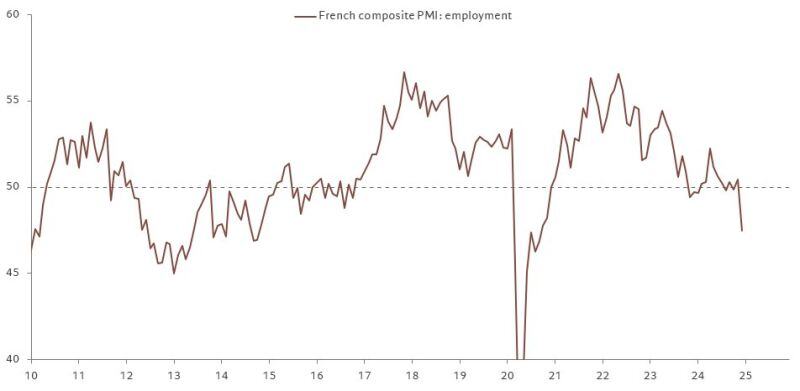

French PMI big warning:

The drop in employment was the largest since the pandemic, with the political situation often cited by firms as a reason to be downbeat. Source: Frederic Ducrozet

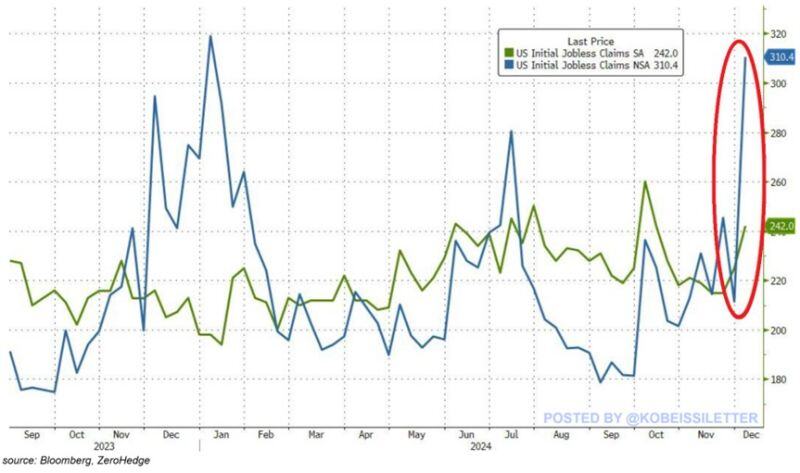

Has the era o stagflation begun?

Initial jobless claims spiked by 17,000 to 242,000 last week, the highest since the first week of October. Non-seasonally adjusted claims skyrocketed by 99,140 to 310,366, the highest since January. This marks a whopping 30% year-over-year increase. At the same time, the number of people receiving jobless benefits surged to 1.89 million, near the 3-year high. To put this into perspective, continuing jobless claims are now 14% above the 2018-2019 pre-pandemic levels. All while CPI, PCE, and PPI inflation are all back on the rise. We have a weakening labour market with rising inflation. Source: The Kobeissi Letter

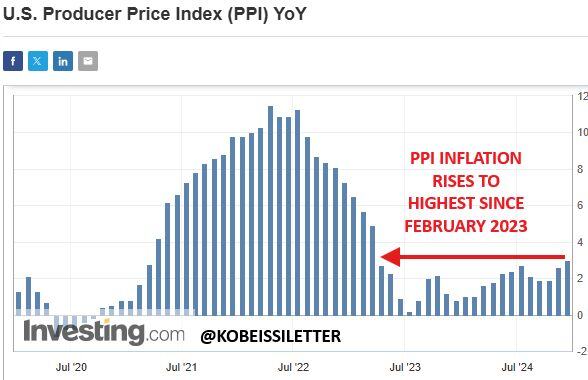

BREAKING: November PPI inflation RISES to 3.0%, above expectations of 2.6%. Core PPI inflation RISES to 3.4%, above expectations of 3.2%.

