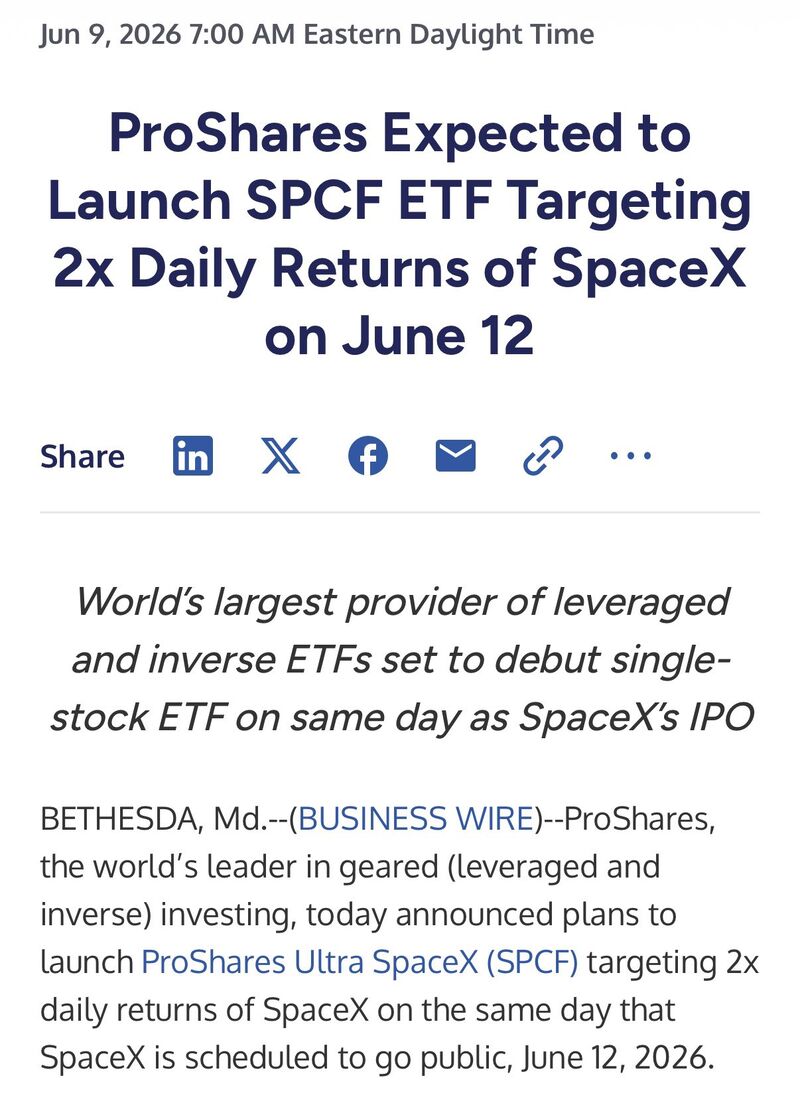

ProShares issued press release indicating it plans to launch 2x leveraged SpaceX ETF on *same day* as IPO.

Source: Nate Geraci

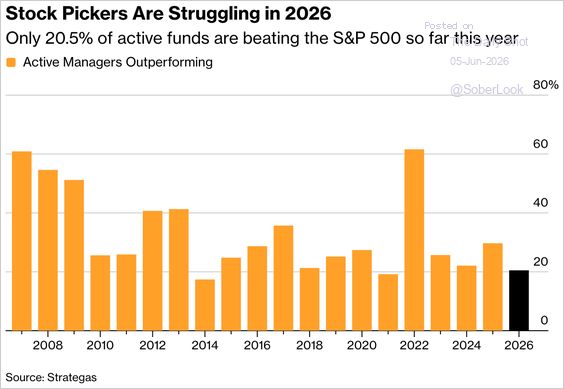

Active large-cap equity managers are struggling to keep pace with a technology-led market rally, with only 20.5% outperforming the S&P 500 this year.

Source: Bloomberg, The Daily Shot

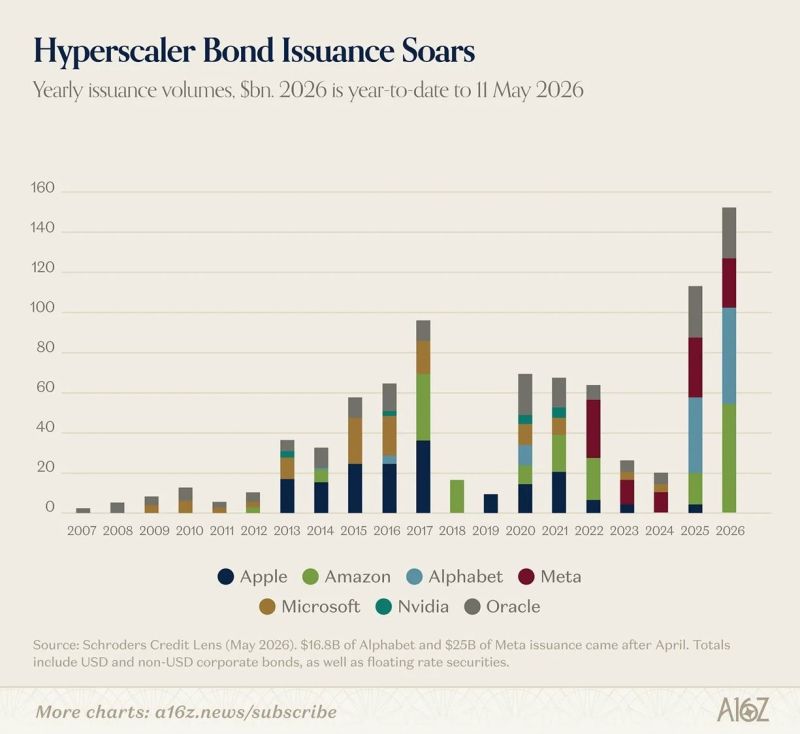

Breaking: Hyperscaler Bond Issuance Soars

In 4+ months in 2026 it is already more than in 2025, and several times more than the average of previous years. Their Free Cash Flow is dropping to 0. -> They must sell stocks, or slow down AI CAPEX. Source: BraVoCycles Newsletter

