WSJ: "Nvidia $NVDA is in talks to provide a roughly $250 billion backstop for OpenAI as part of a massive data-center project

It is one of the most ambitious financial transactions yet in America’s artificial-intelligence boom The guarantees from Nvidia would help the ChatGPT maker lease a 10-gigawatt project that SoftBank’s energy subsidiary is developing in southern Ohio, people familiar with the matter said. In total, the project could cost more than $500 billion, including the chips that would go inside the data centers. It would be the largest data-center project announced to date".

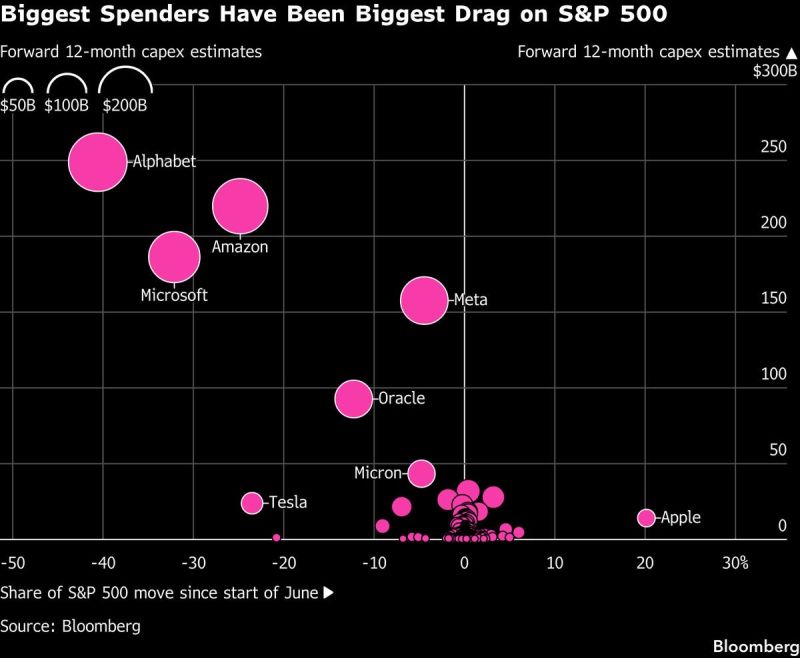

Biggest spenders have been biggest drag on S&P 500 since the start of June.

The chart below shows contribution to SPX declines versus 12 month capex estimates. Apple is the outlier. Tim Apple is leaving the company on a high note. It takes a lot of discipline not to follow the crowd - undoubtedly part of the reason why Buffett loves him. Source: Bloomberg, Negligible Capital

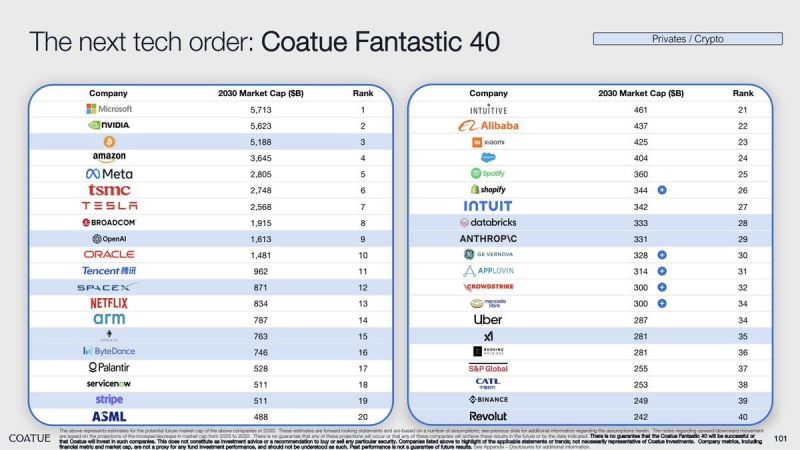

A little over one year ago, Coatue released a 100-page keynote presentation on the evolving technology landscape across public & private companies.

They predicted these 40 companies will be the largest by market cap in 2030. Note the absence of Alphabet $GOOG $GOOGL Source: Koyfin @KoyfinCharts

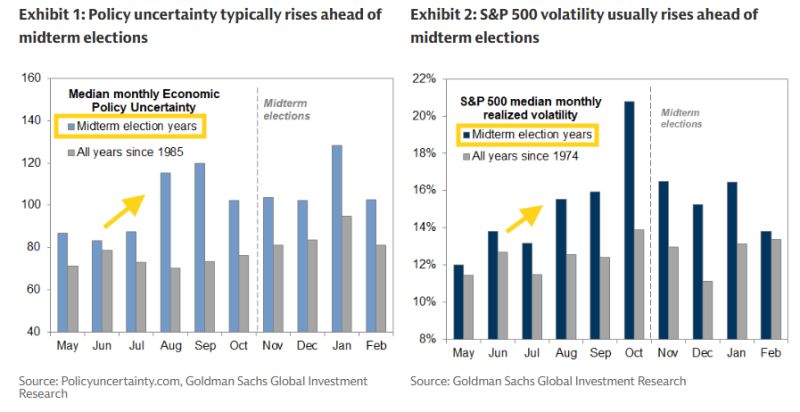

Goldman: With the 2026 midterms three months away, investor focus is likely to turn increasingly to elections in coming weeks. Midterm elections will take place this year on November 3.

