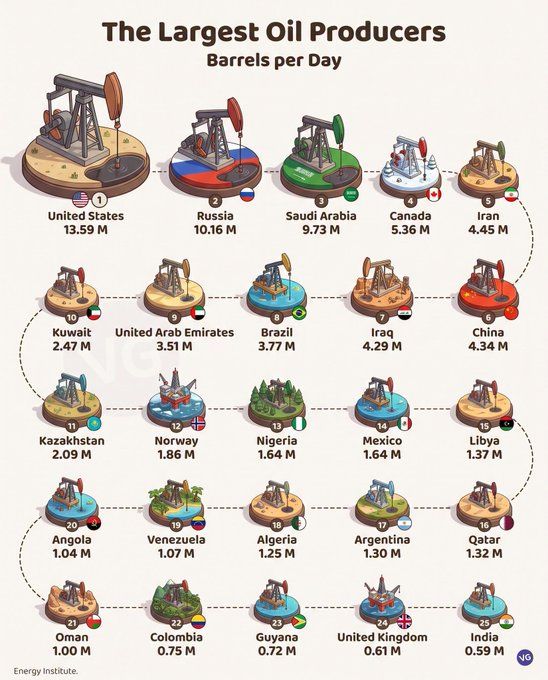

US produces 13.59 million barrels a day.

That is more than Russia and Saudi Arabia , at 10.16 million and 9.73 million. It is nearly triple Iran's 4.45 million. America is not just the largest oil producer on earth, it is exporting record volumes of that supply overseas. Source: Jack Prandelli on X

SK Hynix last 5 days "price discovery"

8/3: -11.47% 7/31: +26.42% 7/30: -3.62% 7/29: -7.54% 7/28: -16.16% Source: zerohedge

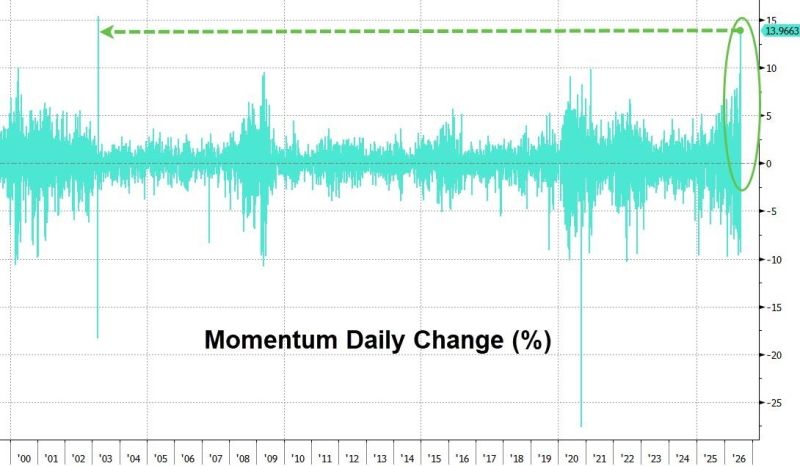

Yesterday saw Momentum's single-biggest daily gain since 2003...

