The cycle of change

Source: Reads with Ravi on X

The ratings agency kept the U.S. at AA+/A-1+ with a stable outlook.

“The stable outlook indicates our expectation that although fiscal deficit outcomes won’t meaningfully improve, we don’t project a persistent deterioration over the next several years,” S&P said in its statement. The firm pointed to broad economic resilience, policy continuity, and strong revenue streams, including what it described as “robust tariff income” - as offsets to fiscal slippage stemming from legislative changes. While acknowledging concerns that tariffs could dampen business confidence, growth, and hiring while spurring inflation, S&P said revenue gains would help balance the ledger, WSJ reports. The agency’s decision comes against the backdrop of a $5 trillion increase in the debt ceiling and projections that net general government debt will approach 100% of gross domestic product, driven by “structurally rising non-discretionary interest and aging-related expenditure.” S&P cited several strengths underpinning the rating, including the resilience of the U.S. economy, effective monetary policy, and a deficit trajectory that, while elevated, isn’t accelerating. Yet the firm also noted risks... “Bipartisan cooperation to strengthen the U.S. fiscal profile - namely to meaningfully lower deficits and tackle budgetary rigidities - remains elusive,” S&P said. Below is a chart of USA sovereign credit risk Source: zerohedge

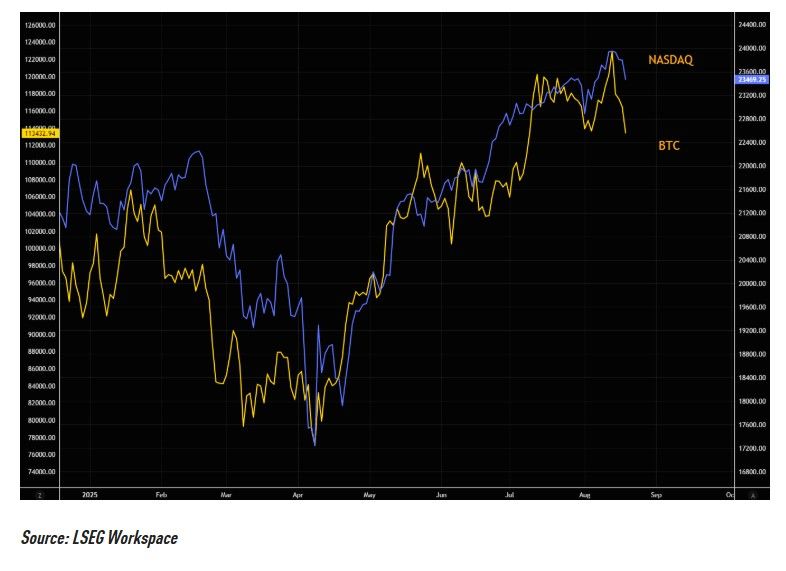

Nasdaq and Bitcoin often trade in the same direction

Source: www.zerohedge.com, LSEG workspace

Stocks and rate-cut expectations have decoupled significantly since the start of the Summer... will they start to move in sync after Jackson Hole ?

Source: zerohedge

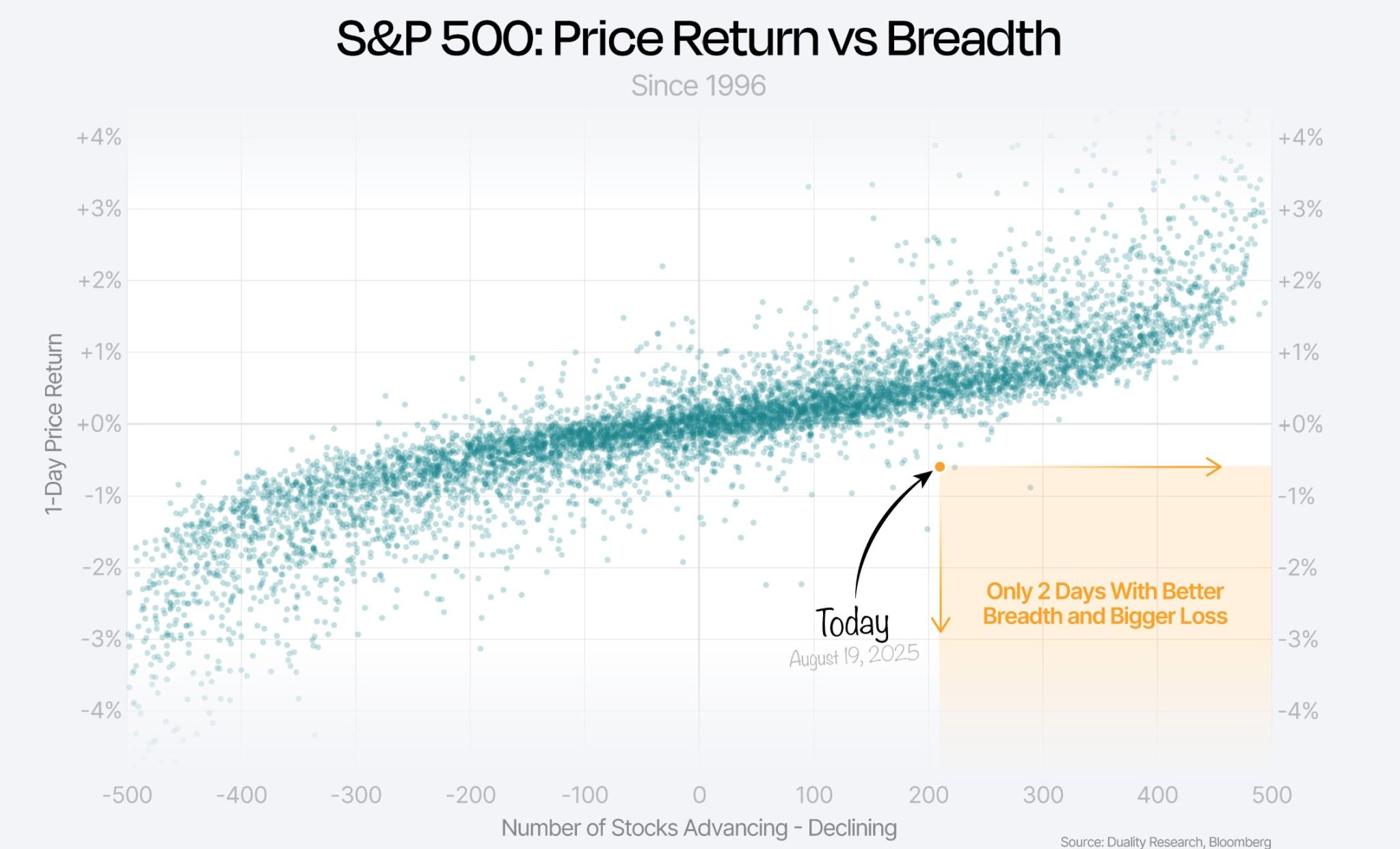

Very interesting session in Wall Street yesterday Since 1996, only two other days have seen stronger S&P 500 breadth paired with a bigger loss.

Source: Duality Researchv@DualityResearch

Let's hope that all that capex pays off

Source: @PeterBerezinBCA

What a chart by Brew Markets...

Source: Bloomberg

If you buy individual stocks, you must know how to identify a moat

Source: Brian Feroldi