2 Dec 2025

Gold is on pace for its best year since 1979, up over 60% in 2025.

Source: Charlie Bilello

1 Dec 2025

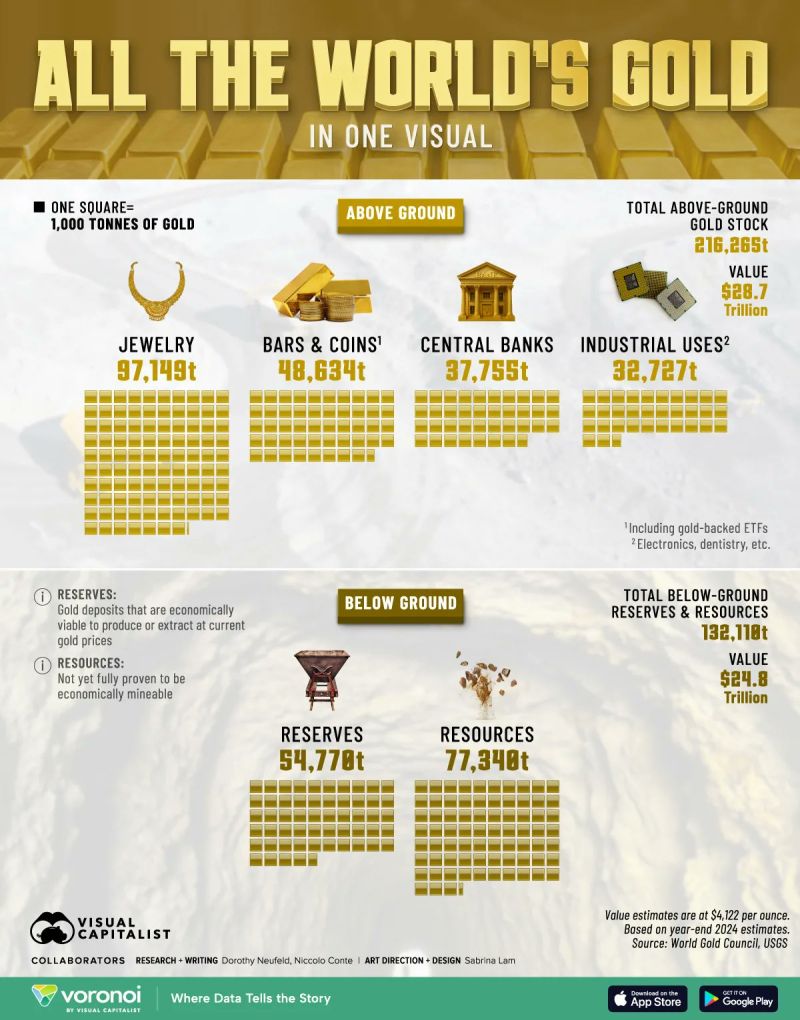

All the world's gold, in one visual

There are 216,265 tonnes of gold above ground… and another 132,118 tonnes still waiting below Where is it all? Jewelry: 97,149t Central Banks: 37,755t Industry & Tech: 32,727t Bars & Coins: 48,634t Source: ⚡️AIGOLD⚡️ @AIGOLDOfficial

28 Nov 2025

Breakout Alert 🚨: Gold

Source: Barchart

28 Nov 2025

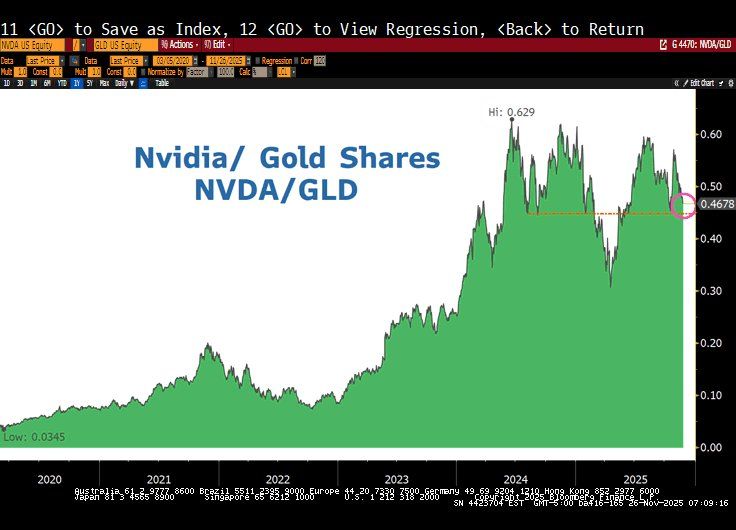

Got Hard Assets?

