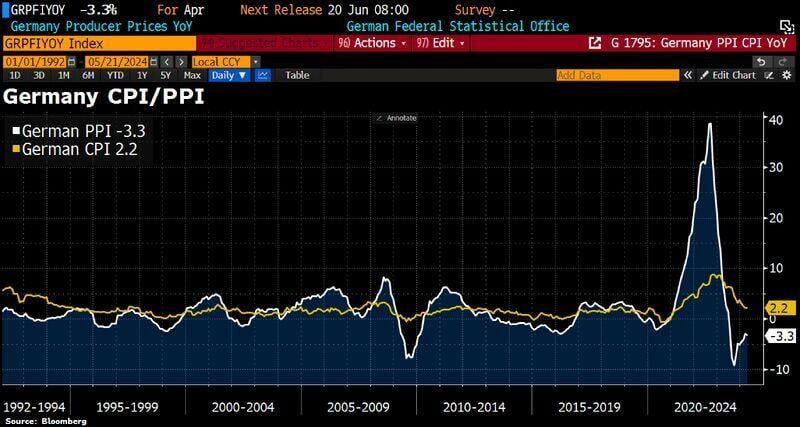

Deflationary forces are intensifying again in germany.

Producer prices fell by 3.3% YoY in April. In March, the decline was 2.9%. PPI is a good leading indicator for CPI. Source: Bloomberg, HolgerZ

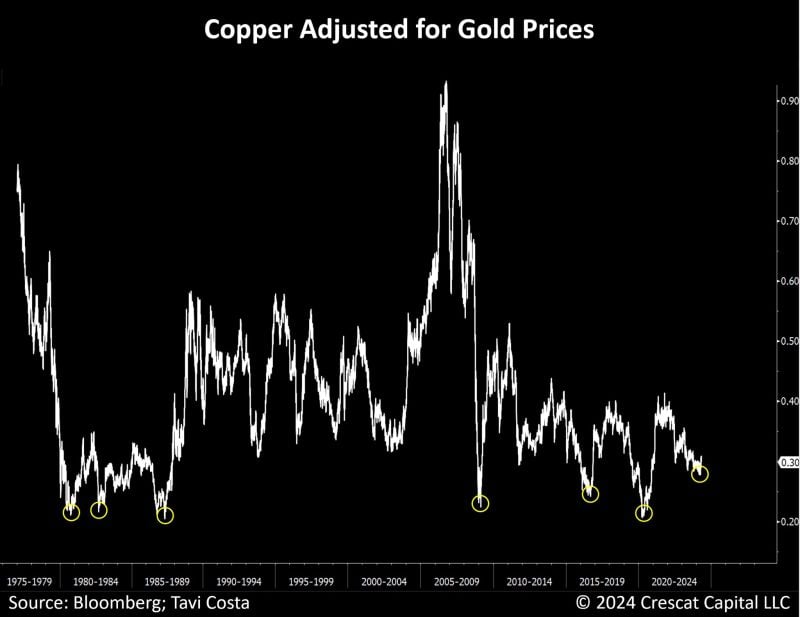

As highlighted by Tavi Costa ->

Despite the recent surge in copper prices, when adjusted for true inflation, the metal is trading at levels we saw in the early 1990s. Will copper prices adjusted for gold still be this low by the end of this decade if we proceed with one of the largest infrastructure developments we've seen in the last 100 years??? Source: Crescat Capital, Bloomberg

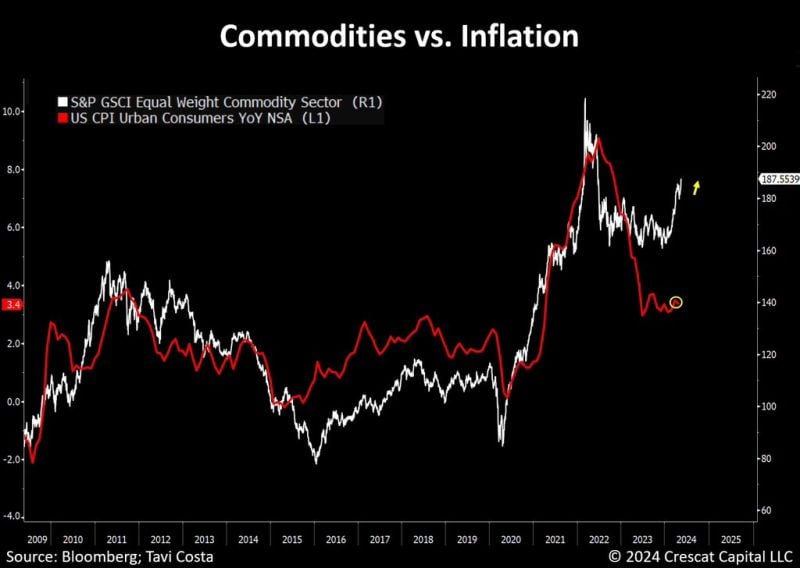

Could headline inflation start following the rebound in commodities prices?