Moreover, the US Bureau of Labor Statistics has revised October PPI inflation HIGHER, from 2.4% to 2.6%. Also, Core PPI inflation for October has been revised HIGHER from 3.1% to 3.4%. This means that 6 out of the last 7 PPI inflation reports have now been revised higher. With today's 3.0% PPI inflation print, PPI inflation is now at its highest level since February 2023. CPI, PPI, and PCE inflation are all officially back on the rise in the United States... Source: The Kobeissi Letter

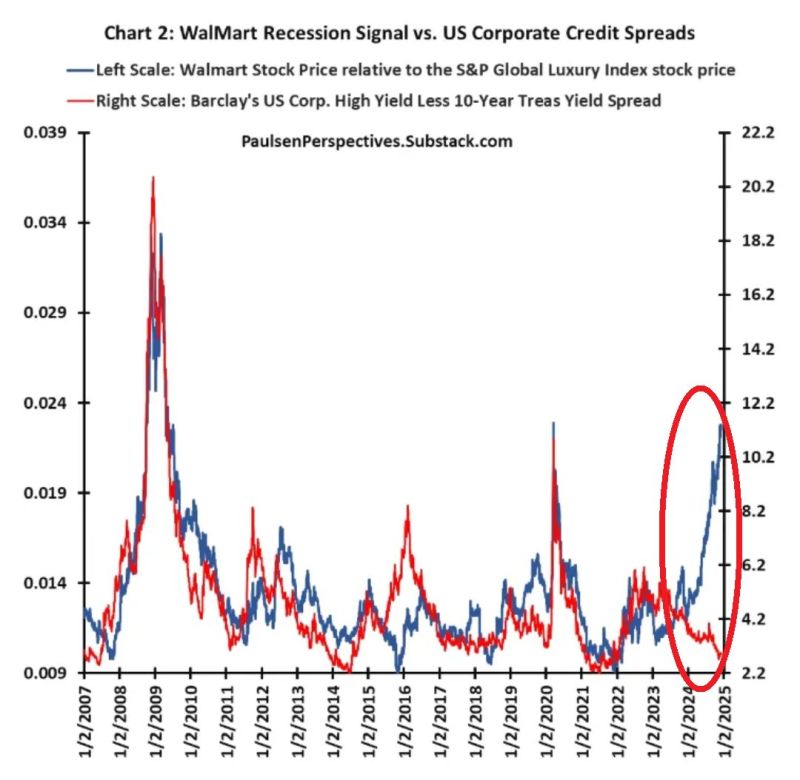

⁉️ WALMART RECESSION SIGNAL IS FLASHING RED BUT CREDIT SPREADS ARE AT THE TIGHTEST. WHO'S RIGHT ?

Walmart, $WMT, share price divided by the S&P Global Luxury Index price jumped to near the highest since the 2008 Financial Crisis. However, US corporate bond spreads stay at historically low levels. Is this indicator still valid? Source: Global Markets Investor

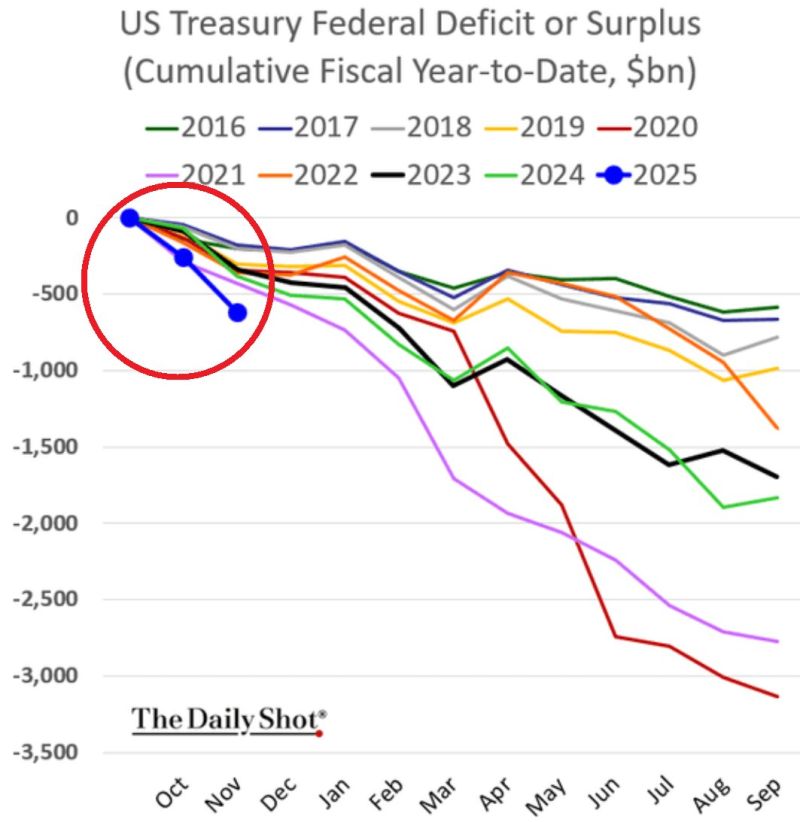

‼️ US budget deficit hit a GIGANTIC $367 BILLION in November 2024.

