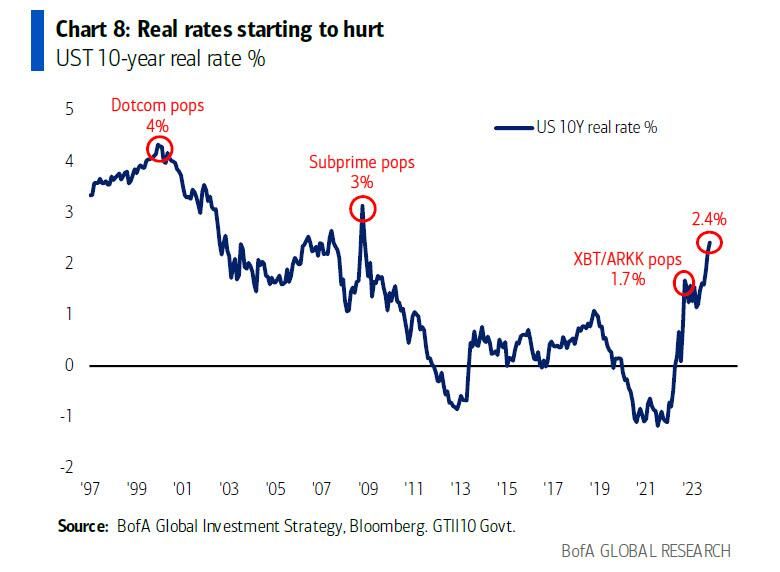

Rising real rates are going to inflict real pain on a variety of asset classes, particularly longer duration risk

BofA, Markets & Mayhem 🤖

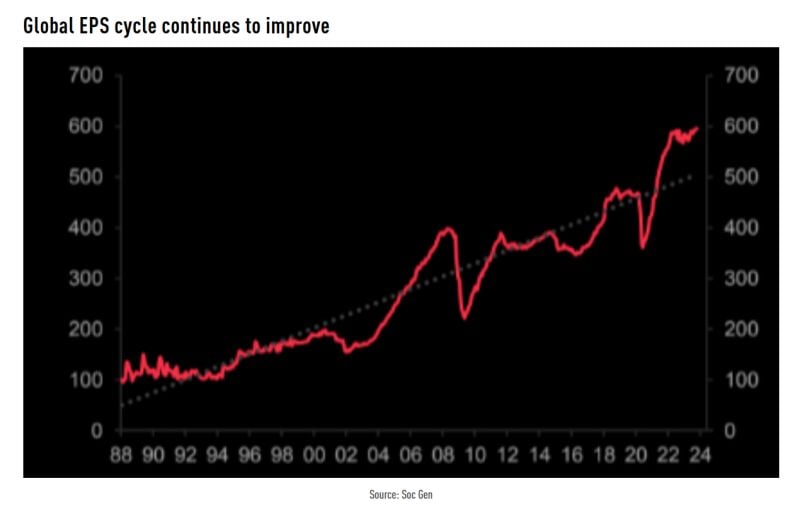

The global EPS cycle continues to improve, with nominal GDP growth continuing to support the cycle

