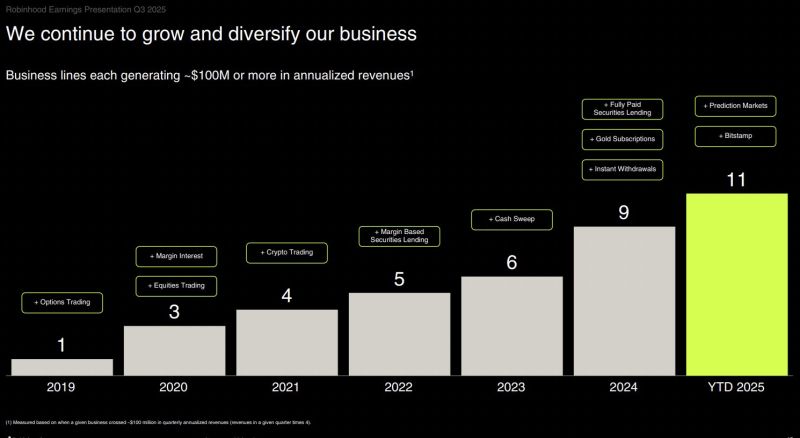

Robinhood $HOOD now has 11 separate business segments generating more than $100 Million of revenue on an annualized basis.

Source: Source: Evan @StockMKTNewz

$SPY S&P 500 is back at multi-month channel support.

Can the bulls pull off another stick save? Source: TrendSpider LLC

The US has added copper, silver, and uranium to its official list of critical minerals

This expanded the Trump administration’s definition of resources considered essential to the nation’s economy and security According to a Bloomberg report, citing a US government website, the revised US Geological Survey list now includes 60 minerals in total — 10 more than before — with new additions such as metallurgical coal, potash, rhenium, silicon, and lead. The list also encompasses 15 rare earth elements and replaces the previous version published in 2022. https://lnkd.in/eFTMDJ29 Source: Firstpost

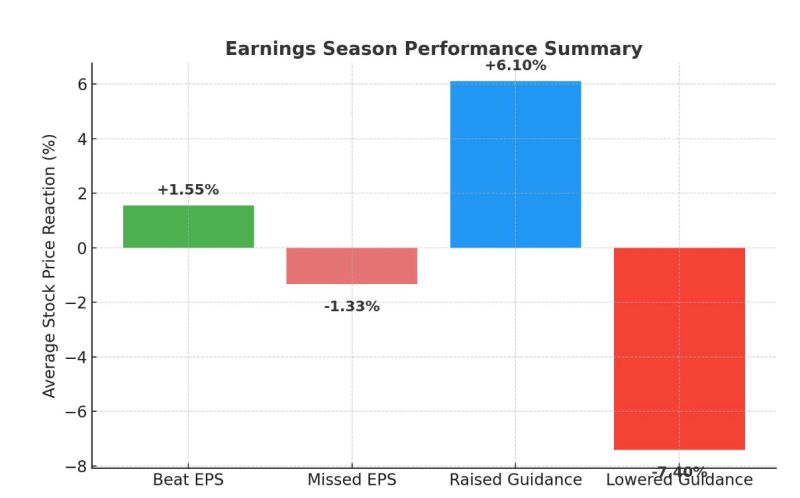

Bespoke on US earnings season thus far:

--Stocks that beat EPS estimates have risen 1.55% while stocks that have missed EPS have fallen 1.33%. --Stocks that have raised guidance (62) have risen 6.1%, while stocks that have lowered (29) have fallen 7.4%. Source: Bespoke

All you need to build a million dollar company?

Source: Omkar @psomkar1

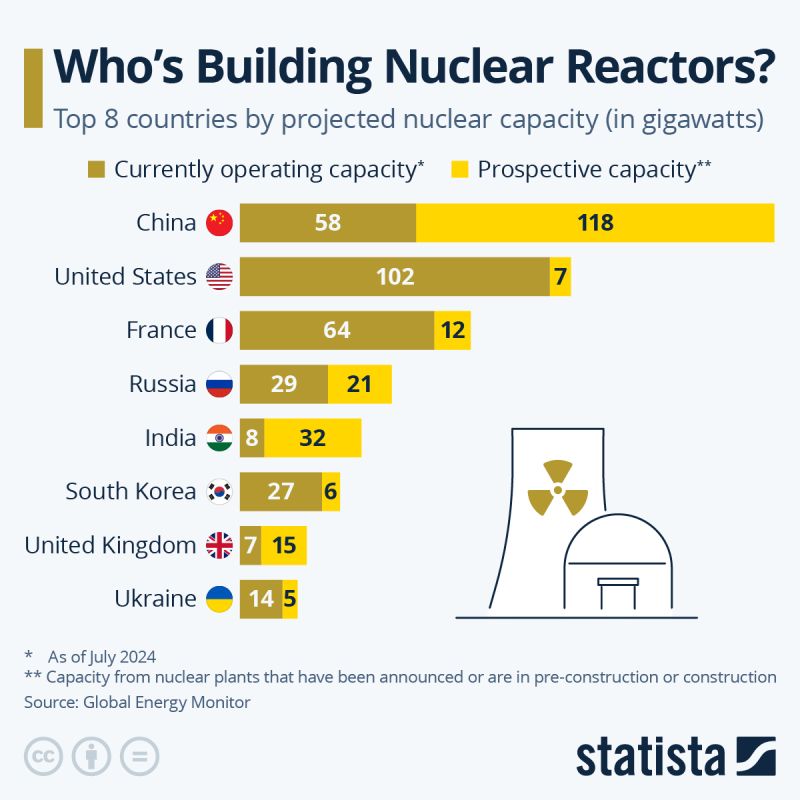

The Nuclear Power Shift Has Begun Right now, the world’s total nuclear power capacity stands at 396 GW.