This puts the total deficit for the first 2 months of the Fiscal Year 2025 to a TREMENDOUS $624 BILLION, the highest EVER. This has even surpassed the 2020 CRISIS LEVELS. Source: Global Markets Investor, The Daily Shot

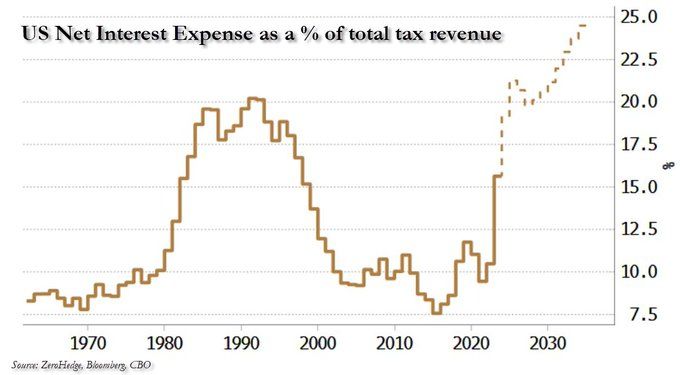

US net interest expense is 15% of tax revenue, it will rise to 25% in 2035 according to the CBO...

It will get there much faster if the Fed starts hiking rates again Source: zerohedge

🚨 JUST IN: CANADA SLASHES RATES BY 50 BPS

Fifth cut in a row... Dropping the policy rate from 5% to 3.25% in 2024—150 bps total. But it’s not working fast enough: -Unemployment: 6.8% (highest in 8 years). -GDP per capita: Down 6 straight quarters. -Canadian Dollar $CAD at 4.5-year low -Former BOC Governor says “We’re already in a recession.” Market is pricing in another ~50bps of cuts by July 2025 ➡️ 2.75% overnight rate. Source: Genevieve Roch-Decter, CFA, Bloomberg

Swiss National Bank (SNB) halved its interest rate with 50bps cut,

in the current context of weak inflation, upward pressures on the Swiss franc and worrying dynamics in neighboring European countries. The 50bp rate cut is half-a-surprise for financial markets, that were not fully convinced of the possibility of such large movement and were rather pricing a 25bp rate cut. swiss franc initially weakened 0.5% vs the Euro. But it is already back to 0.93. OUR TAKE (based on our Chief Economist Adrien Pichoud views) 👉 Swiss CPI inflation has slipped below 1% in the 4th quarter of 2024 (+0.7% in November) and it is expected to slow further in 2025. The SNB expects inflation to hover just above zero (+0.2%/+0.3%) for most of next year before picking up slightly as 2026 draws near. By averaging +0.3% in 2025, the inflation rate would be at the very bottom of the 0-to-2% range that the SNB targets. 👉 As the Swiss economy faces headwinds from the strength of the Swiss franc and the weakness of economic activity in Germany and most other European economies, monetary policy has no reason to be restrictive and had to be adjusted. After today’s rate cut, the monetary policy stance is about neutral (with a real short-term rate close to 0%). 👉 Looking ahead, more rate cuts are to be expected in 2025. We expect the CHF short-term rate to be lowered to 0.0% by June next year, with 25bp rate cuts at the March and June meetings. 👉 Will Switzerland move back to NEGATIVE RATES? This is not our scenario at this stage, even if it wasn’t ruled out by Mr Schlegel recently. Potential undue upward pressures on the CHF will then likely be addressed with interventions on the FX market and a possible expansion of the SNB’s balance sheet size. It would require a significant deterioration in global growth and inflation dynamics next year for the SNB to be pushed back into negative interest rate policies. Source chart: Bloomberg