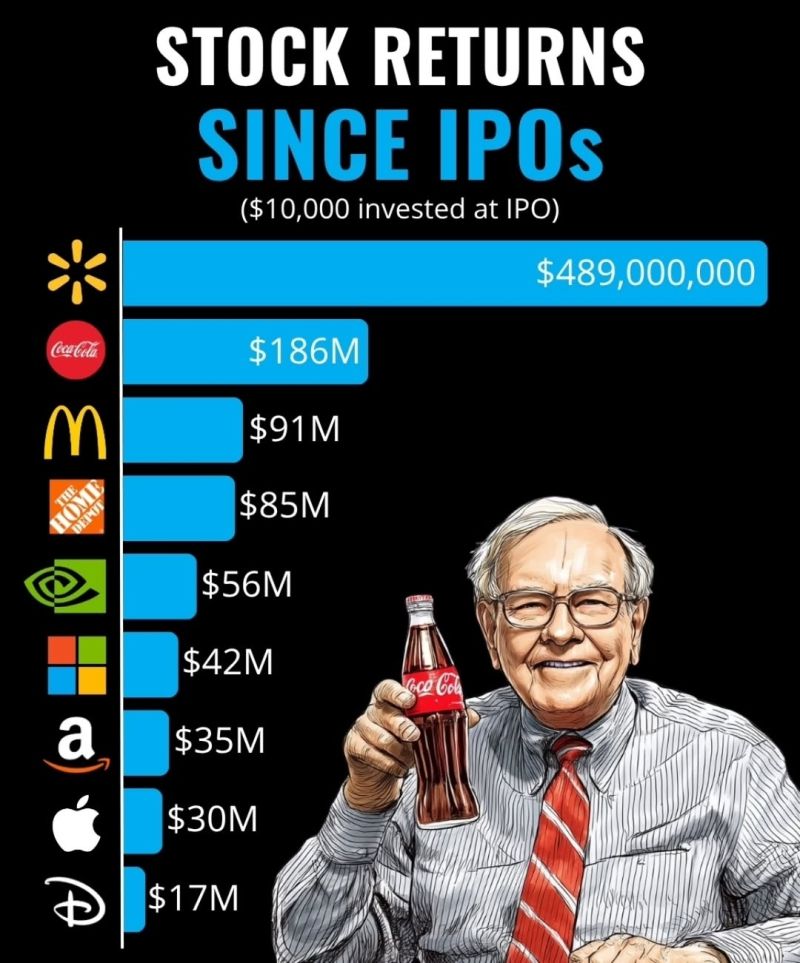

Any retail investor who bought Cerebras after the IPO got decimated.

What about SpaceX?

Stock returns since IPO

Source: Stocks World

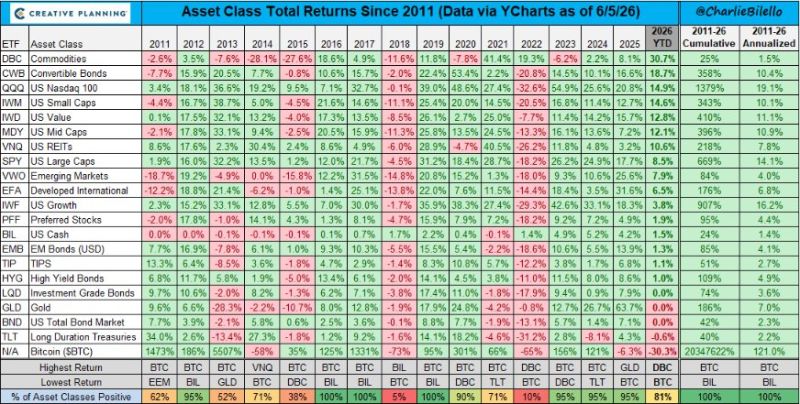

Asset class total returns since 2011

Winners: Commodities +30.7%; Convertibles +18.7%; Nasdaq 100 +14.9%; US Small Caps +12.8% Losers: IG bonds 0%; Gold 0%; US Total bonds markets 0%; Long duration Treasuries -0.6%; Bitcoin -30.3% Source: Charlie Bilello

Just for reference the market cap of the entire stock markets

• UK: ~$3.94 trillion • France: ~$3.45 trillion • Germany: ~$3.04 trillion Europe is becoming really poor. Source: Michel A.Arouet

Trafigura just made $4.1 billion in 6 months.

That's more than its entire 2025 full year. October-December 2025 was the 2nd-best quarter in company history and the war hadn't even fully started yet. For context: → Trafigura full-year 2025 profit: $2.7 billion → Trafigura H1 2026 profit: $4.1 billion → Time elapsed: 6 months Source: Jack Prandelli on X