He did it again... Over $495,100,000 have been liquidated from the crypto markets within the last 24 hours.

This is the single largest Bitcoin liquidation event in history, just days after Jim Cramer told investors to buy and called $BTC a winner... More seriously some pullback / profit taking was long due... but the market is taking the habit of going short Jim Cramer's view Source: Jacob King

JUST IN: 'America elected the most pro-crypto Congress ever with almost 300 pro-crypto elected to the House and Senate - CNBC

Crypto execs, investors and evangelists saw the election as existential to an industry that spent the past four years simultaneously trying to grow up while being repeatedly beaten down. In total, crypto-related PACs and other groups tied to the industry reeled in over $245 million, according to Federal Election Commission data. Nearly 300 pro-crypto lawmakers will take seats in the House and Senate, according to Stand With Crypto, giving the sector unprecedented influence over the legislative agenda. Link to CNBC article >>> https://lnkd.in/euj8FDqN

Elon Musk, CEO of Tesla, praised India's election process for its speed.

Musk was responding to a post, highlighting how India counted 640 million votes in a single day.

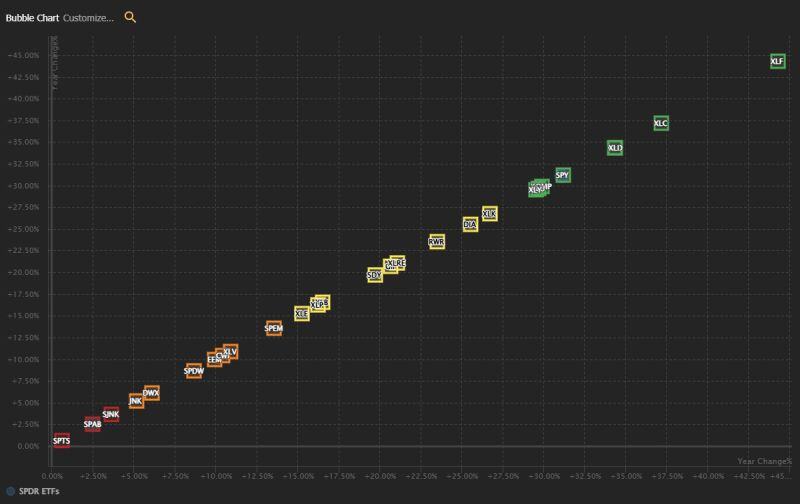

SPDR ETFs and their YTD Performance

🥇 Financials $XLF +44.28% 🥈 Communication Services $XLC +37.19% 🥉 Gold Trust $GLD +34.37% Source: Trend Spider

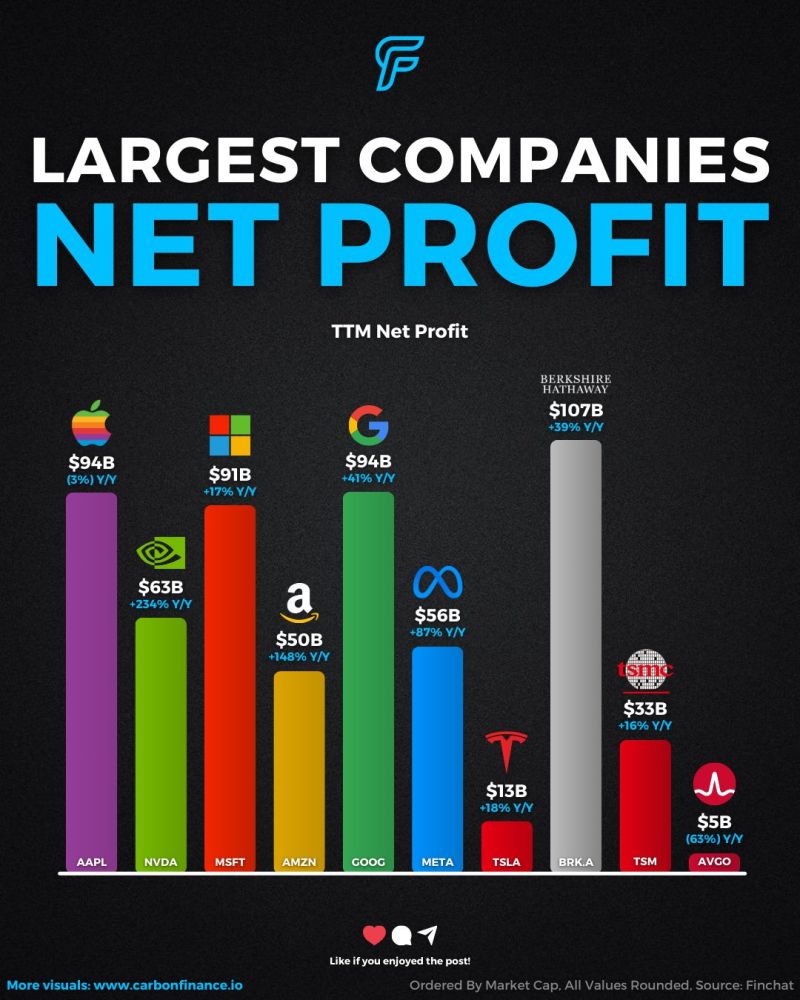

The giants of the U.S. economy are absolute cash machines.

Here’s their TTM (trailing-twelve-months) net income (and Y/Y growth): $AAPL: $94B (-3%) $NVDA: $63B (+234%) $MSFT: $91B (+17%) $AMZN: $50B (+148%) $GOOG: $94B (+41%) $META: $56B (+87%) $TSLA: $13B (+18%) $BRK.A: $107B (+39%)* $TSM: $33B (+16%) $AVGO: $5B (-63%) *Note: Berkshire's net income includes unrealized gains from its massive investment portfolio. These 10 alone earned $606B this year. Will they continue to grow their profit at similar rates moving forward?

Should pension funds invest in Crypto?

The Times @CoinCornerDanny makes the case for YES!! The "Times" are changing... Source: Bitcoin Magazine

How will this end?

Source: Jim Bianco

It has been a very quiet year... Can we expect the same in 2025??? (Clone)

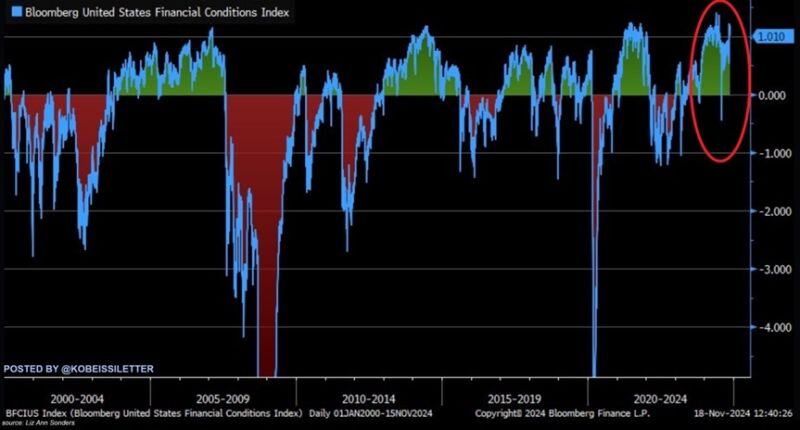

Financial conditions are now even easier than previous records seen in late 2020 and 2021. In fact, this makes financial conditions easier than when the Fed cut rates to near 0% overnight in 2020. Meanwhile, the market is pricing in a 59% chance of another 25 bps Fed rate cut in December. Source: The Kobeissi Letter, Bloomberg