Another 299 GW is already in the pipeline — announced, pre-construction, or under active build. For decades, the U.S. has been the nuclear superpower, leading with 102 GW of capacity (as of July 2024). It’s followed by: 🇫🇷 France — 64 GW 🇨🇳 China — 58 GW 🇷🇺 Russia — 29 GW 🇰🇷 South Korea — 27 GW 🇨🇦 Canada — 15 GW But the status quo is about to flip — and flip hard. 🚀 China’s Nuclear Acceleration China is building at industrial speed. A total of 104 new reactors are in development across 22 power plants — adding 118 GW of future capacity. If completed (and current reactors stay online), China’s total capacity will soar to 176 GW, surpassing the U.S. for the first time in history. 🇺🇸 The U.S. Response The U.S. plans to add just 7 GW, spread across 30 prospective reactors at 8 power plants — bringing its potential total to 109 GW. However, four major reactors are scheduled to retire soon: Diablo Canyon (2 reactors) by 2030 Salem (2 reactors) by 2036 & 2040 ➡️ Together, that’s a 5 GW reduction. Russia (-4 GW) and Ukraine (-1 GW) also have planned retirements. 🌍 The New Global Order (If All Goes to Plan) 🇨🇳 China – 176 GW 🇺🇸 United States – 109 GW 🇫🇷 France – 76 GW 🇷🇺 Russia – 46 GW 🇮🇳 India – 41 GW 🌱 The Next Wave Beyond China, India is the next big mover — with 31 new reactors across 9 plants adding 32 GW. Other countries ramping up: 🇷🇺 Russia – 21 GW 🇬🇧 U.K. – 15 GW 🇷🇴 Romania – 15 GW 🇹🇷 Turkey – 15 GW 🇵🇱 Poland – 14 GW (starting from zero nuclear capacity) 🇫🇷 France – +12 GW 🇺🇸 U.S. & 🇮🇷 Iran – +7 GW each 🔋 The Takeaway Global nuclear power is not fading — it’s accelerating. We’re entering a new era where energy independence, decarbonization, and geopolitics collide. The next energy superpower won’t just be the one with oil or gas. It will be the one with reactors online and uranium secured. Source: Statista

The government shutdown is officially the longest one ever...

Source: zerohedge

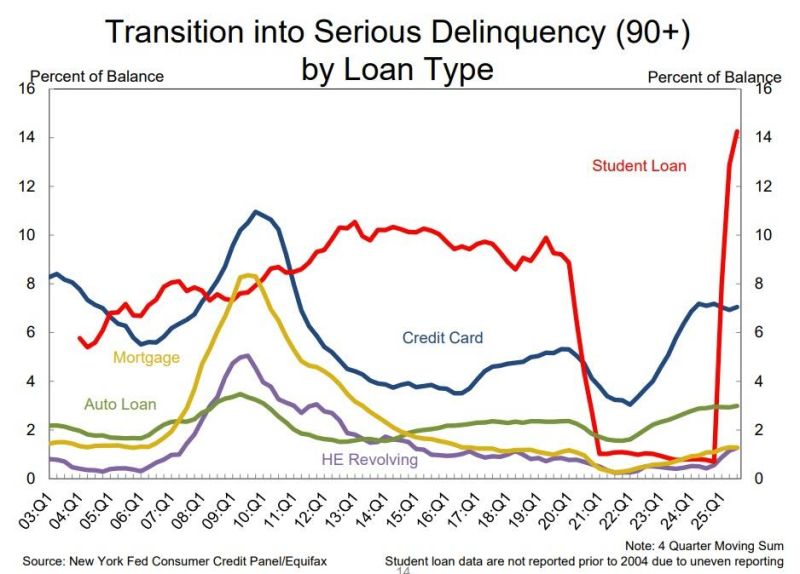

💥 U.S. household debt just hit another record.

The New York Fed’s Q3 2025 report shows total household debt rising $197 billion (+1%) to a new all-time high of $18.59 trillion. Here’s the breakdown 👇 🏠 Housing debt: $13.5T 💳 Non-housing debt: $5.1T Key highlights: 🏡 Mortgage balances up $137B → now $13.07T Delinquency: 0.83% (barely up from 0.82%) 💳 Credit card balances up $24B → now $1.23T Delinquency: 12.41%, highest since 2011 🚨 🚗 Auto loans steady at $1.66T 🎓 Student loans up $15B → $1.65T 90+ day delinquencies at 9.4% — surging after repayment resumed 🏡 HELOCs up $11B → $422B 🧾 In total: Non-housing balances rose 1% from last quarter. 📉 Consumer bankruptcies: 141,600 — the most since 2020. 🔍 What’s happening: “Household debt balances are growing at a moderate pace, with delinquency rates stabilizing,” said the NY Fed’s Donghoon Lee. True — but under the surface, cracks are widening. Credit card delinquencies are the highest in 14 years. Student loan defaults are accelerating — especially among borrowers 50+, where 1 in 5 loans is now delinquent. Mortgage resilience is holding — for now — but that may change if housing prices slip and credit tightens. 🧠 Big picture: Consumers are tapped out. The pandemic-era cushion is gone. Credit limits are rising, but so are missed payments.