2025 rate cut odds:

from just ONE 2 weeks ago to MORE THAN TWO now... Source: zerohedge

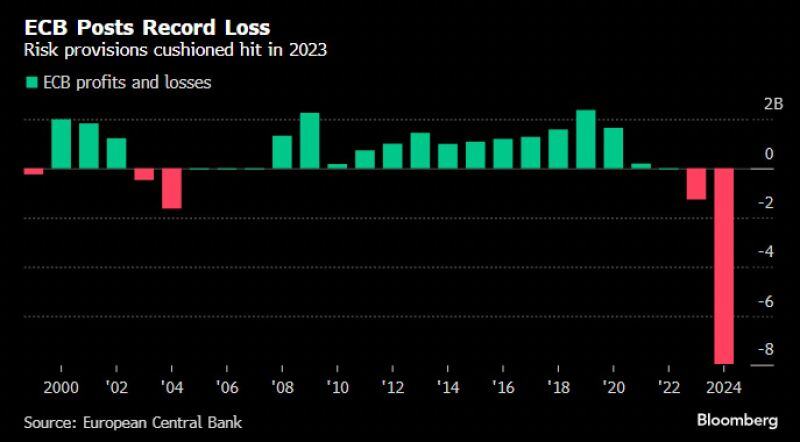

The ECB has recorded the biggest loss in its 25y history.

This is the result of its aggressive policy responses to Eurozone crises & surging inflation—1st buying large amounts of bonds & then sharply raising interest rates. As a result, ECB is earning less interest from the bonds it holds than it has to pay to banks for their deposits. Source: HolgerZ, Bloomberg

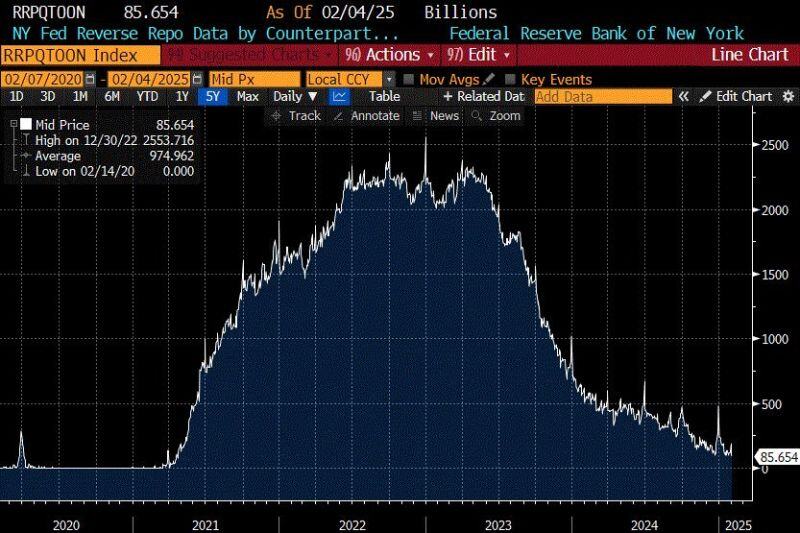

Federal Reserve's Reverse Repo Facility is plummeting

QE & money printing might start aggressively when this drains to 0 Source: Quinten | 048.ethm@QuintenFrancois, Bloomberg

Cut cut cut...

