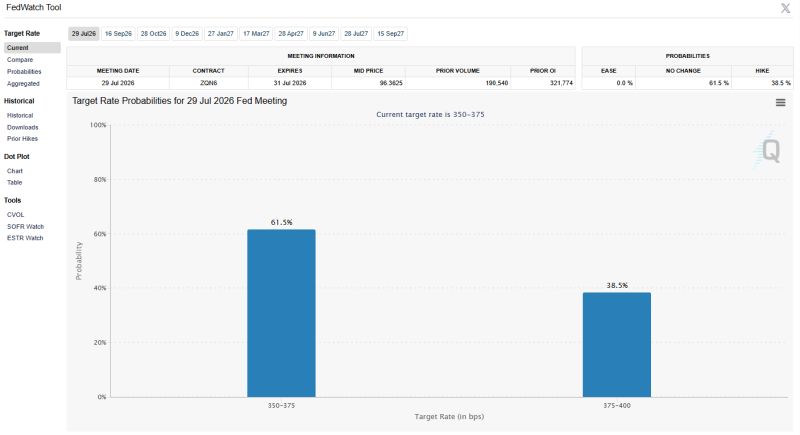

There is now a 38% chance of a rate hike at the July FOMC and a 0% chance of a rate cut

Source: Barchart

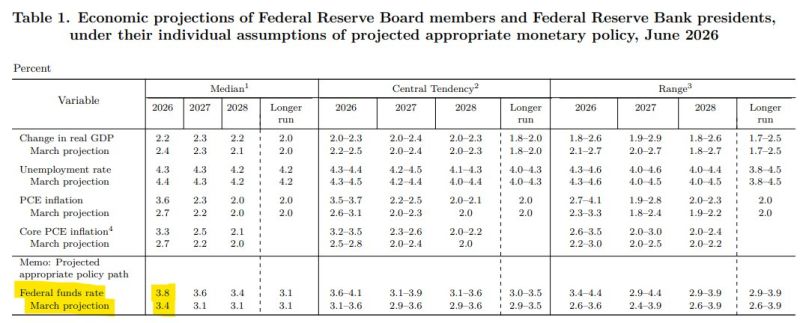

Big shift in Fed dot plots with the median member now forecasting 1 rate HIKE this year when previously they were forecasting 1 rate CUT. (Clone)

The stock market may not like it but this is the right move if the Fed wants to regain any credibility as an inflation fighter. Source: Charlie Bilello @charliebilello

Big shift in Fed dot plots with the median member now forecasting 1 rate HIKE this year when previously they were forecasting 1 rate CUT.

The stock market may not like it but this is the right move if the Fed wants to regain any credibility as an inflation fighter. Source: Charlie Bilello @charliebilello

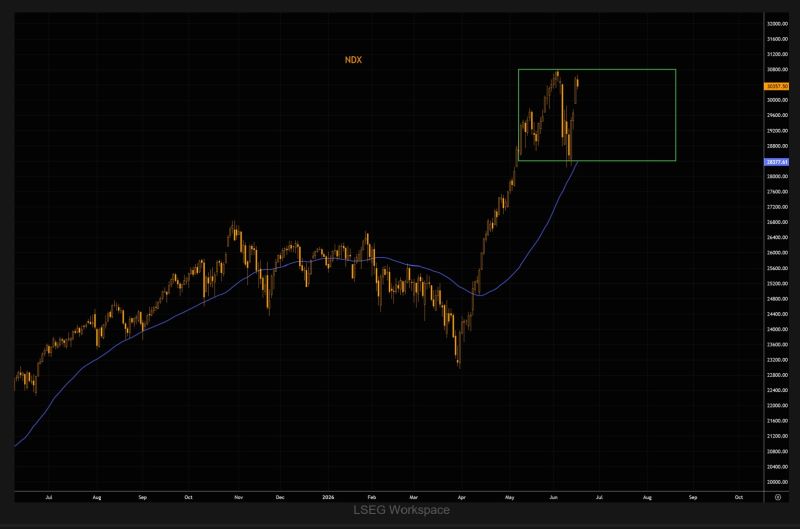

NASDAQ bounced on range lows and the 50-day moving average, only to reverse near range highs.

Massive moves, but no new direction. In a market like this, chasing breakouts has been one of the most expensive trades around. Source: TME

The U.S. Department of Justice (DOJ) has intervened in a lawsuit against Elon Musk's AI company, xAI, arguing that its Colossus 2 data center is critical to U.S. national security.

