An ugly canadian CPI, surging crude oil prices and cautious positioning ahead of tomorrow's FOMC decision have pushed #us treasuries yields to their highest since 2007...

Bonds are now at their cheapest to stocks since Oct 2007... Source: Bloomberg, www.zerohedge.com

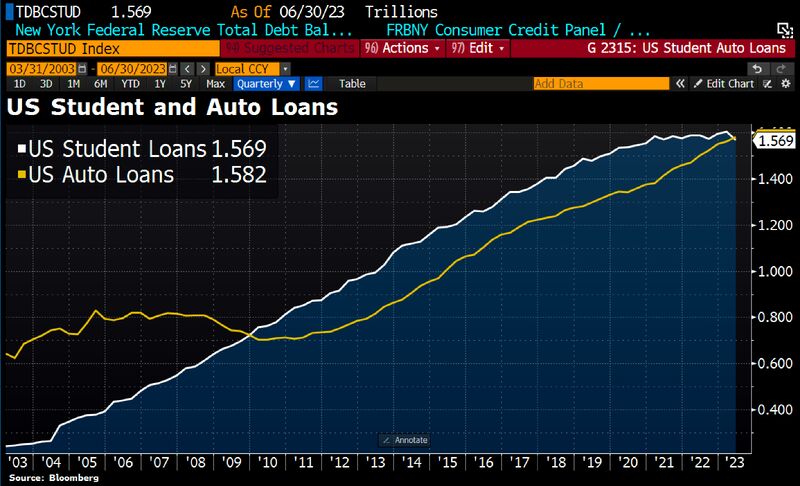

From October onwards, US consumers face a double whammy: student loans + auto loans...

Suspended Student loan payments helped fuel the auto market over the last several years. Auto loans pass Student loans in consumer debt load for the first time in 13yrs, which means consumers face a double-whammy starting in October w/existing auto payments & resumed student loan obligations. Auto loan delinquencies are on the rise and more consumers could fall behind if unemployment increases. Source: Bloomberg, HolgerZ

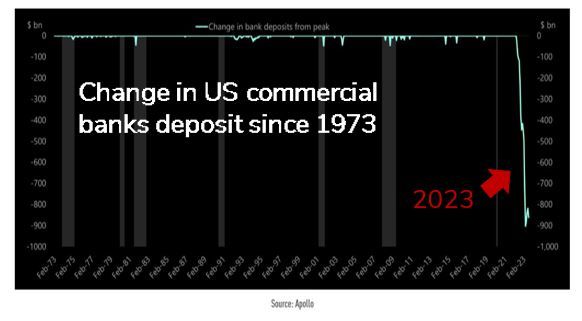

In the US, the slow motion bank run continue...

Interest Rates on Deposits, by Bank: 1. Wells Fargo: 0.15% 2. Citibank: 0.05% 3. Chase: 0.01% 4. Bank of America: 0.01% 5. US Bank: 0.01% Rates on Alternatives to Bank Deposits: 1. CDs: 5.0% 2. Money Market: 4.5% 3. Treasury Bonds: 4.0% Deposits continue to flow out of banks at a historic pace with $1 trillion+ withdrawn over the last year. The era of "free" money for large US banks is coming to an end. They must raise interest paid on deposits or capital will continue to leave. Source: The Kobeissi Letter, Apollo

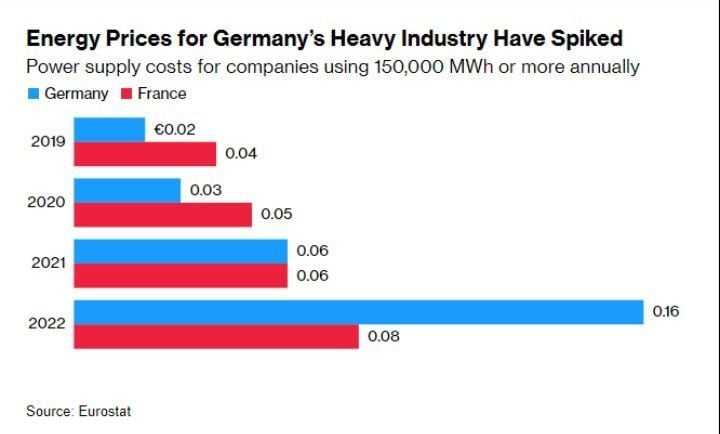

Why German industrial model is at risk in one chart...

Without reliable access to affordable power, Germany fears energy-intensive companies will invest elsewhere, and “we will lose this industrial base,” vice-chancellor Robert Habeck said. Source: Eurostat, Gustavo Philippsen Fuhr

