5 Aug 2024

A worrying divergence...

Source: J-C Parets

2 Aug 2024

BREAKING: The 10-Year Note Yield has dropped below 4.00% for the first time since February 2024.

This comes after the July Fed meeting and ISM manufacturing data came in weaker than expected. Markets expect the first Fed rate cut since March 2020 to come at their next meeting, in September 2024. Over the last week, the 10-Year Note Yield is now down over 30 basis points. Source: The Kobeissi Letter

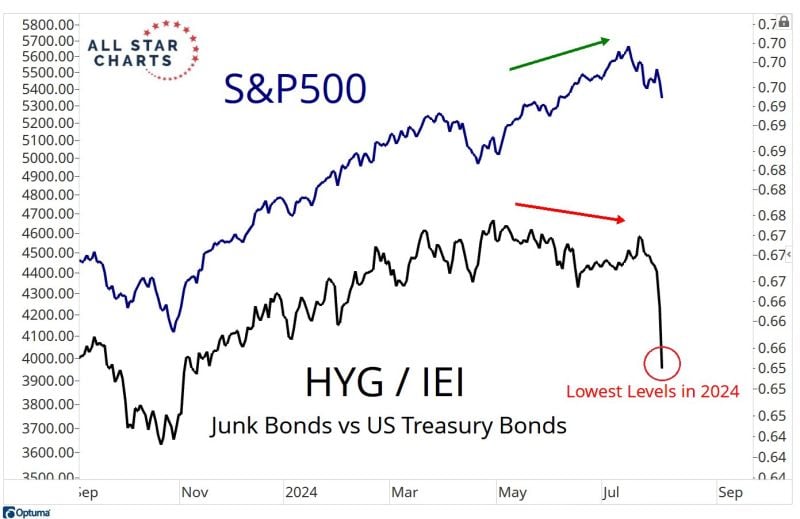

29 Jul 2024

Junk bonds closed at an ATH (total return) last week $HYG

Source: Mike Z.

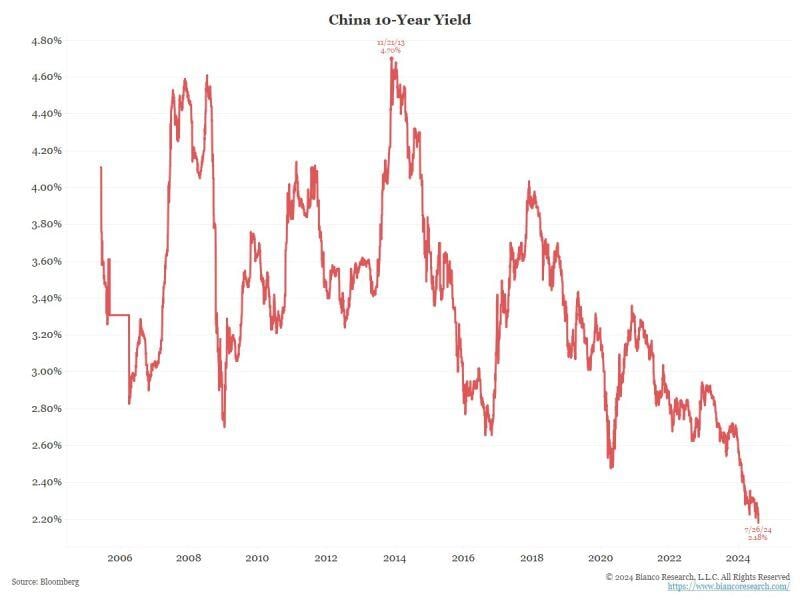

26 Jul 2024

CHINA 10-YEAR YIELD FALLS TO A FRESH RECORD LOW

So, what is the Chinese bond market signaling about the Chinese economy? Source: Bianco research

25 Jul 2024

The steepening trade continues with US 2s/30s yield spread jumping to 12bps, the highest since 2022.

Source: Bloomberg, HolgerZ

22 Jul 2024

Speculators have ramped up their bets against long-dated US bonds due to the rising prospects of Trump 2.0.

Source: Bloomberg, HolgerZ

19 Jul 2024

The US dollar index $DXY and the 10-year yield $TNX are both breaking down.

Source: Steven Strazza, All Star Charts

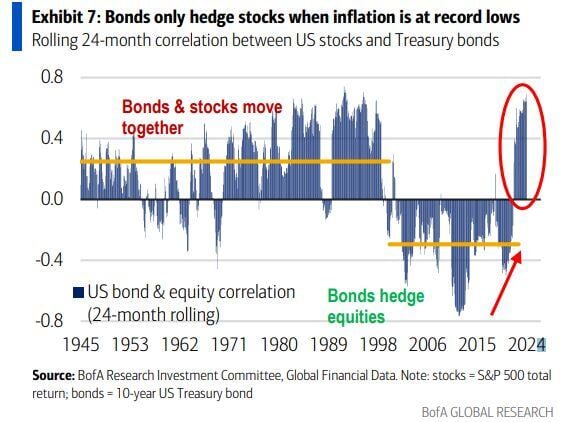

18 Jul 2024

Historically, bonds acted as efficient portfolio hedges only when inflation is <2%.

Below is the rolling 24-month correlation between US stocks and Treasury bonds. Source: Mike Zaccardi