Oil Just Did the Unthinkable.

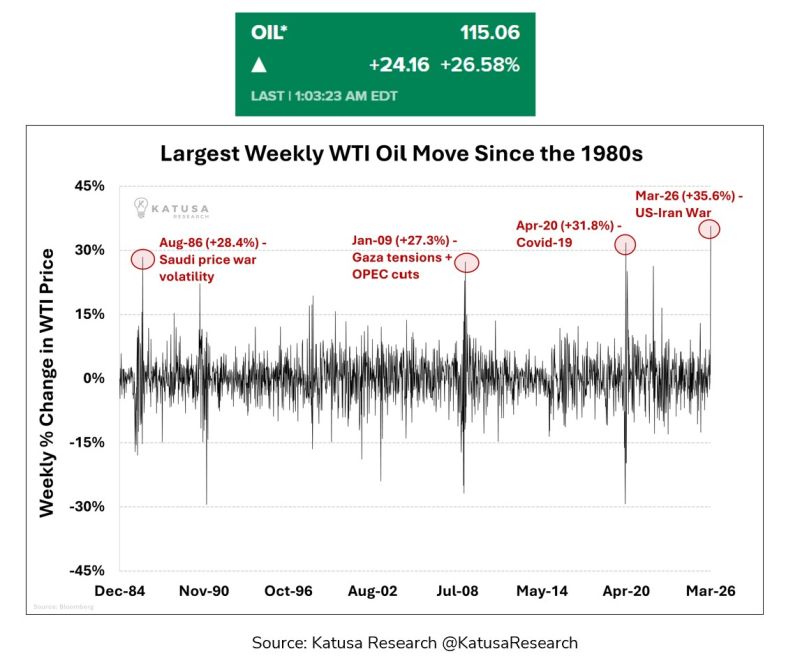

It didn’t just beat a crisis. It beat every crisis. Last week, WTI oil moved more violently than: • The Saudi price war of 1986 • The Gaza crisis of 2009 • Even the Covid demand collapse of 2020 In one week, oil experienced its biggest move in 40 years of recorded history. Source: Katusa Research @KatusaResearch

South Korea and Taiwan imposed fuel price caps to shield their economies from rising oil costs after the Middle East conflict.

South Korean President Lee Jae Myung announced a maximum price system for petroleum, the first in nearly 30 years, and pledged to seek alternative energy sources beyond the Strait of Hormuz. Taiwan set a weekly limit on oil-price increases to stabilize domestic prices, with the government activating its price-stabilization mechanism. Source: Market Watcher

Great chart by Bluekurtic Market Insights Bluekurtic -> Middle East producers have started reducing oil production.

A rise in oil prices to around $108 per barrel could add roughly 0.8 percentage points to U.S. inflation. The impact on Europe and the UK would be far more severe due to their greater dependence on energy imports.

1973-74 oil embargo

Source: QE Infinity @StealthQE4

BREAKING: Oil just slipped back below $100.

It traded as high as $119 this morning...

The G7 may be preparing the largest oil reserve release in history.

G7 finance ministers held an emergency call to discuss a coordinated release of strategic petroleum reserves led by the IEA. The U.S. and two other countries support releasing 300–400 million barrels—25–30% of reserves and more than double the previous record. WTI crude briefly spiked to $120 before dropping to $102.5, while U.S. gasoline rose to $3.45 per gallon. This would be the largest emergency release in history. Source: Global Markets Investor

Germany, where spot gas prices have surged to above €60 per megawatt hour.

That makes natural gas roughly 6 times more expensive here than in the US. Source: Bloomberg, HolgerZ

America ALLOWS Modi Regime purchase oil from Russia temporarily.

American EXPECTS, India will purchase costlier oil from it. Narendra Modi’s regime is a puppet in the hands of America who has TRADED ‘India’ in return for support to Rule over India. Source: Raju Parulekar