Here's a great post on Situation Awareness Hedgefund by CoinPost Inc.

Leopold Aschenbrenner's $20B Situational Awareness fund was up +439% through June... then July erased a huge chunk of those gains as leveraged AI bets unraveled. Instead of de-risking, he's raising fresh capital and calling this "the best buying opportunity since early 2025." His main recovery catalyst? A potential Anthropic IPO. Sometimes the biggest conviction trades look the worst right before they recover. $TE -60.76% $SNDK -55.32% $SHAZ -52.65% $NBIS -46.33% $SEI -46.04% $BE -45.90% $CRWV -38.90% $IREN -35.90% $RIOT -33.38% $HIVE -30.36% $CORZ -29.19% $AMD -26.05% $CLSK -17.46% In a letter to LPs he called the pullback one of the best buying opportunities since early 2025 and opened a new funding window for Aug 1. Anthropic IPO cited as a possible H2 catalyst. Even the biggest AI bulls aren’t immune... Source: Coinpost

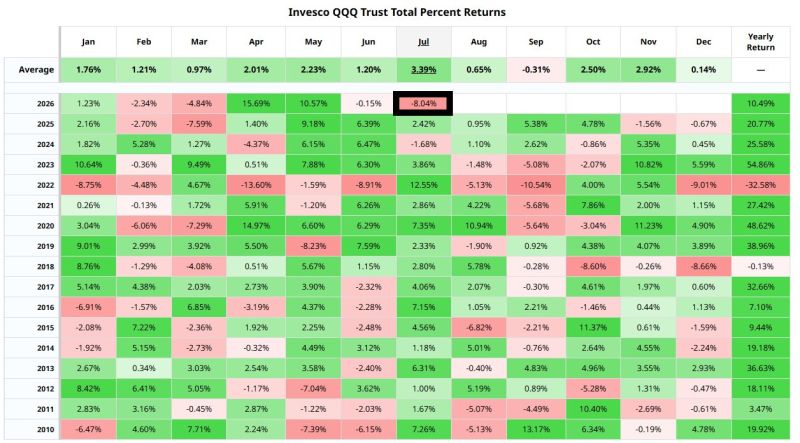

Nasdaq 100 $QQQ is now on track for its worst July in 24 years

Source: Barchart

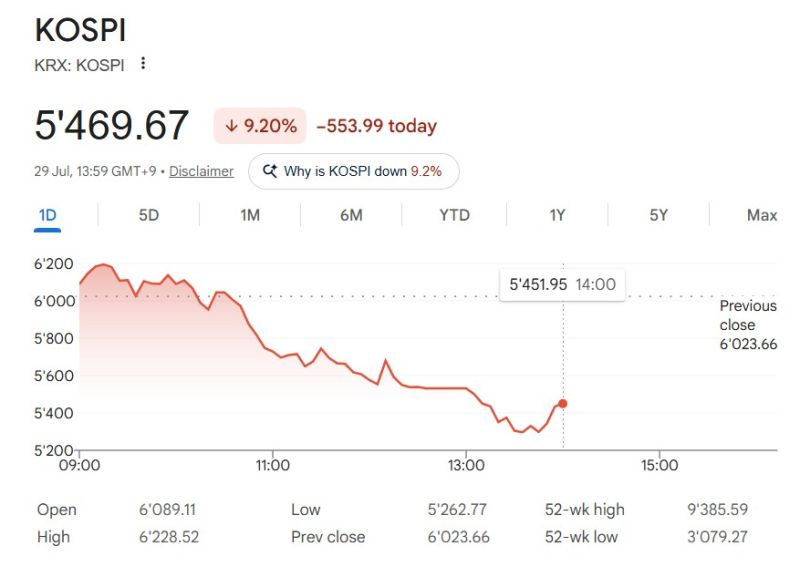

South Korea's stock market is in free fall.