Gold > Nvidia since Q1 2024 *Bloomberg terminal data. Lawrence McDonald @Convertbond

27 Nov 2025

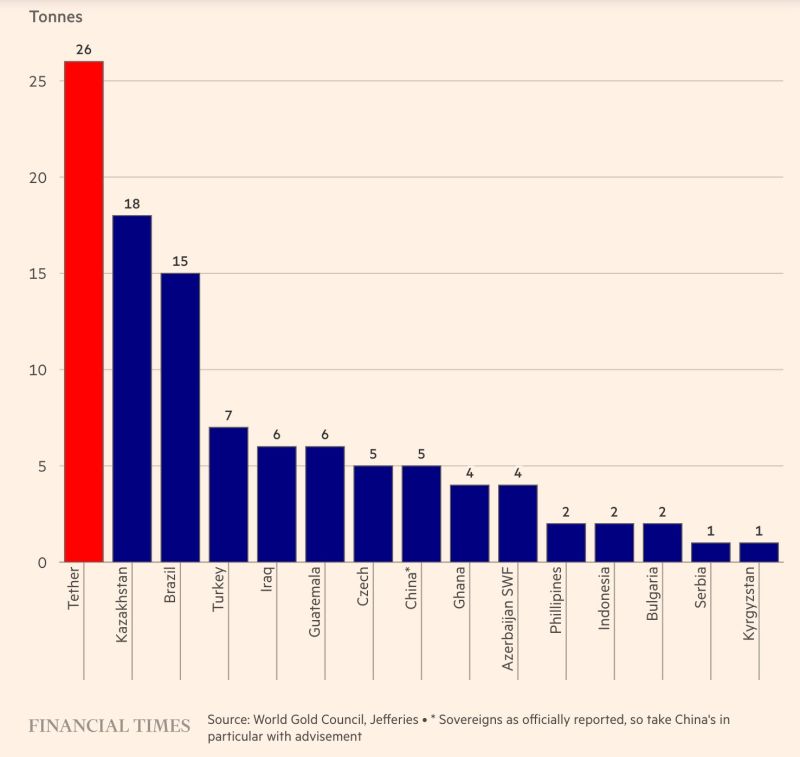

Stablecoin Tether bought more gold last quarter than every Central Bank.

Source: Sam Callahan @samcallah FT

26 Nov 2025

Gold loves rising Japanese rates.

This remains a massive driver of the shiny metal, despite few talking about it on a daily basis. Source: The Market Ear

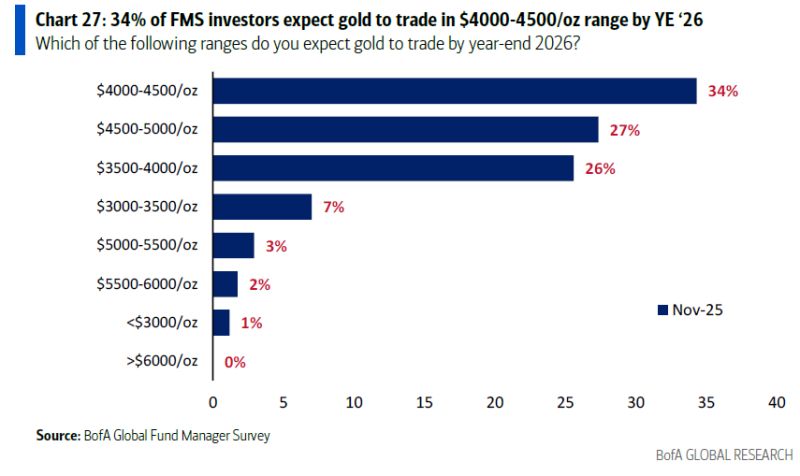

19 Nov 2025

Only 5% of Fund Managers expect gold to trade above $5,000 by the end of 2026, none over $6,000

Source: BofA

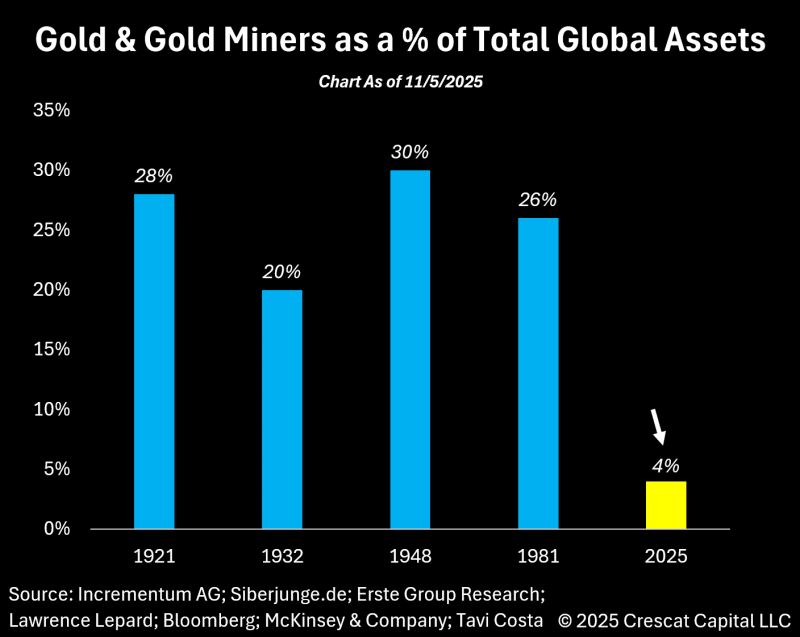

7 Nov 2025

Gold and gold miners together represent about 5% of total global assets.

That is approximately 7–5 times below the highs reached in prior cycles. Source: Tavi Costa, Bloomberg