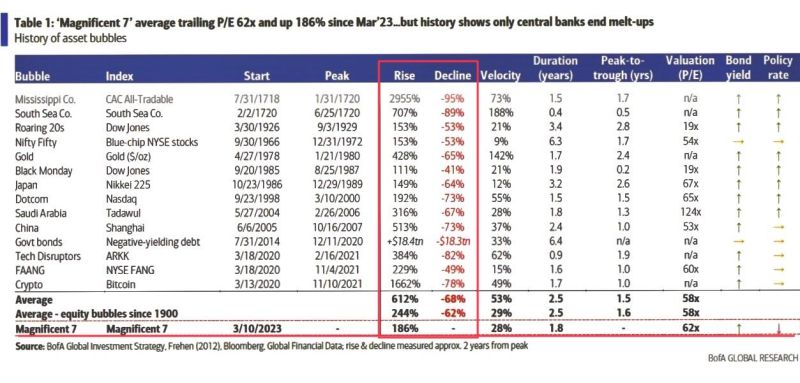

Historical asset bubble summary from BofA, including the current Mag7 frothiness.

”History shows only central banks end melt-ups”… Source: BofA, Wasteland Capital

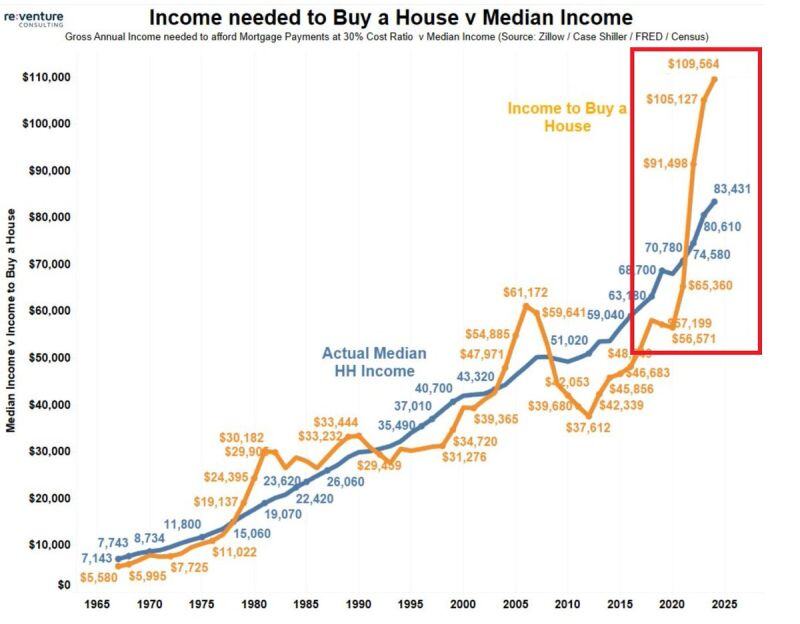

THE ISSUE WITH US HOUSING AFFORDABILITY IN ONE CHART...

Annual income needed to buy a house in the US hit a whopping $109,564, an all-time high. This has DOUBLED in just 4 years... At the same time, median income earned is just $83,431. The difference between the two has NEVER been greater. Source: Global Markets Investor

Apollo made a HUGE call on Sunday:

For the first time since the "Fed pivot" began, Apollo has officially declared inflation back on the rise. They warn of a potential repeat the 1970s as the Fed cuts rates into rising inflation. Apollo says the probability of the Fed RAISING interest rates in 2025 is now rising. Here's why: 👉 First, measures of inflation stickiness are all now well above the Fed's 2% target. In fact, the Atlanta Fed Core Sticky CPI index has leveled off near 4%. ALL major measures of CPI stickiness are now above 3%. 👉 Meanwhile, core CPI has levelled off at 3.3% fore multiple months in a row. This was "fine" because headline CPI was moving in a straight-line to 2% all year. However, as of the latest CPI inflation data, it's now RISING and back to 2.7%. Source: The Kobeissi Letter, Apollo