Source: zerohedge

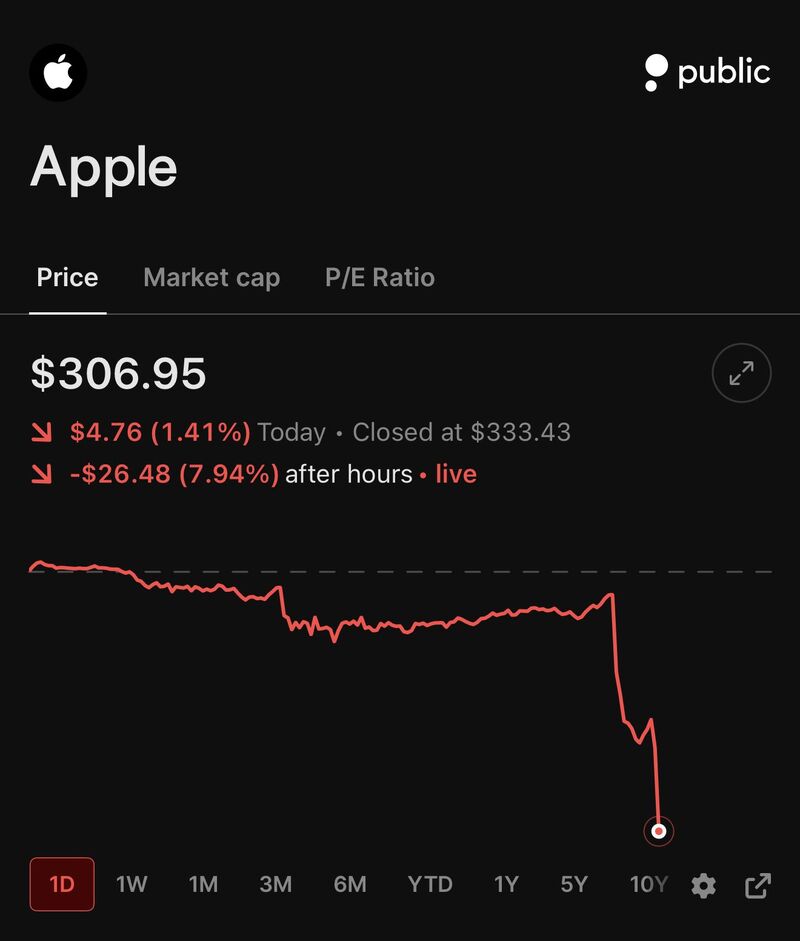

APPLE $AAPL IS DOWN NEARLY 8% AFTER HOURS DESPITE BEATING ON REVENUE AND EPS

The quarter itself was strong: • Revenue: $109.42B, beating expectations of $108.65B • EPS: $2.02, beating expectations of $1.89 • iPhone revenue: +22% Y/Y, its best growth in years The guidance may be what sold off: • September quarter revenue guided to 9%-11% growth, a slowdown from Q3's 16% • Gross margin guided down to 47%-48% from the 50.1% just reported • Services missed expectations, and Greater China came in below estimates Apple came into the print at 35x forward earnings, well above its 5-year average of 28, and up 22% YTD. At that valuation, a beat wasn't enough. Source: WOLF

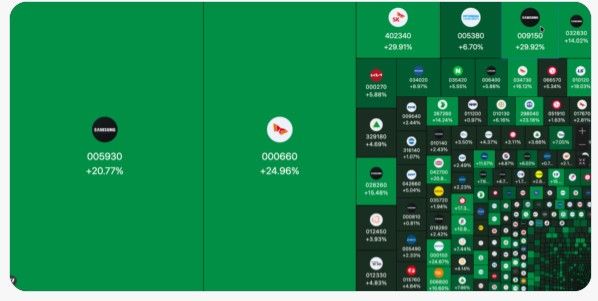

MASSIVE REVERSAL IN SOUTH KOREA

₩720 trillion has been added to Korean market today as KOSPI surged 16%. Samsung is up 20% SkHynix is up 25% Source: The Macro paper