Source: Tavi Costa, Bloomberg

The cost of servicing US government debt is on course to surpass defense spending

Source: Bloomberg, Michael McDonough

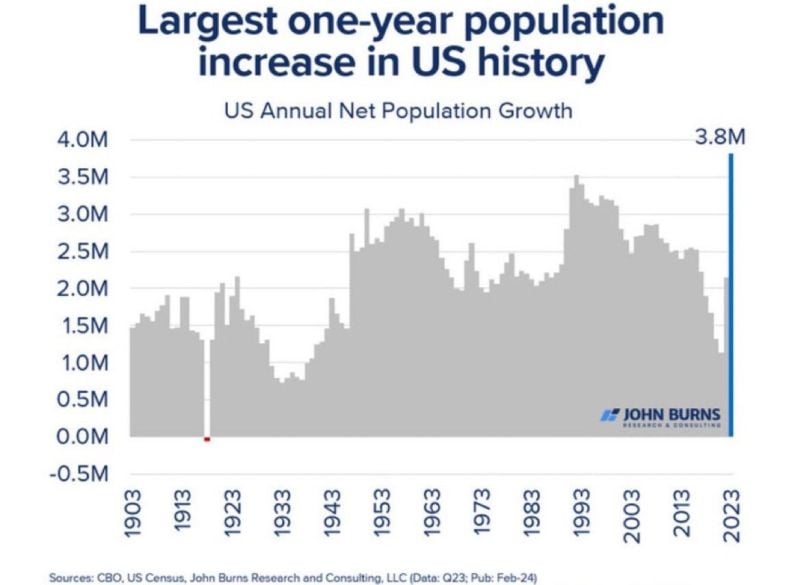

US Demographics

.

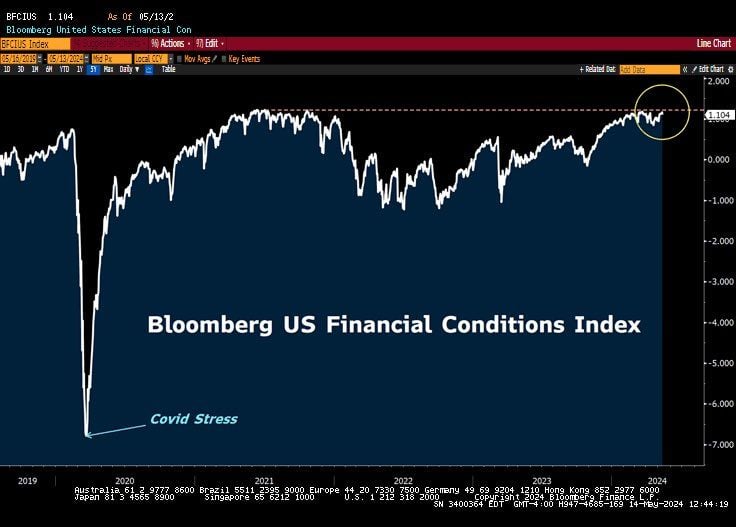

Today’s inflation numbers are seen as a relief by investors… and the FED

Indeed, the just released data shows that US inflation cooled down in April for the first time in 6 months, following several reports of upside surprises. While yoy headline inflation is in-line with expectations (+3.4pct) the positive surprise came from the MoM number (+0.3pct) which is BELOW estimates (+0.4pct). Core inflation number MoM came in as expected (+0.3pct). The core yoy number (+3.6pct as expected) is at the lowest level since April 2021. Bottom-line: this report is bullish equities, bonds, gold and cryptos as it indicated that the disinflation trend might have further to go. Still, we believe that the Fed might wait for some confirmation before turning dovish. We note that the SuperCore (core ex-shelter) rose 0.5pct MoM to 5.05pct YoY. Source: CNBC

“We have to let restrictive policy do its work on inflation.”

Fed Chair Jay Powell Source: Lawrence McDonald, Bloomberg

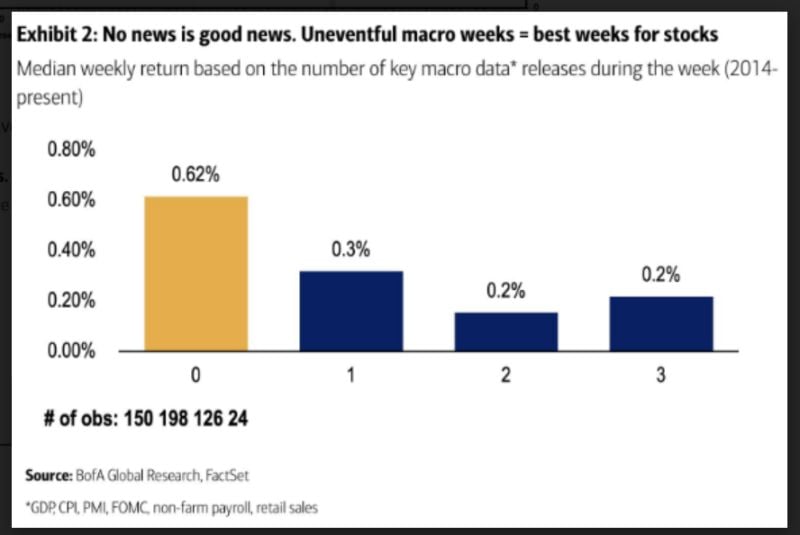

Non major macro weeks have been better...

Source: BofA