US debt balance credit cards

Source: TradingView

Images to remember when you are studying big losses at companies pitching AI tools:

Source: Brian Sozzi

In case you missed it... Iran will demand that shipping companies pay tolls in cryptocurrency for oil tankers passing through the Strait of Hormuz

as it seeks to retain control over passage through the key waterway during the two-week ceasefire. Hamid Hosseini, a spokesperson for Iran’s Oil, Gas and Petrochemical Products Exporters’ Union, told the FT on Wednesday that Iran wanted to collect tolling fees from any tanker passing and to assess each ship. He said that the tariff is $1 per barrel of hashtag#oil, adding that empty tankers can pass freely. “Once the email arrives and Iran completes its assessment, vessels are given a few seconds to pay in hashtag#bitcoin, ensuring they can’t be traced or confiscated due to sanctions,” Hosseini added. So why does Iran want to be paid in hashtag#bitcoin? Bacause: - It is portable - It is divisible - It can be trusted - It is economically & politically neutral - It has immutable monetary policy - It has perfect property rights But also because it preserves long-term purchasing power from finite energy exports. Indeed, storing oil revenues in traditional assets like US Treasury bonds can erode value over time, especially as energy prices rise faster than returns. Historical examples suggest Iran would struggle to repurchase the same oil it once sold. In contrast, assets like gold—and more recently Bitcoin—have better preserved or increased purchasing power relative to energy. Bitcoin, in particular, has dramatically outperformed oil prices since 2013. The conclusion is that commodity exporters may increasingly shift reserves into assets like gold and crypto to avoid losing value.

GDP per capita South Korea vs North Korea

Source: Jacob King

$SPX sp500 is back inside the range, trading roughly in the middle. Note the 200 day MA is right here.

Source: TME

Something weird took place the last week of March.

"Our retail cash platform finished last week net selling, the first such week since November 2025 ... retail has moved away from one-way buying behavior." (Citadel)

This is what really matters for markets.

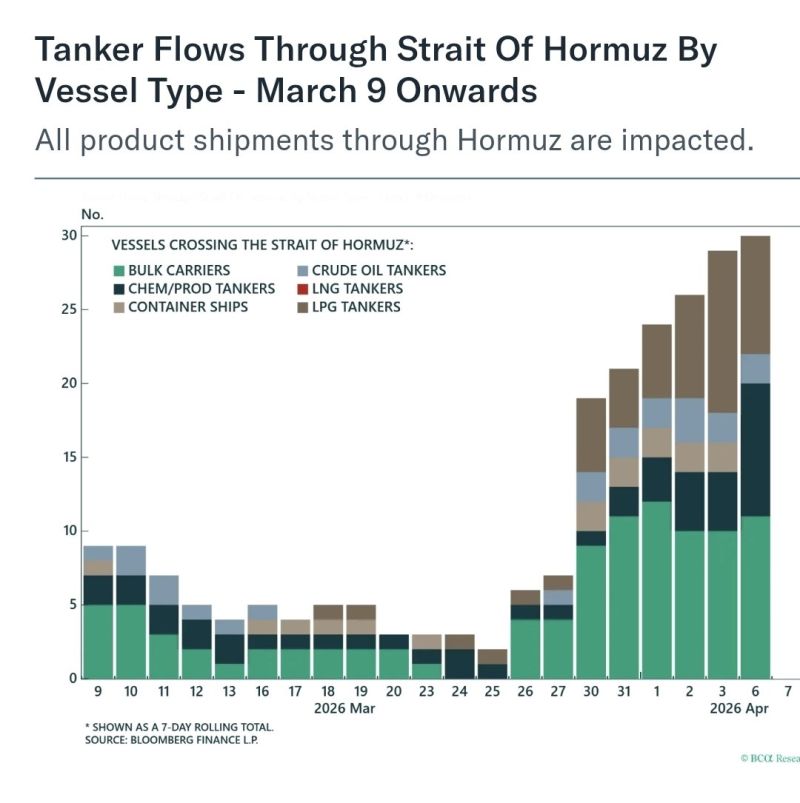

Source: BCA

Goldman Sachs: "We have seen one of the weakest periods of relative returns for technology over the past 50 years."

Source: Brian Sozzi @BrianSozzi, Goldman Sachs