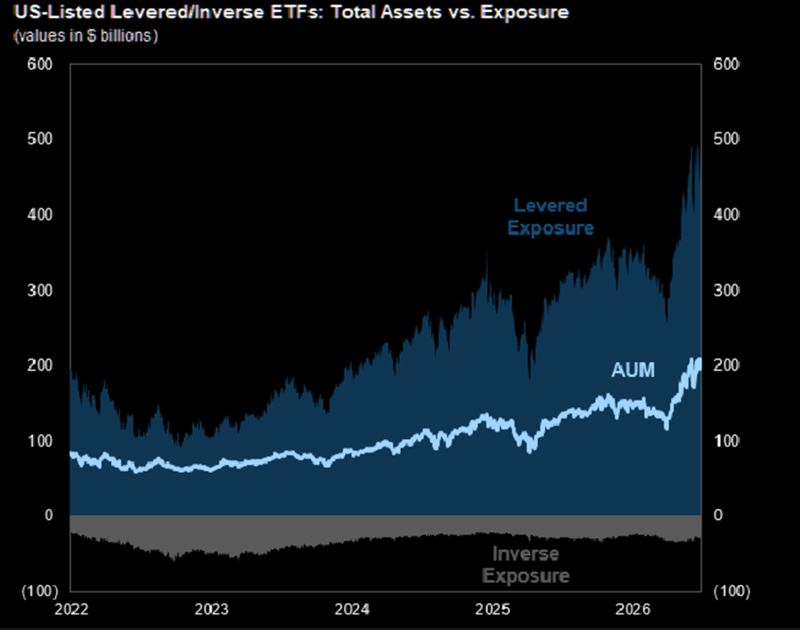

Leveraged ETFs are no longer a niche product.

US-listed funds now hold around $200 billion in assets, equivalent to roughly $400 billion of market exposure, while trading volumes are running about 50% above last year's record pace. Market structure increasingly matters. Source: TME, JP Morgan

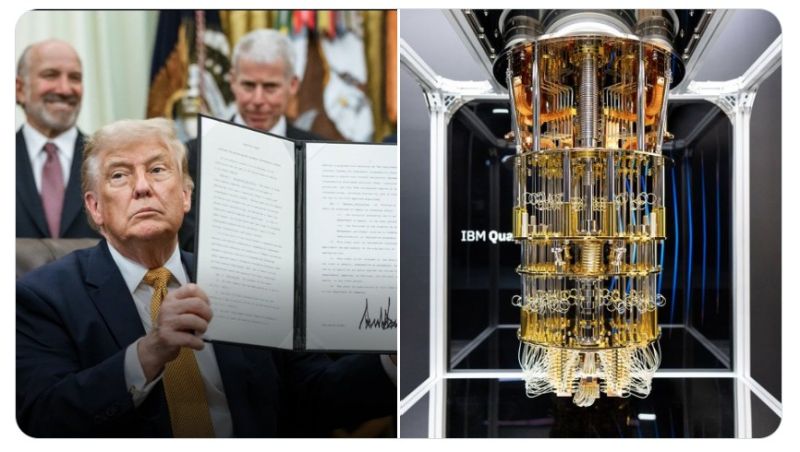

The U.S. just doubled down on quantum.

President Trump signed two executive orders to accelerate U.S. quantum technology and strengthen cybersecurity. The initiatives aim to develop a research-grade quantum computer by 2028, deploy quantum sensors and networks within five years, expand workforce training, and secure domestic supply chains. Federal systems are set to transition to post-quantum cryptography by 2031. These measures follow $2 billion in investments across nine quantum companies. The strategy highlights quantum technology’s growing importance for economic competitiveness, cybersecurity, national security, and global technological leadership.Source: Bull Theory

