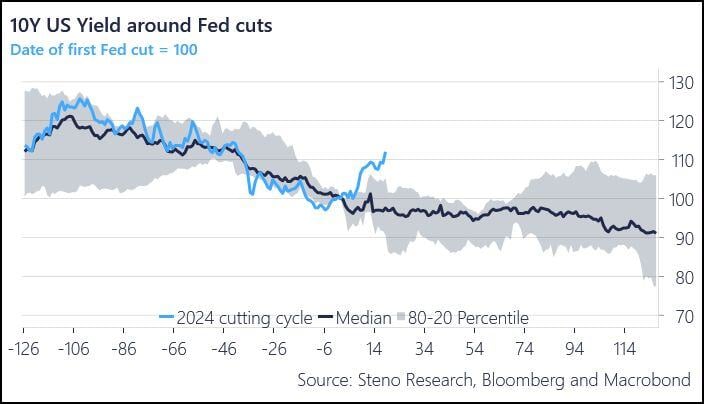

The move in bond yields after the 50bp cut is very out of the ordinary.

Source: Andreas Steno Larsen @AndreasSteno on X

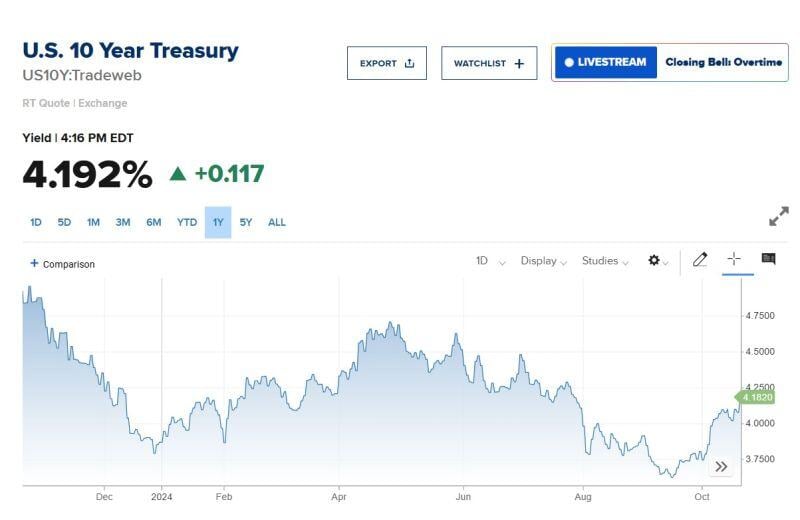

The 10 year bond yield soared on Monday, closing i on 4.2%.

The rise in bond yields took stocks down with them. Has the Fed lost control of the bond market? Was the Fed jumbo rate cut a policy mistake?