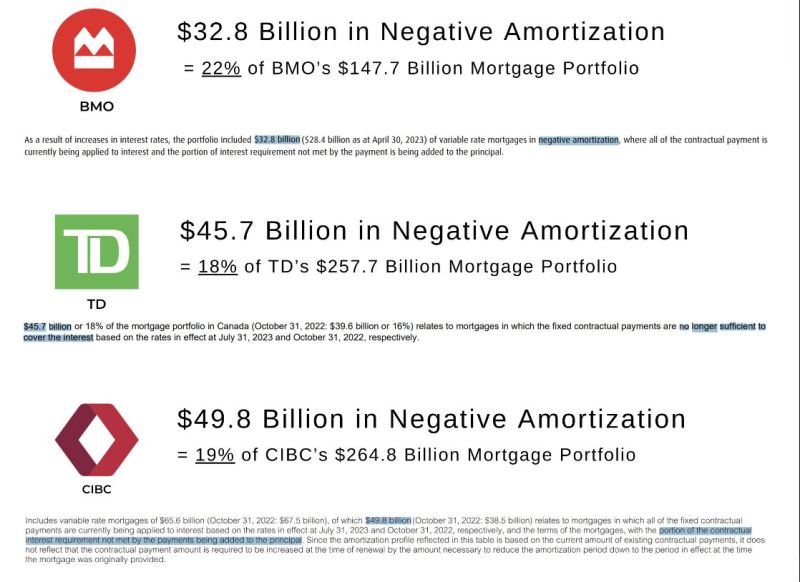

Have you ever heard about mortgages in negative amortization?

As highlighted by The Kobeissi Letter, three of Canada's largest banks are seeing ~20% of their outstanding mortgages in negative amortization. What does this mean? Monthly payments on ~20% of mortgages at BMO, TD, and CIBC are no longer enough to cover interest expense. This means you end up owing more than your original loan amount over time. Typically, variable rate mortgages with fixed payments experience this in a rapidly rising interest rate environment. These homeowners may begin to foreclose over the next few months. This is an important trend worth watching.

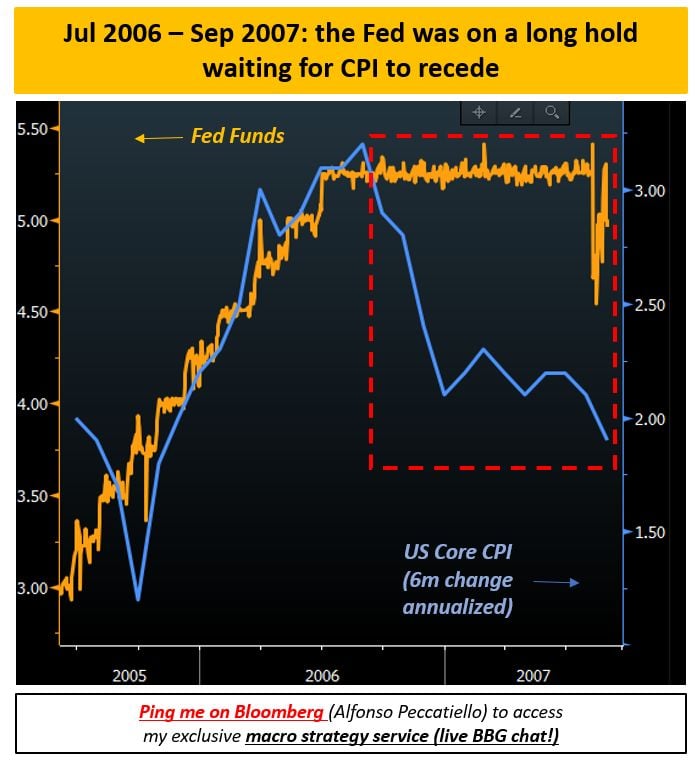

Can be the second half of 2007 be a good parallel for today's market?

As highlighted by MacroAlf, back in 2007, the FED kept rates at 5.25% (orange) despite core inflation was trending around 2% (blue) for quarters already. That ''higher for longer'' stubborness kept policy unnecessarily tight - as we figured out in 2008... Source: Alfonso Peccatiello

It is official? Total US Debt surpasses $33 trillion for the first time. For those keeping tabs, the US added $1 trillion in debt in just 3 months

Cartoon: Gary Varvel

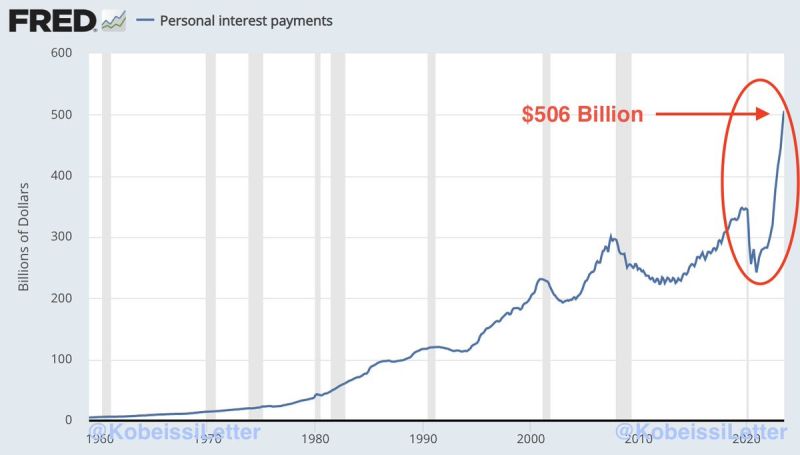

JUST IN: Personal interest payments in the US hit a record $506 BILLION in July

During the first 7 months of 2023, Americans paid a total of $3.3 TRILLION in personal interest. This is up a staggering 80% since 2021 and nearly above the entire 2022 total. The worst part? These numbers do NOT include interest on mortgage payments. Source: The Kobeissi Letter, FRED