SpaceX prospectus is expected to drop as soon as this week.

Space names are going crazy: Source: Negligible Capital

In case you missed it.... KKR Funds Loses $560 Million In 3 Months

The WSJ reports KKR’s big private-credit fund for regular investors just took a $560 Million bath (10% of its value) as loan defaults jumped to 8.1%. KKR's largest private-credit fund, primarily held by individual investors, experienced a significant $560 million loss in the first quarter due to an increasing number of loan defaults. Wall Street Journal (Markets) posted on X that this development highlights the challenges faced by private-credit funds as economic conditions fluctuate. The fund, which has been a popular choice among individual investors seeking higher yields, has been impacted by the financial instability of several borrowers. KKR share price has been cut in half and it’s now junk-rated.

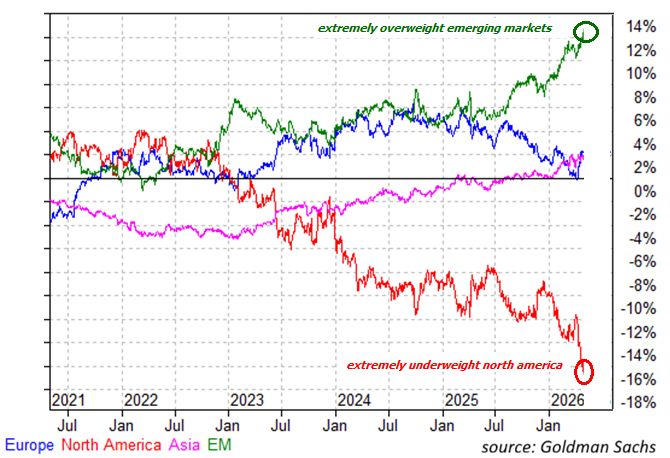

Hedge funds have rarely been this underweight North American stocks:

Hedge funds sold North American stocks for 3 consecutive weeks despite 3 consecutive weeks of S&P 500 all-time highs. This has pushed their allocation to North American equities down to the lowest on record relative to the MSCI All World Index, according to Goldman Sachs. At the same time, their allocation to Emerging Markets is up to an all-time high. What is happening here? Source: Global Markets Investor, Goldman Sachs

TRILLION DOLLAR BABY...

OpenAI's pre-IPO valuation has officially hit a record $1 trillion. Pre-IPO instruments trading onchain, backed 1:1 by SPV exposure on Jupiter, are providing a real-time proxy for the company’s implied IPO valuation. OpenAI’s implied valuation is now up +163% since October 2025. This comes as Anthropic is also nearing a potential $1+ trillion IPO and SpaceX is reportedly targeting $1.7+ trillion. The world has never had this many trillion-dollar private companies... Source: The Kobeissi Letter

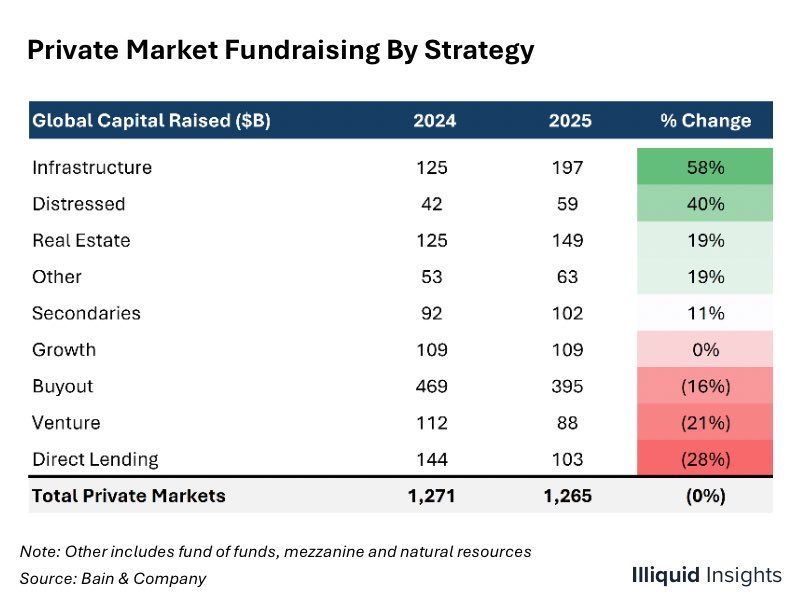

LPs are rotating.

Infrastructure and liquidity solutions (secondaries, opportunistic) are in. Software, buyouts and direct lending are out. Source: Illiquid Insights

Anthropic is receiving investment offers at an $800B valuation according to Business Insider.

This means Anthropic and OpenAI might be at near equal valuations now. Crazy how fast Anthropic has scaled enterprise versus OpenAI. $SKM should fly on this. $800B is over 2x where they last raised, which was at a $380B valuation. Source: Bloomberg, Negligible Capital

From the FT: OpenAI investors question $852bn valuation as strategy shifts

OpenAI’s $852bn valuation is facing scrutiny as it shifts strategy toward enterprise AI, competing with Anthropic while maintaining ChatGPT’s consumer lead. Some investors worry the company is unfocused and vulnerable, especially as Anthropic’s rapid revenue growth challenges its position. The Claude-maker’s annualised revenue surged from $9bn at the end of 2025 to $30bn at the end of March, driven by demand for its coding tools. Anthropic’s business appears to have leapfrogged OpenAI, which hit $25bn in annualised revenue in February, though the companies use different accounting methods to book revenue, making direct comparison difficult. Despite raising $122bn and strong leadership confidence, OpenAI is cutting side projects and prioritizing higher-margin tools like Codex. It is also expanding infrastructure and workforce. However, strategic pivots, abandoned initiatives, and intensifying competition from Anthropic and Google raise concerns about execution and long-term valuation ahead of a potential IPO.

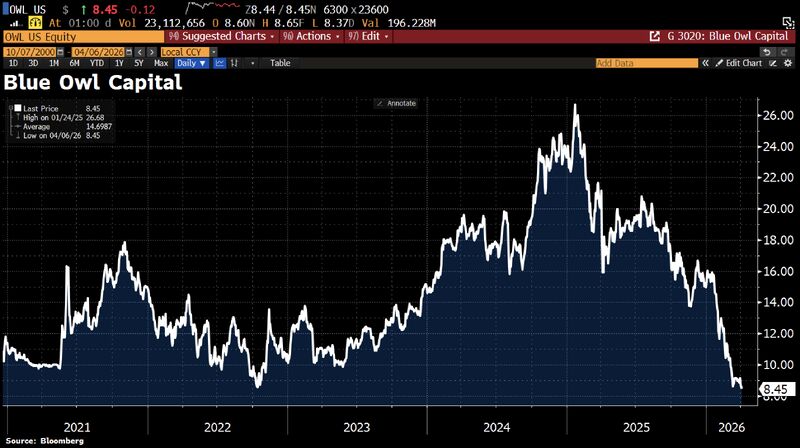

Is this a warning sign of a private credit crisis, or just market panic?

Blue Owl Capital, often considered a poster child for the private credit boom, closed at a record low as worries grow about the health of the $1.8tn market. The stock fell 1.4% to $8.45, slipping below its previous low from late 2022. It is now down 68% from its all-time high. Source: HolgerZ, Bloomberg