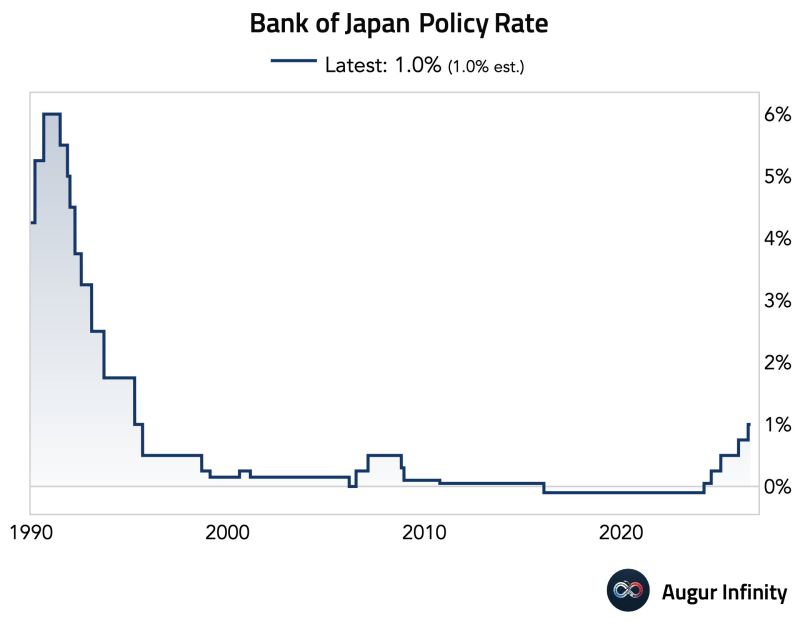

Bank of Japan ) keeps rates unchanged at 1% However, it warned that core inflation was likely to exceed its 2% target from September.

The move comes as Japan reportedly conducted an intervention to strengthen the yen on Thursday night. • The Bank of Japan kept its policy rate unchanged at 1% in an 8-1 vote on Friday, in line with market expectations, after raising rates to their highest level since 1995 last month. • Board member Naoki Takata dissented, calling for an immediate 25-basis-point hike, citing upside inflation risks and changing global financial conditions. • The BOJ said it will continue to raise rates if economic activity, inflation and financial conditions evolve as expected, adding that underlying inflation is now close to its 2% target. • In its latest outlook, the central bank lowered its FY2026 core CPI forecast to 2.5% from 2.8% and raised its FY2026 GDP growth forecast to 0.6% from 0.5%. FY2027 GDP growth forecast is raised to 0.8% from 0.7% 🏦BoJ Says: Significant downside risks to economy activity & significant upside risks to prices have decreased. In its outlook, the BOJ said that core inflation was likely to accelerate to a level “clearly above” 2% from the second half of its 2026 fiscal year, which runs from September to March. It cited wage increases being passed along into selling prices, the rise in crude oil prices and the recent depreciation of the yen. Inflation should then come down toward 2% as crude oil prices decline, it said. Japan’s core inflation for July came in at 1.6%, and has been below 2% for most of 2026. The decision comes as Tokyo reportedly conducted an intervention on Thursday night, in conjunction with U.S. authorities executing a “rate check,” a move usually seen as a precursor to intervention. Peter Schiff: "The BoJ’s decision to hold rates at 1%, with only the possibility of a quarter-point hike by year-end, ensures a weaker yen, rising inflation, and higher long-term interest rates, ultimately forcing the BoJ to hike much more in the future, with even more adverse consequences". Source: Augur Infinity

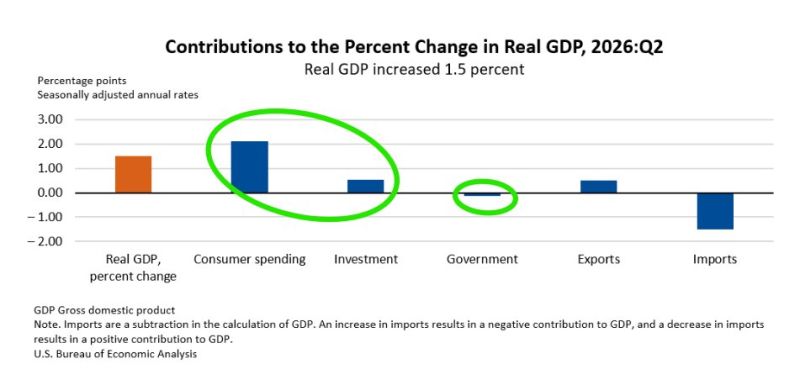

In case you missed it... US Q2 GDP came in at +1.5% vs. expectations of +2.1%

While it looks as a miss, let's keep in mind that underlying private domestic demand was strong, with real final sales to private domestic purchasers rising 3.9 percent in Q2 from 1.7 percent in Q1, showing solid private-sector momentum despite the "softer" headline GDP. More importantly, government spending fell. Source: Daniel Lacalle

$AMZN Q2 earnings blew past Wall Street's expectations with strong AWS revenue. Stock is up nearly +10% after-hours

Source: Yahoo Finance