Korea Exchange halted all stock and program trading for the second consecutive day after the KOSPI crashed -8%. KOSPI triggered its ninth circuit breaker of the year and is down -18% in just two days. South Korea has fallen from the world's 6th-largest stock market to 11th after the crash. Source: Bull Theory

This is what a rotational market looks like

S&P 500 Equal weight (white bars) juste made a new all-time high Nasdaq (in green) is getting hammered Source: Bloomberg, RBC

Semiconductor Stocks Head & Shoulders Pattern almost completely formed now It's sitting right on the neckline, if it breaks 528, look out

Source: Barchart

SK Hynix posted record Q2 earnings but still missed expectations.

- Revenue: ₩79.3T vs ₩80.9T (+257% YoY) - Operating profit: ₩60.5T vs ₩64.0T (+557% YoY) - Net profit: ₩93.9T (+1,242% YoY) Record revenue was driven by strong AI memory demand and higher DRAM and NAND prices. A large portion of net profit came from ₩63.3 trillion in investment-related gains, including gains on investment assets, rather than from its core semiconductor business. SK Hynix crashed -10% after the results and is now down -53% from its all-time high. Source: Bull Theory

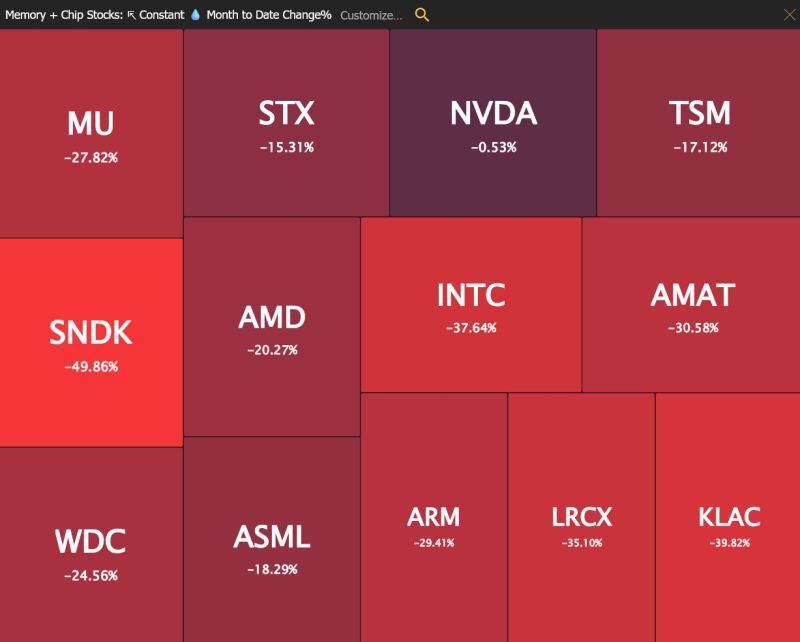

July has been nothing but brutal to chip and memory stocks

Source: TrendSpider

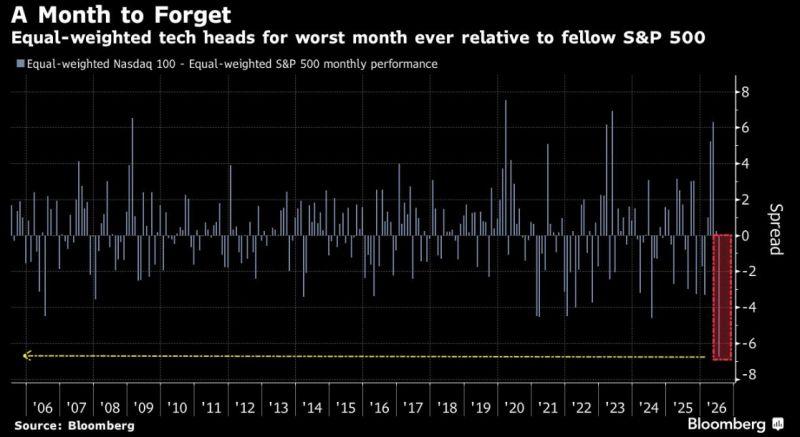

Nasdaq 100 Equal-Weight eyes historic divergence. Equal-weighted tech heads for worst month ever relative to S&P 500 Equal-Weight.

Source: HolgerZ, Bloomberg