Source: SocGen, TME

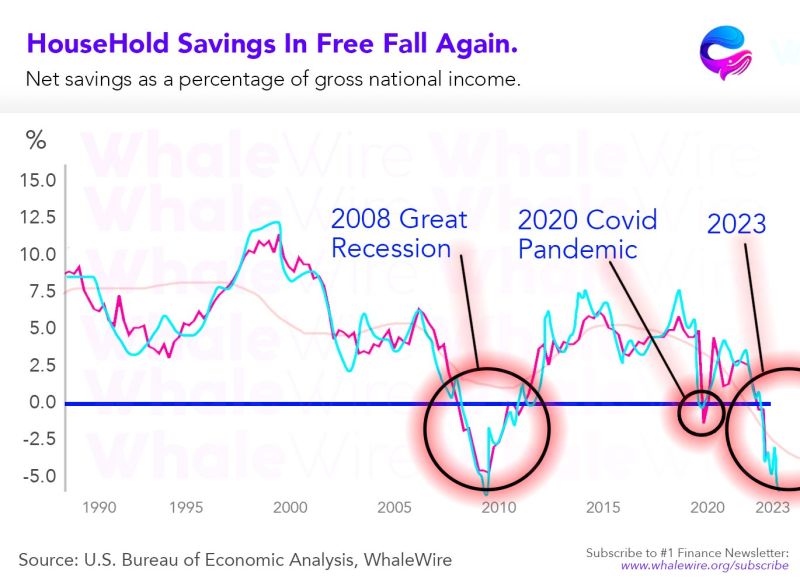

In the last 8 decades, savings as a percentage of national income has ONLY contracted three times:

2008 - Great Recession. 2020 - Covid Pandemic Crash. 2023 - The Everything Bubble. Source: Whalewire

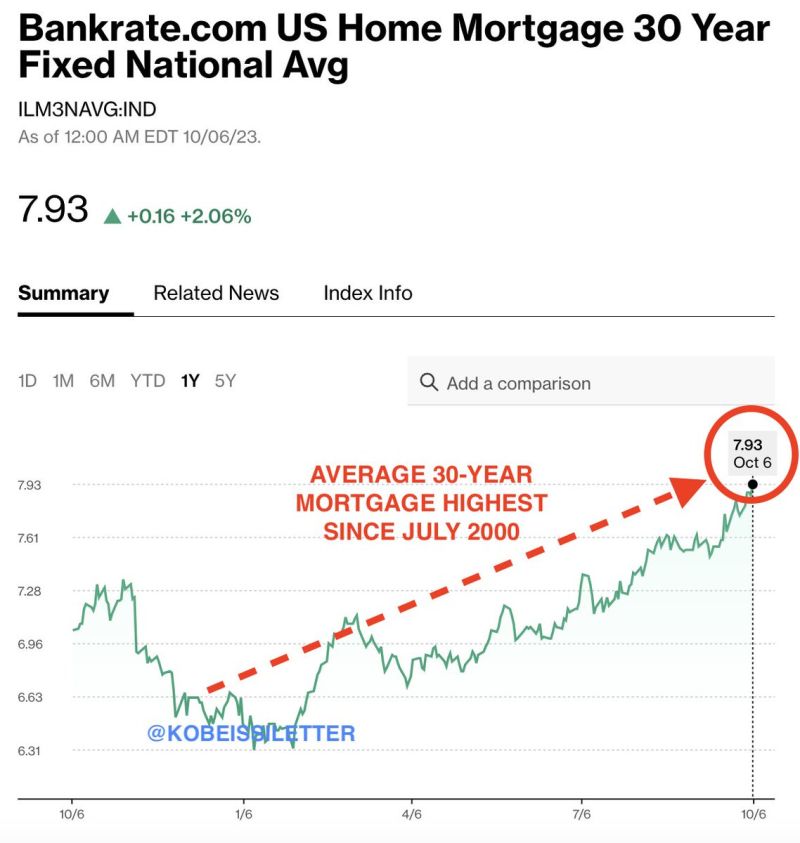

BREAKING: Average interest rate on a 30-year mortgage rises to 7.93%, its highest since July 2000

Since January 2021, less than 3 years ago, interest rates have gone from 2.65% to 7.93%. This means that homebuyers just 3 years ago would see their interest rate TRIPLE if they decided to move. This is exactly why existing home sales are at their lowest since 2010. The average new home is about to cost LESS than the average existing home for the first time since 2005. You know something is wrong when old costs more than new. Why sell if your mortgage rate triples? From The Kobeissi Letter

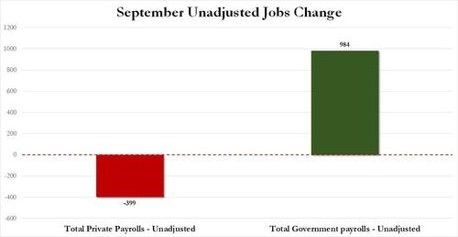

Looking at the September US payroll numbers through another lens

Unadjusted total payrolls rose by 585K and yet private payrolls dropped by 399K. All of the unadjusted jobs in September came from the government, which added a whopping 984K jobs (mostly teachers). What if all the mess in Washington (shutdowns, political gridlock in Congress, etc.) and rising cost of debt put a cap on the fiscal support? Where are the jobs going to come from? Source: www.zerohedge.com, Bloomberg

