🚨 S&P500 erased $1.8 TRILLION of market cap on Fed "hawkish cut".

‼️ Big Tech, Bonds, Bullion and Bitcoin fell sharply after the Fed cuts rates by 25 basis points - which is exactly what 97% of market participants expected. So what happened❓ 👉 Actually, today's market reaction had NOTHING to do with the rate decision. Rather, it would about the Fed's outlook for 2025 which shifted SHARPLY in the hawkish direction. 👉Indeed, the hashtag#Fed reduced their outlook from 3 to 2 rate cuts in 2025. 👉Furthermore, the Fed now sees hashtag#inflation at 2.1% at the end of 2026, still slightly above their 2.0% target. ⚠️ The stock market's decline accelerated after Powell said one specific sentence in his press conference today: "Today was a closer call but we decided it was the right call." ⚠️The US Dollar surged to its highest since November 2022 after he said that. Clearly, the Fed has acknowledged that inflation is an issue, once again. ⚠️On top of this, Cleveland Fed President Beth Hammack dissented in today's decision. 1 out of 19 Fed officials sees no rate cuts in 2025 and 3 officials see just 2 rate cuts. Only 5 Fed officials currently see 3 or more interest rate cuts in 2025 in a sudden hawkish shift. This led to what appears to have been the biggest panic sell in the market since the Yen carry trade collapsed. Small cap stocks fell nearly 5% today and the Dow posted a 10-day losing streak for the first time since 1974. Sentiment is shifting as we look into 2025.

⚡ Foreign holdings allocation to US stocks hit nearly 60%, a record.

This share has more than DOUBLED over the last 15 years. Allocation to equities exceeds the levels seen at the 2000 Dot-Com Bubble peak Foreigners are all-in on US stocks. Chart: @topdowncharts thru Global Markets Investors

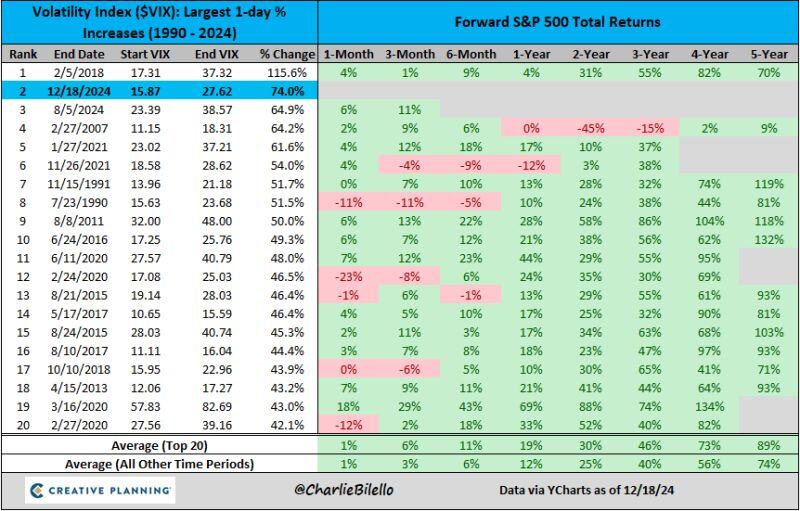

The $VIX spiked 74% higher yesterday, the 2nd biggest 1-day % increase in history

Volatility is back. Source Charlie Bilello

🔈 BANK OF JAPAN JUST MADE THEIR INTEREST RATE DECISION: THEY WILL NOT BE RAISING INTEREST RATES. This is a relief for markets 👍

🚨 If Japan hiked rates, the US Dollar would weaken against the Yen. Anyone who is short the Yen then would have to sell off US equities in order to cover their short, which could've caused a decline in stocks. Most of those stocks would have been tech stocks. It also could have caused a sell off in Bitcoin as many people have borrowed against the Yen to put money into crypto. Basically it would be another edition of the Yen Carry trade which still has trillions of dollars tied into it. 😊 On a day like today, bulls really needed Japan to NOT raise rates. USD/JPY after the decision, up 0.27% Source: @amitisinvesting

