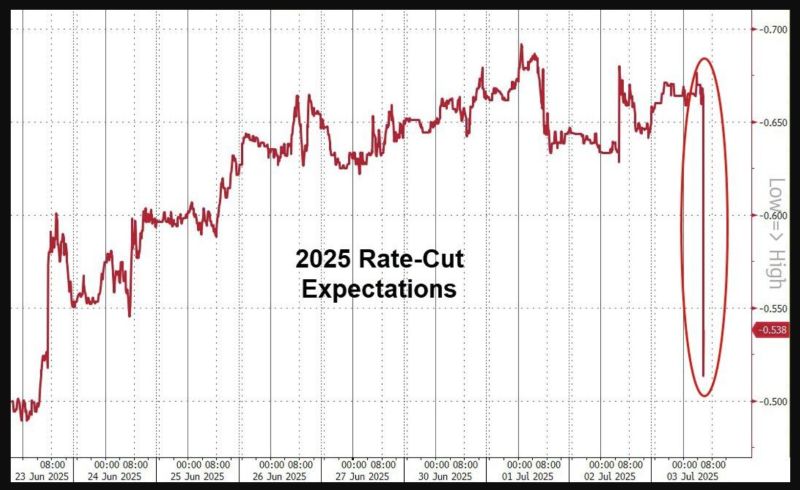

Overall 2025 fed rate cut expectations tumbled on "Big Beautiful Bill" being passed & better us payrolls

Source: www.zerohedge.com, Bloomberg

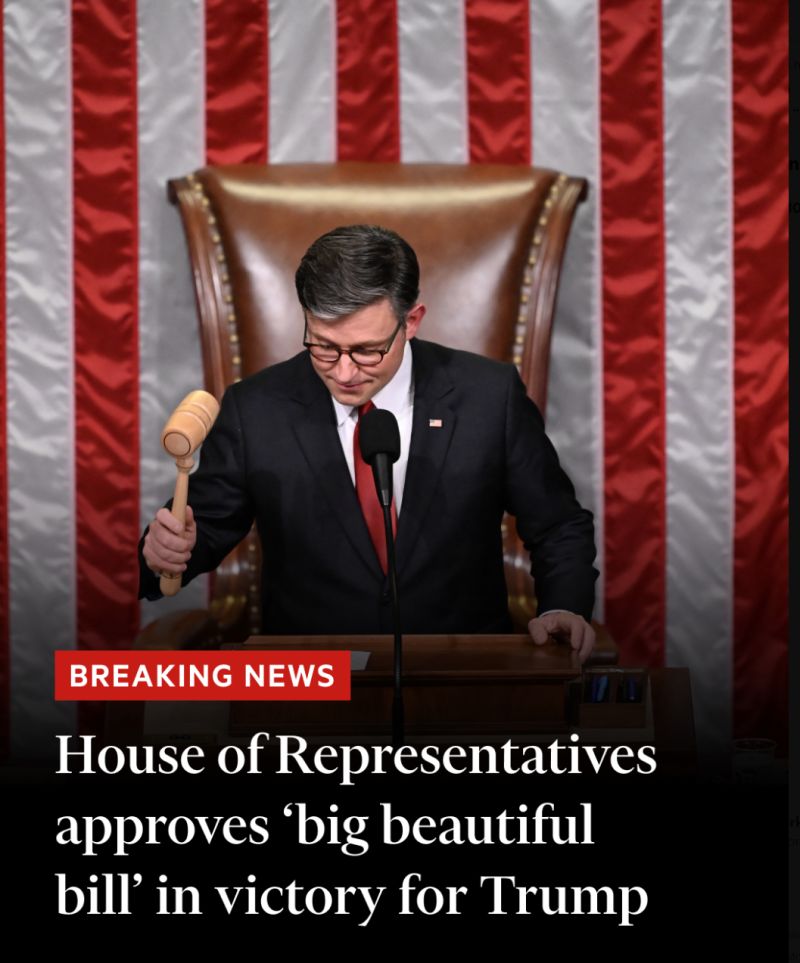

BREAKING

🔴 Donald Trump has secured passage of his flagship tax and spending legislation after the House of Representatives approved the bill, handing the US president a political triumph six months into his second term ✅ ▶️ The 218 to 214 vote by the House on Thursday came after Democratic minority leader Hakeem Jeffries spoke against what he called the “ugly” legislation for a record eight hours and 44 minutes, in a symbolic act of defiance. ▶️The House’s approval came hours after the president quashed a rebellion among House Republicans who threatened to hold up what Trump calls his “big, beautiful bill”. ▶️ The president would sign the bill into law at 5pm on Friday in Washington, according to White House press secretary Karoline Leavitt, meeting his self-imposed deadline of July 4. ▶️ The legislation extends vast tax cuts from Trump’s first administration, paid for in part by steep cuts to Medicaid, the public health insurance scheme for low-income and disabled Americans, and other social welfare programmes. ▶️ The bill will also roll back Biden-era tax credits for clean energy, while scaling up investment in the military and funds for Trump’s crackdown on immigration. Source: FT (link to the article ▶️ https://lnkd.in/errs6gtu)

⚠️YOU CAN'T MAKE THIS UP

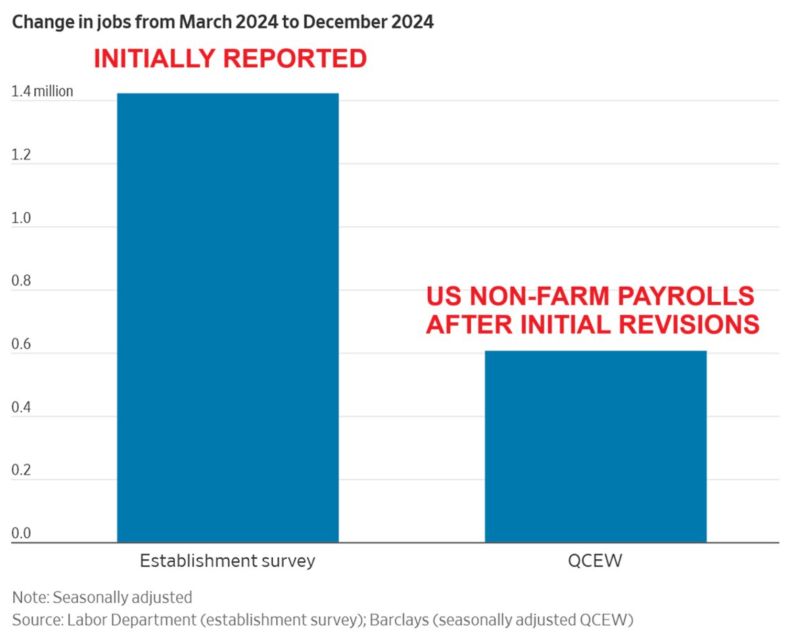

‼️ The US job numbers will likely be REVISED DOWN by nearly 800,000 for the 9-month period ending December 2024, according to QCEW data. ▶️ This means non-farm payrolls were OVERSTATED by ~88,888 jobs each month during this period. Source: Global Markets Investor