The NAACP sued xAI in April 2026 under the Clean Air Act, alleging the company was operating gas turbines without the necessary permits to power its AI facility. The turbines are located in Southaven, Mississippi, near the data center in Memphis, Tennessee. According to the lawsuit, the number of turbines has increased from 27 to 57 since the case was filed. xAI maintains that the turbines are exempt from Mississippi permitting requirements because they are mounted on trailers and classified as temporary mobile equipment. On Monday, the DOJ filed court documents arguing that shutting down the turbines could harm U.S. national, economic, and energy security. The department stated that the facility supports military AI capabilities. A declaration from the Defense Department's Chief Digital and AI Officer, Cameron Stanley, said Grok is one of only four AI models approved for mission-critical use on classified U.S. government networks and has been utilized in recent military operations involving Iran. The DOJ, xAI, and the State of Mississippi are jointly seeking dismissal of the lawsuit. Source: Bull Theory

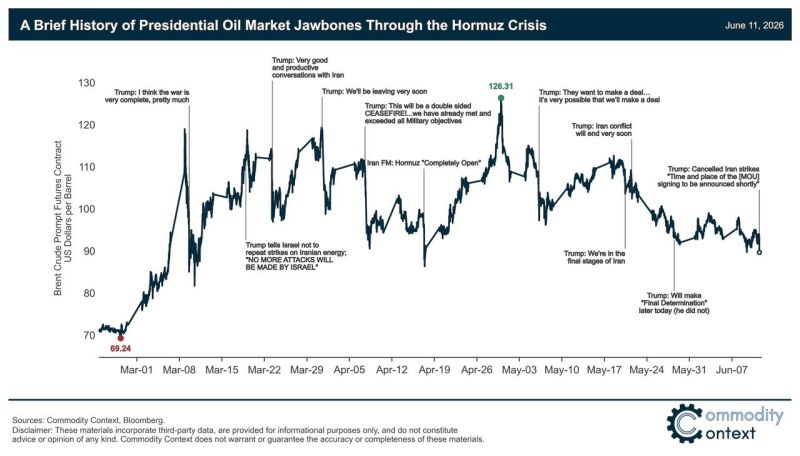

Here are the reported terms of the US-Iran peace deal MOU:

1. Immediate and permanent end to war on all fronts, including Lebanon 2. US naval blockade on Iranian ports lifted immediately 3. Strait of Hormuz to reopen within 30 days 4. US oil and petrochemical sanctions on Iran suspended 5. $24 billion in frozen Iranian assets released during 60-day negotiation period, $12 billion before talks even start 6. 60-day negotiation period for Iran's nuclear programme and full sanctions relief 7. Final signing in Geneva on June 19. JD Vance expected to attend The US disputes point 5, saying no funds will be released without Iran fulfilling commitments first.

Yesterday was a "TACO-Thursday", with Trump's rhetoric intraday-flipping from 'blowing the sh*t out of Iran' to a 'no strikes

Deal pretty much wrapped up' sparking a plunge in oil (ignoring denials), spike in stocks, and big drop in yields (shrugging off hot headline PPI and ECB rate-hikes). CNN reports that this is the 38th time that President Trump has declared a peace deal is imminent... Source: zerohedge

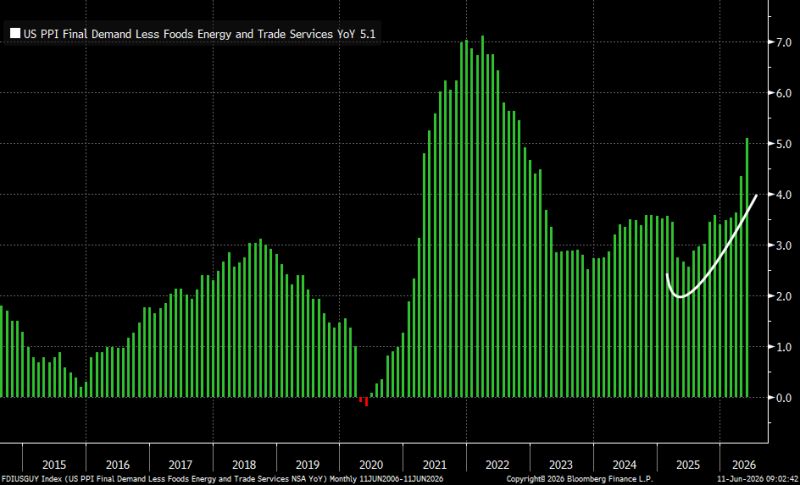

The SuperCore PPI (i.e., no food, energy or trade) has been accelerating for 11 months.

Source: Bernstein Advisors