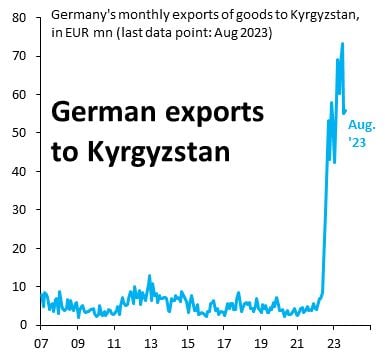

Robin Brooks tweet: "In the first 8 months of 2023, German exports to Kyrgyzstan were up 1400% from the same period in 2019

A lot of these goods - mostly cars and car parts - never ends up in Kyrgyzstan, but go directly or indirectly to Russia"

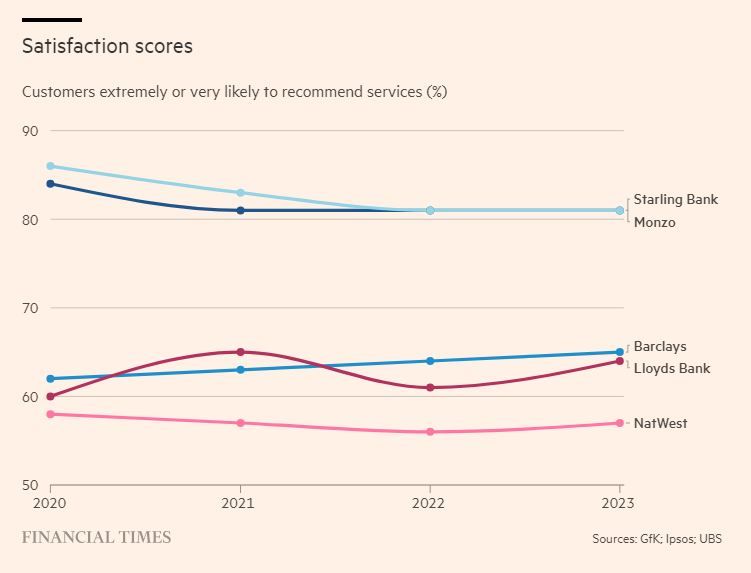

Interesting FT article on UK neobanks: "UK fintech: neobanks may end up blending in"

Low fees mean profits have remained elusive. But higher interest rates are now compensating for that, not least with better returns on client money put out on deposit. Satisfaction scores by customers are also much higher than traditional banks. Some lessons need to be learned. Source: https://lnkd.in/emZyY76d

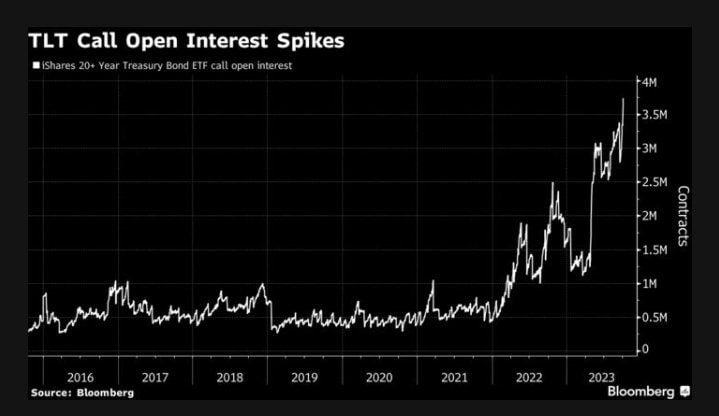

Open interest for bullish call contracts has soared to an all-time high for $TLT

Traders see an end to the market rout that has led to TLT’s longest streak of weekly losses since 2022. Source: Credit From Macro to Micro