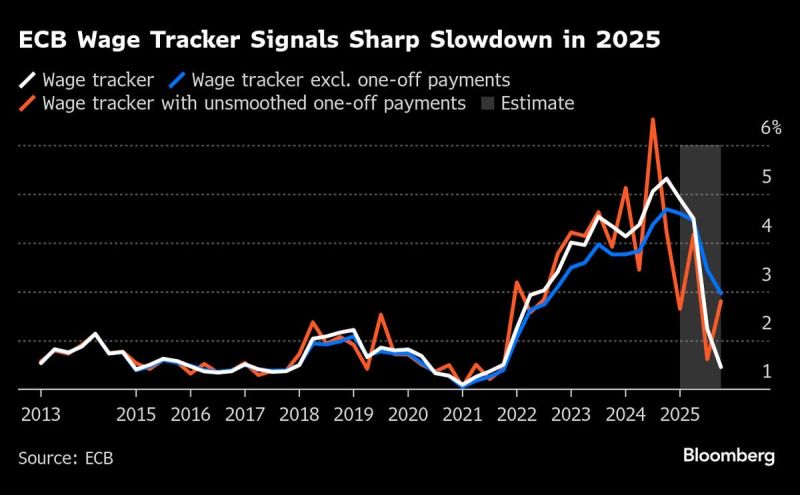

ECB’s Wage Tracker Points to Steep Slowdown This Year - Bloomberg Source: Bloomberg

BOC (Bank of Canada) ANNOUNCES AN END OF QUANTITATIVE TIGHTENING

AND WILL GRADUALLY RESTART ASSET PURCHASES IN EARLY MARCH. Who will be next?

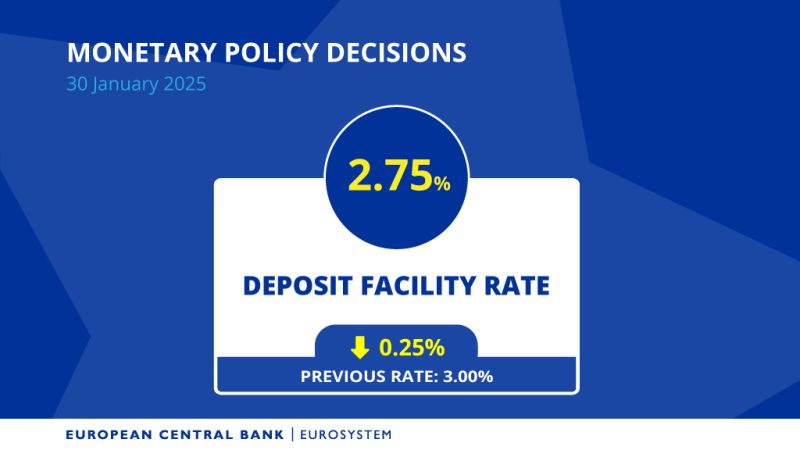

As expected, the ECB just cut interest rates by 0.25% to 2.75% as inflation nears 2% and growth stays weak.

Indeed, with Germany and France shrinking, the pressure was on. The eurozone economy is barely moving with Q4 GDP flat for the eurozone, with Germany (-0.2%) and France (-0.1%) dragging things down while Portugal (+1.5%) and Spain (+0.8%) showed some life. The ECB is playing it cautious, adjusting rates based on data. They reiterated that the disinflation process is well under way and that they see inflation converging towards 2%. The ECB says it’s not locking into a rate path—just watching inflation and economic data closely. The bond market is taking it quite positively with 10y Bond yield down 7bps at the time of our writing. With growth slowing, more cuts might be on the table. Let see what Mrs. Lagarde have to say during the conference call - especially with regards to wages and tariffs. Baring a major positive surprise coming from Germany on the fiscal side, the Eurozone growth outlook remains bleak - this opens the door to at least 1 rate cut every quarter.

The Fed held rates steady as widely expected.

The FOMC statement contains only minor changes that mark to market recent economic developments: 👉 "Labor market conditions remain solid" = Hawkish❗ 👉 "Inflation remains somewhat elevated." (The central bank notably removed reference to inflation making progress towards the goal) = Hawkish❗ The Fed will continue its QT program at an unchanged pace of $60 billion a month. The market does not expect rate cuts at least until June 2025. Source: Nick Timiraos, The Kobeissi Letter

Czech Central Bank Plans Bitcoin Reserve

Source: Bloomberg thru Willem Middelkoop