🚨FROM THE MOST EUPHORIC MARKET IN HISTORY TO A COMPLETE BLOODBATH IN 2 HOURS🚨

US stocks, Gold and Bitcoin massacred after the Fed cut rates by 0.25% and expect fewer cuts in 2025 and 2026 due to inflation concerns. VIX and US dollar spiked. Performance yesterday: S&P 500 -3.0% - biggest drop since March 2020 CRASH Nasdaq -3.6% Russell 2000 -4.7% Dow Jones -2.6% Bitcoin -5.5% Bank Index -4.2% VIX +54% front mth futures VIX +17% Gold -2.2% Silver -3.3% WTI Crude Oil -0.9% Source: Bloomberg, Global Markets Investor

US BANKS UNDER PRESSURE

With Powell stating that there won’t be significant rate cuts next year and the yield curve un- inverting along with BTFP going away banks were hammered yesterday as most of them have BILLIONS worth of unrealized LOSSES in BONDS. Source: The Coastal Journal

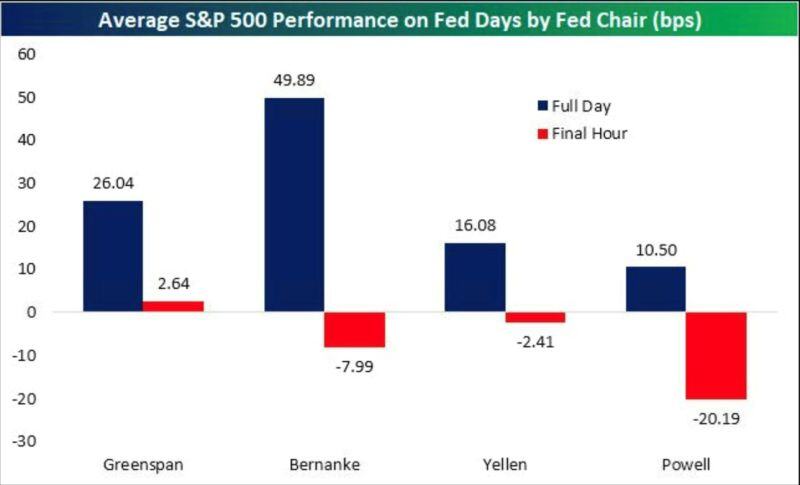

Powell is second to none when it comes to market reaction on Fed day.

He lived up to his reputation and track record yesterday. To say the least... Source: Bespoke

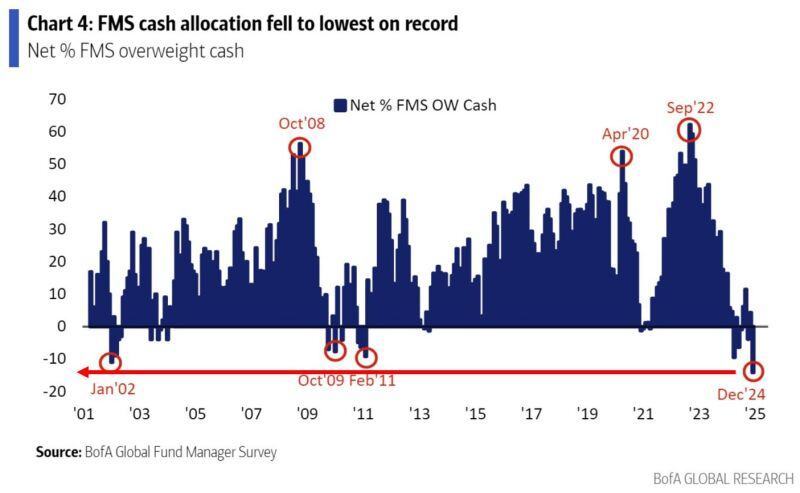

‼️AHEAD OF THE FED MEETING YESTERDAY, INSTITUTIONAL INVESTORS WERE ALL-IN ON US STOCKS AND CASH ALLOCATION AT RECORD LOW ‼️

Institutional investors* cash allocation hit the lowest level ON RECORD. This comes as allocation to US equities hit a RECORD HIGH. What will happen when stocks begin to drop? *171 Fund Managers with $450 billion in assets Source: BofA, Global Markets Investor