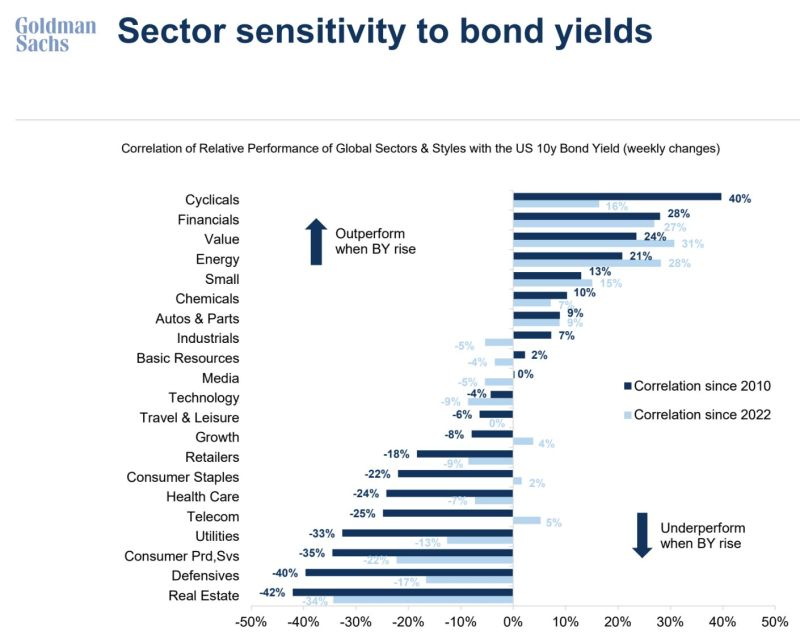

A good chart from GS that shows how sectors & factors may react to change in 10Y bond yields.

Source: Ayesha Tariq, CFA, Goldman Sachs

"....the selloff in US bonds is driving yields higher everywhere, including in economies where the growth outlook hasn’t improved.

Of course, this second point isn't hard to explain. US Treasuries act a generic riskfree asset for the global financial system. When US yields move higher, it creates pressure on bonds everywhere." - TS Lombard, Perkins thru The Market Ear

A turn in the trend? US 10-year Treasury yield has risen ~440 basis points over the last 5 years to 4.76%.

If this trend continues that will materially shift the investing landscape with many investors being caught off guard. Source. Bloomberg, Global Markets Investor

This chart is $IEI iShares 3-7 years Treasury Bond ETF / $HYG iShares iBoxx $ High Yield Corporate Bond ETF

Clearly not indicating any major credit risk! Maybe the market isn’t pricing in a credit crisis because there isn’t one to price in... Source: @cfromhertz on X

The $TLT chart shows a significant 52% decline from its peak, highlighting the harsh effects of increasing rates.

Investing in long-duration US Treasuries is advisable only under specific circumstances: - When a recession is on the horizon. - When inflation is quickly slowing down. Currently, neither of these scenarios is unfolding. Source: Kurt S. Altrichter, CRPS® on X

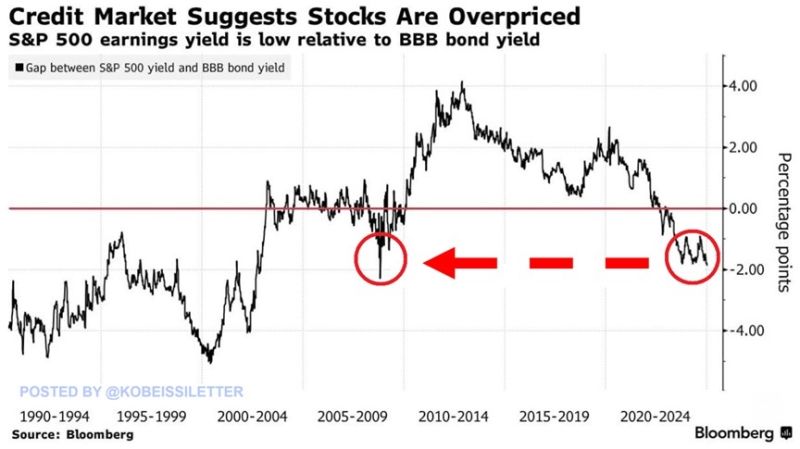

BREAKING: The difference between the S&P 500’s earnings yield and BBB-rated corporate bond yield has dropped to -1.9%, the lowest in 15 years.

Excluding a brief period in 2009, this is the lowest level in 23 years. The gap has fallen by 4 percentage points over the last 5 years as US interest rates have risen sharply. In other words, less risky investment-grade corporate bonds now pay a higher yield than S&P 500 companies' profits relative to their stock prices. This metric suggests the market may be overvalued. Can this gap continue to widen? Source: Bloomberg, The Kobeissi Letter

OUCH! UK 10y yields rose as much as 14bps to 4.82%, highest since Aug. 2008

Source. HolgerZ, Bloomberg

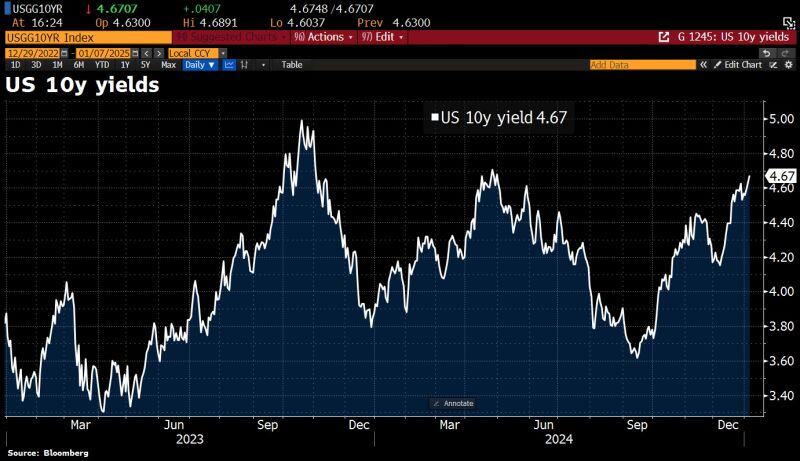

Yields spike after somewhat hot US economic data with US 10y now at 4.67%:

ISM Prices Paid Index came in higher than expected, signaling potential future inflation. At the same time, JOLTS job openings unexpectedly increased, with previous month's data also revised upward. Source: Bloomberg, HolgerZ