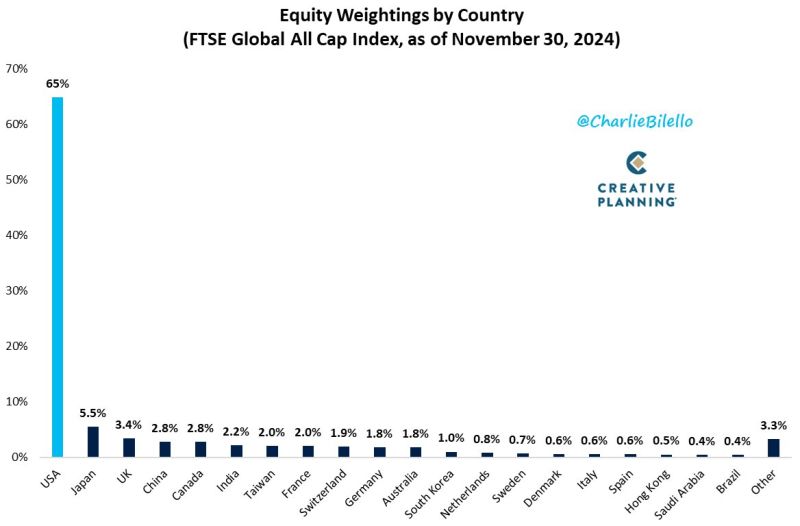

US stocks now make up 65% of the global equity market, their highest weighting in history.

This is more than 11x bigger than the second largest country by market cap (Japan at 5.5%). Source; Charlie Bilello

🚨 The S&P 500 P/E Ratios Heat Map.