During the last few decades, economic policy uncertainty and equity market volatility have typically begun to rise in the late summer ahead of midterm elections. Our economists have found the same pattern after adjusting for the economic cycle as measured by the unemployment rate. Source: Goldman Sachs, Neil Sethi on X

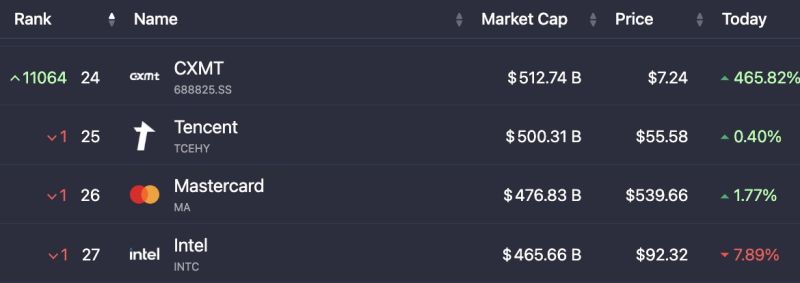

CXMT is the largest Chinese maker of memory chips. Its shares surged +472% in its trading debut.

CXMT opened at ¥49.50 vs its IPO price of ¥8.66. The company raised ¥57.92 billion ($8.6B) in Asia's largest IPO of 2026. CXMT's market value surged to about ¥3.3 trillion ($487B), up from $85.5 billion at its IPO valuation. CXMT is now larger than Intel $INTC and is reportedly now the largest Chinese public company, overtaking ICBC. Based on sales figures for the fourth quarter of 2025, CXMT held a 7.67% share of the global DRAM market in 2025, according to its IPO prospectus. DRAM chips are used in electronic devices ranging from smartphones to servers. The global DRAM market is dominated by Samsung Electronics, SK Hynix, and Micron Technology. The listing comes at a time when CXMT has seen increased attention, following reports earlier this month that Apple has begun testing the Chinese chipmaker’s DRAM for devices sold in China. CXMT swung to an operating profit of 35.43 billion yuan in the first quarter from a loss of 2.83 billion yuan a year earlier, as it saw continued growth in global computing power demand and capacity allocation by major manufacturers. Morningstar said in a note Friday that as AI is increasingly becoming an issue of national security for China, CXMT will likely be a key beneficiary. The research firm added that while CXMT’s technology still lags global memory leaders, domestic internet giants spearheading AI development will likely drive robust adoption of its chips as Beijing pushes for semiconductor self-sufficiency. CXMT, founded in 2016 by Chairman Zhu Yiming, plans to boost its technological capabilities and core competitiveness, primarily memory wafer mass production and R&D projects, by employing the IPO proceeds, according to a Google translation of the information in the prospectus. Source: Bull Theory, Evan on X, CNBC

Yesterday was a terrible day for Mag7 stocks, down almost 5% on the back of GOOGL's plunge (the Mag7 stocks lost almost $800 Billion in market cap on a single day).

This was the worst day for Mag7 since April '25 (Liberation Day) and the basket index broke below all its major moving averages. What's remarkable is that despite that decline, the semis (SOXX) are basically unchanged. Source: zerohedge, Finviz

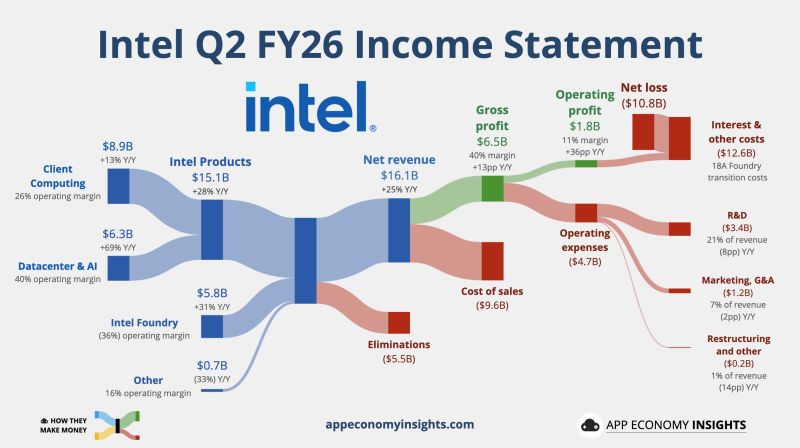

Intel reported better-than-expected second-quarter results on Thursday

Notching its fastest revenue growth rate for any quarter since 2011 and issuing guidance that topped expectations. The stock rose about 4% in extended trading. Intel shares are up over 170% so far in 2026 as of Thursday’s close after soaring 84% last year, when the U.S. government took a 10% stake in the company as part of an effort to support U.S. chip manufacturing. However, the stock has been in a slump more recently, dropping 28% in July. $INTC Intel Q2 FY26: • Revenue +25% Y/Y to $16.1B ($1.7B beat). • Non-GAAP EPS $0.42 ($0.20 beat). Q3 FY26 Guidance: • Revenue ~$15.8-16.8B ($1.2B beat). • Non-GAAP EPS $0.38 ($0.10 beat). Source: App Economy Insights, CNBC

The narrative of 'punish the spenders

(the hyperscalers - in red below) and celebrate the receivers' (the semiconductors - in green below) is still ongoing. Source: zerohedge