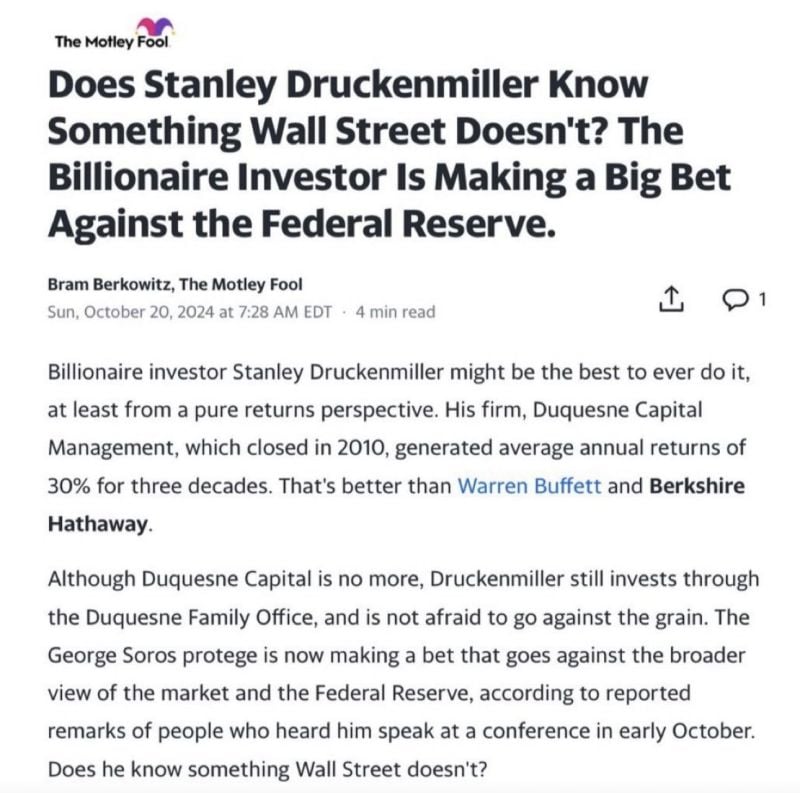

Druckenmiller is shorting U.S. Treasuries with a record setting 20% of his portfolio.

He knows what's about to happen ("Interest rates could double from here.") Source: Financelot @FinanceLancelot on X

A fascinating chart by James Bianco ->

The 10-year yield (blue) and Trump's Political Betting probabilities (orange). The chart starts the day Biden dropped out. Coincidence, or are these series related? If they are related, what happens to 10-year yields if the orange line (man) goes to 100 in 14 days? Source: Bianco Research

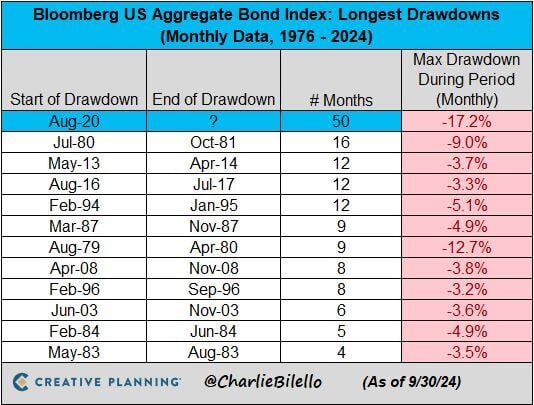

The US Bond Market has now been in a drawdown for over 50 months, by far the longest in history.

Source: Charlie Bilello

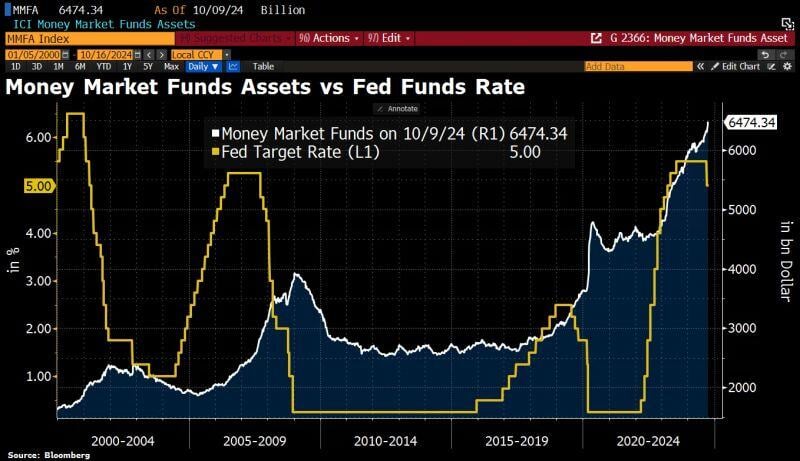

Mind the gap: Assets in US money market funds have hit a fresh ATH at $6.5tn, although the relevant Fed Funds Rates have fallen and are likely to fall further.

Note however that the "relative" figures (i.e money market funds AuMs as a % of total assets AuMs) currently stand at all-time low whereas equities weight is at all-time high... Source. Bloomberg, HolgerZ

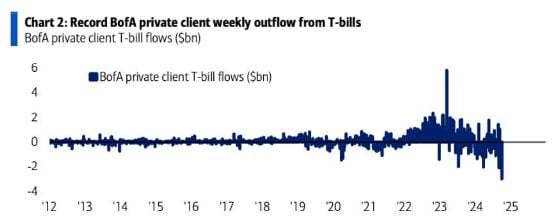

Investors sold the most amount of Treasury Bills in history this week

Source: Bank of America

US Yields back at 4% for the first time since August

Monday 7th of october 2024 recent yields move US Treasury 2yrs and 10yrs