What do you notice? $SPY Source: Jesse Cohen @JesseCohenInv

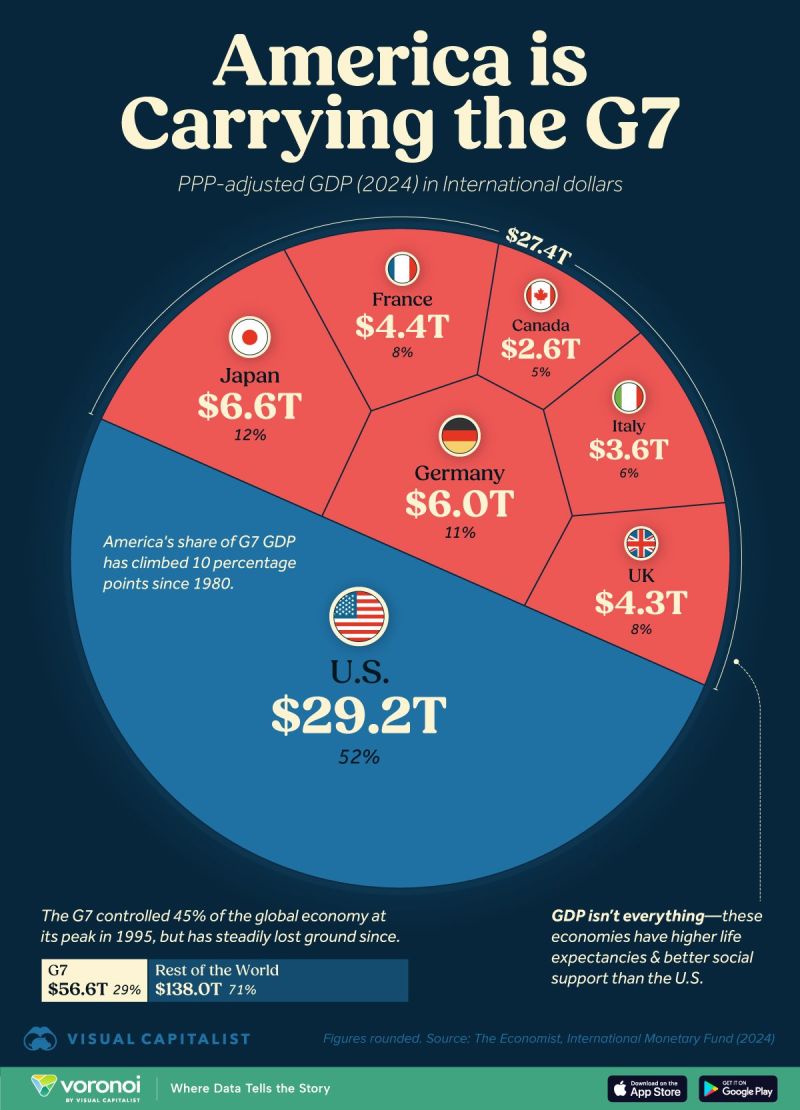

U.S. now accounts for 52% of the entire G7 GDP, up 10 percentage points since 1980.

Source: Visual Capitalist

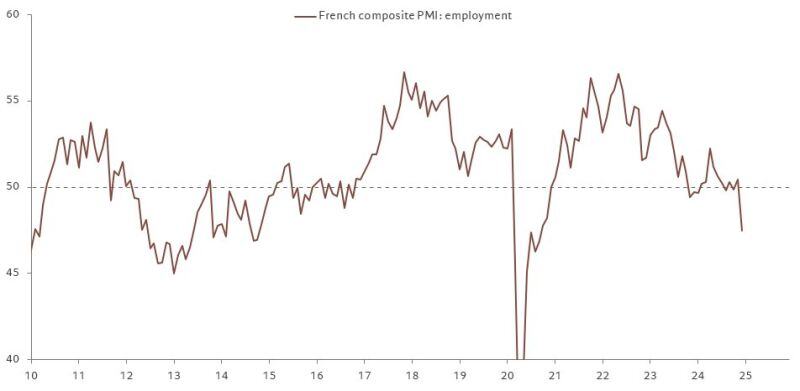

French PMI big warning:

The drop in employment was the largest since the pandemic, with the political situation often cited by firms as a reason to be downbeat. Source: Frederic Ducrozet

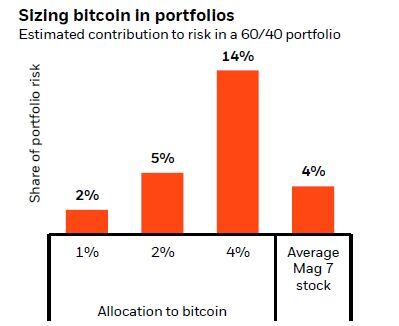

The case for a 2% Bitcoin allocation into multi-assets portfolios by Blackrock:

"So how can investors think about a bitcoin allocation? We take a risk budgeting approach: sizing the allocation based on how much it would contribute to total portfolio risk – measured by its long-run volatility and correlation to other assets (...). But from a portfolio construction perspective, it has some similarities with the “magnificent 7” group of mostly mega-cap tech stocks. Their market value – averaging $2.5 trillion in December 2024 – is similar to bitcoin’s (...) In a traditional portfolio with a mix of 60% stocks and 40% bonds, those seven stocks – if held at their current weights in the MSCI World – each account for 4% of the overall portfolio risk on average. That’s about the same share a 1-2% exposure to bitcoin would represent: Even though bitcoin’s correlation to other assets is relatively low, it’s more volatile, making its effect on total risk contribution similar overall. A bitcoin allocation would have the advantage of providing a diverse source of risk, while an overweight to the magnificent 7 would add to existing risk and to portfolio concentration. Why not more than 2%? A larger bitcoin allocation means its share of overall portfolio risk rises sharply. This effect is small when the allocation is small, but above 2% bitcoin’s share of total portfolio risk becomes outsized compared with the average magnificent 7 stock (...) . In an extreme case, should there no longer be any prospect of broad bitcoin adoption, the loss could be the entire 1-2% allocation. We think this is much less likely to happen to a magnificent 7 stock given these companies generate major cash flow and have tangible underlying assets. The upshot? By allocating no more than 2% to bitcoin, investors would: 1) introduce a very different source of return and risk; and 2) manage risk exposure to bitcoin".