German inflation unexpectedly accelerated in July to 2.3% YoY from 2.2% in June as food price inflation keeps rising, core inflation, and services inflation remain sticky at 2.9% and 3.9%.

Source: HolgerZ, Bloomberg

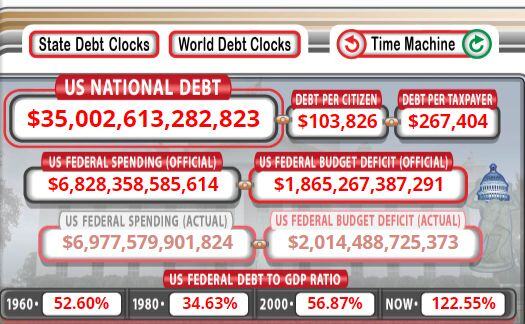

JUST IN: U.S. National Debt surpasses $35 Trillion for the first time in history

Source: Barchart

In the US, if your income and net wealth has not increased by 25% since 2020 you are poorer now than four years ago...

Source: Michel A.Arouet

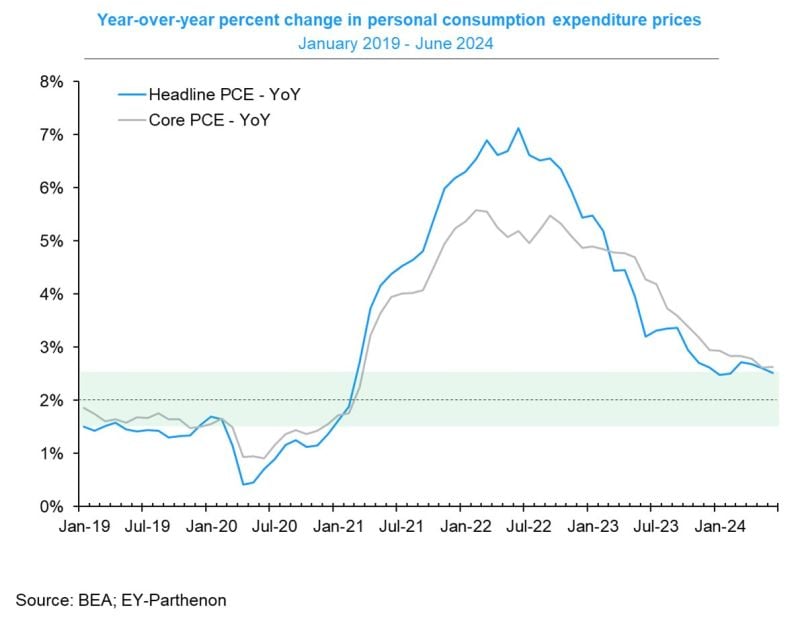

Easing US inflation in June👏

✅Headline PCE prices: 0.1% m/m ✅Core PCE prices: +0.2% m/m 🎯Moving toward Fed's 2% target: ⤵️Headline inflation -0.1pt to 2.5% yoy, IN-LINE with expectations. This is the lowest level since February '21 and down from 7.2% two years ago... ↔️Core inflation is flat at 2.6% yoy, at the lowest level since March '21. This is slightly above expectations (2.5%), which is not such a big surprise as PCE data from yesterday's GDP report revealed a similar picture. Source: Gregory Daco, BEA, EY-Parthenon

JUST IN 🚨: There is now a 100% chance of a 25 bps interest rate cut by September, according to CME FedWatch

Source: Barchart

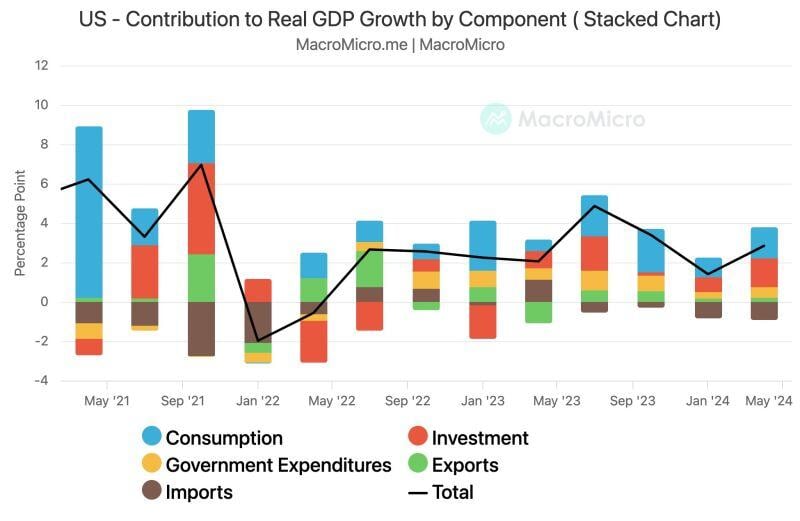

🚨 Breaking! US GDP growth surpasses expectations, hitting 2.8% (est. 2.0%, prev. 1.4%).

GDP Annualized QoQ Contribution: Consumption 1.57 pp (prev. 0.98 pp) Government Spending 0.53 pp (prev. 0.31 pp) Investment 1.46 pp (prev. 0.77 pp) Exports 0.22 pp (prev. 0.17 pp) Imports -0.93 pp (prev. -0.82 pp) Source: MacroMicro

Bulls praying to Lord Powell for a rate cut next week

Source; Barchart

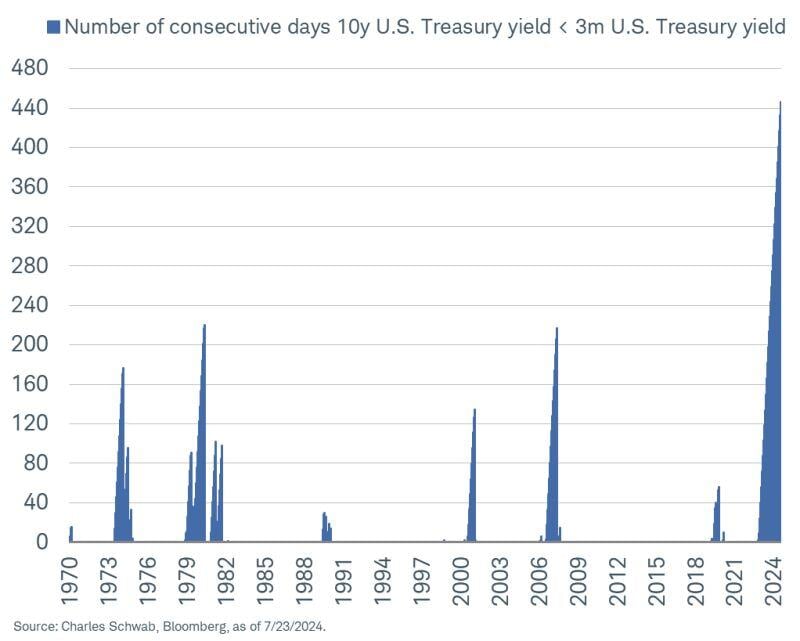

US 10y-3m yield spread has been negative for more than 440 days.

But no recession so far... Source: Kevin Gordon