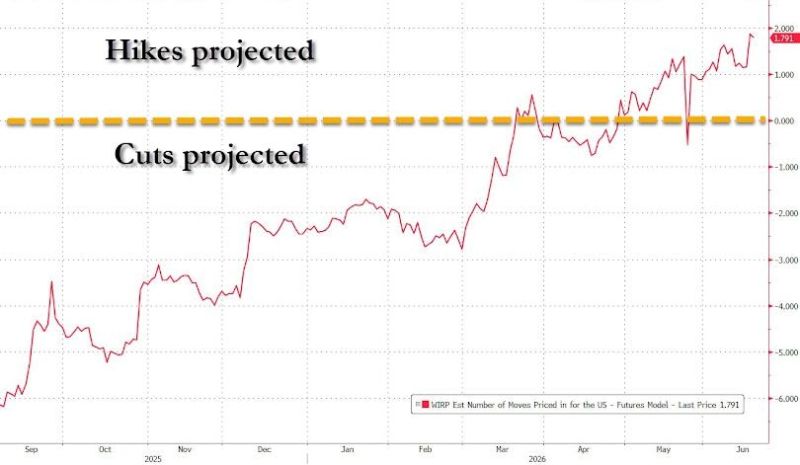

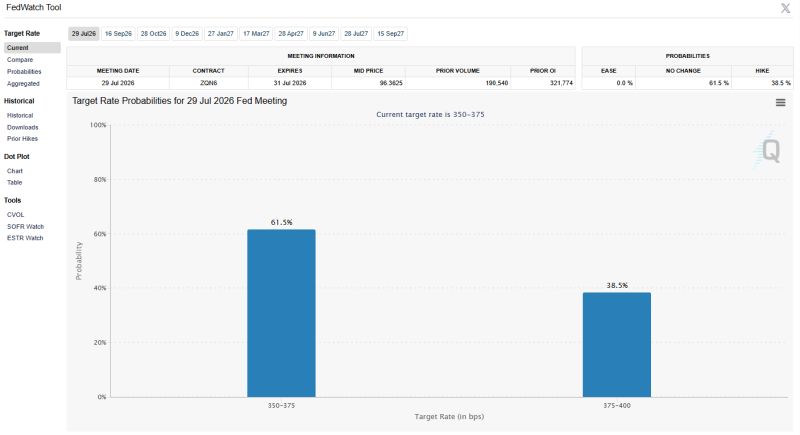

What a turnaround for Fed rates expectations (as implied by Futures). From projecting 6 cuts in September to 2 hikes now

Note that it didn't prevent equities to surge... Source: zerohedge, Bloomberg

There is now a 38% chance of a rate hike at the July FOMC and a 0% chance of a rate cut

Source: Barchart

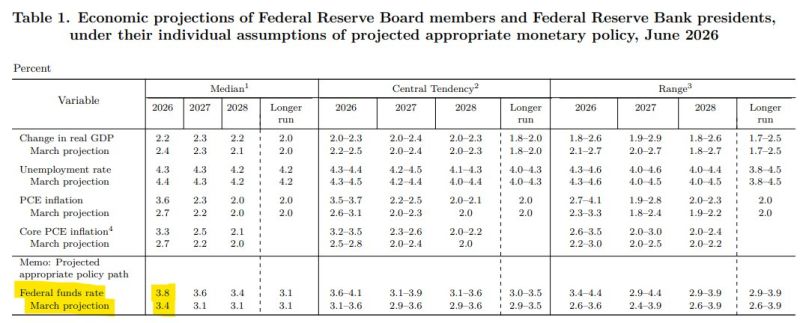

Big shift in Fed dot plots with the median member now forecasting 1 rate HIKE this year when previously they were forecasting 1 rate CUT. (Clone)

The stock market may not like it but this is the right move if the Fed wants to regain any credibility as an inflation fighter. Source: Charlie Bilello @charliebilello

Big shift in Fed dot plots with the median member now forecasting 1 rate HIKE this year when previously they were forecasting 1 rate CUT.

The stock market may not like it but this is the right move if the Fed wants to regain any credibility as an inflation fighter. Source: Charlie Bilello @charliebilello

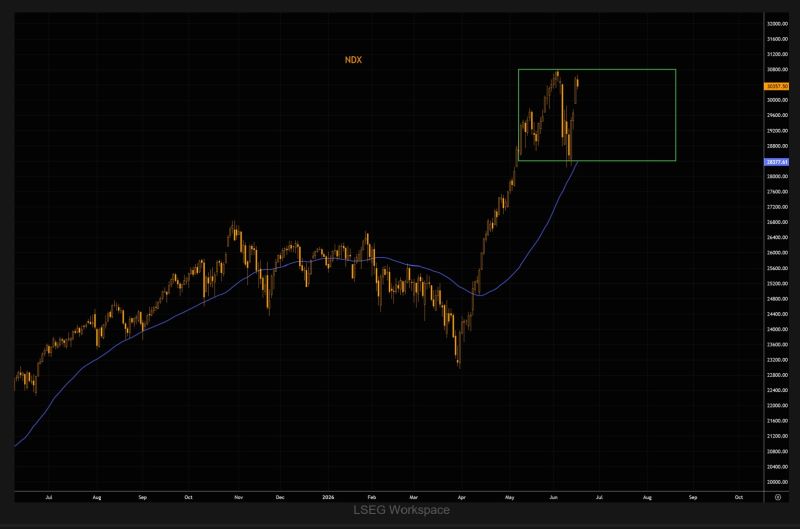

NASDAQ bounced on range lows and the 50-day moving average, only to reverse near range highs.

Massive moves, but no new direction. In a market like this, chasing breakouts has been one of the most expensive trades around. Source: TME

The U.S. Department of Justice (DOJ) has intervened in a lawsuit against Elon Musk's AI company, xAI, arguing that its Colossus 2 data center is critical to U.S. national security.

The NAACP sued xAI in April 2026 under the Clean Air Act, alleging the company was operating gas turbines without the necessary permits to power its AI facility. The turbines are located in Southaven, Mississippi, near the data center in Memphis, Tennessee. According to the lawsuit, the number of turbines has increased from 27 to 57 since the case was filed. xAI maintains that the turbines are exempt from Mississippi permitting requirements because they are mounted on trailers and classified as temporary mobile equipment. On Monday, the DOJ filed court documents arguing that shutting down the turbines could harm U.S. national, economic, and energy security. The department stated that the facility supports military AI capabilities. A declaration from the Defense Department's Chief Digital and AI Officer, Cameron Stanley, said Grok is one of only four AI models approved for mission-critical use on classified U.S. government networks and has been utilized in recent military operations involving Iran. The DOJ, xAI, and the State of Mississippi are jointly seeking dismissal of the lawsuit. Source: Bull Theory