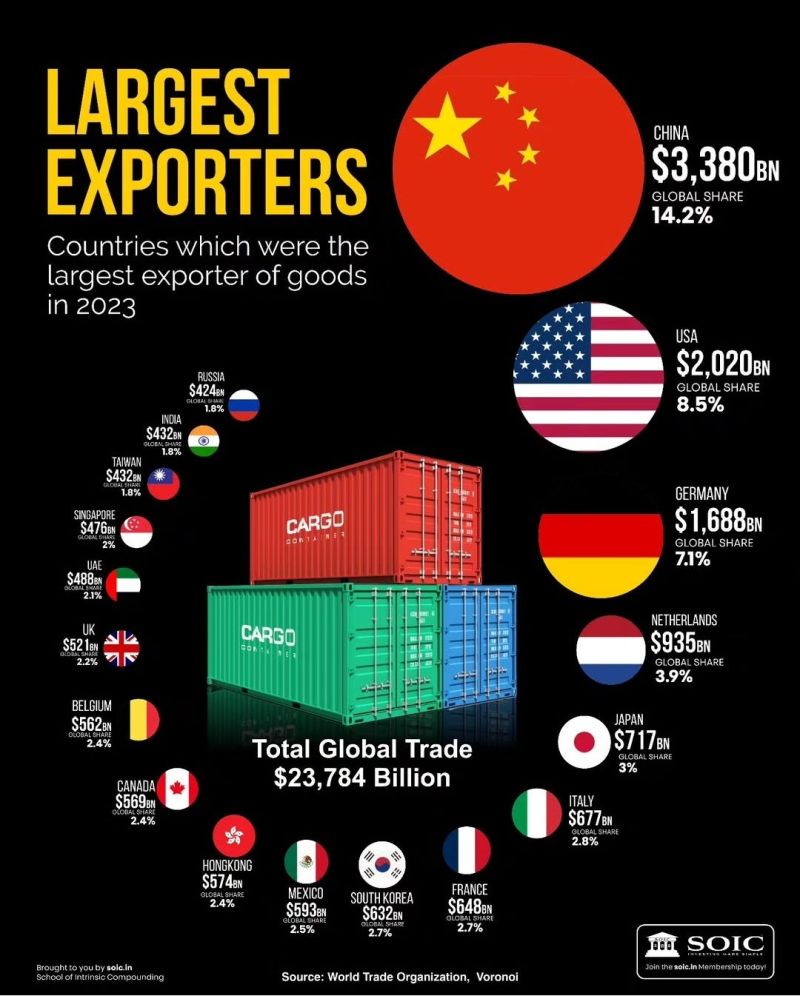

China is, by far, the largest exporter.

Source: Jason Smith @ShangguanJiewen on X

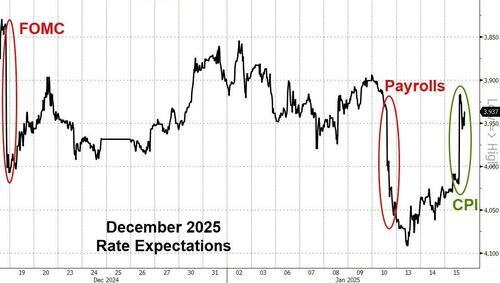

Yesterday, the easing of US inflation fears sparked a huge surge higher in rate-cut expectations for 2025 (back up to 40bps from 28bps)...

Source: Bloomberg, zerohedge

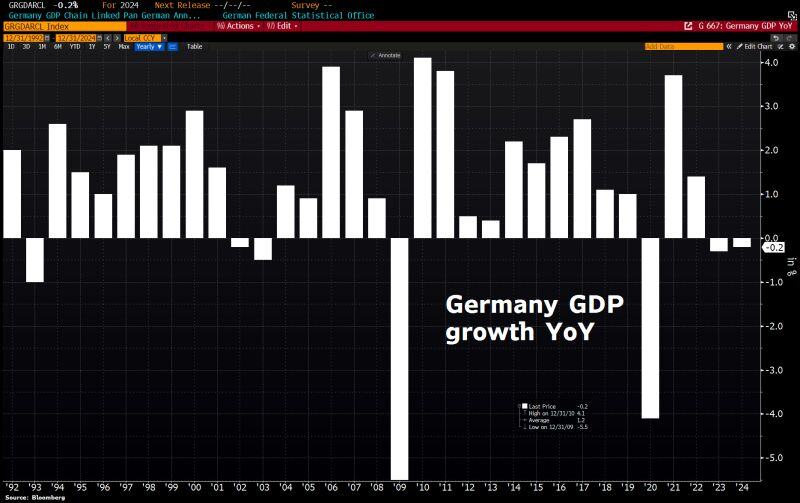

The German economy has shrunk for 2nd year in a row ahead of elections, driven by both cyclical & structural challenges

German GDP declined by 0.2% in 2024, following a 0.3% drop in 2023. This marks only 2nd time since 1950 that econ has contracted for 2 consecutive yrs. Germany's prospects for 2025 remain bleak. Bundesbank predicts growth of just 0.2% and warns that another contraction is even possible if US President-elect Trump follows through on his tariff threats. Source: HolgerZ, Bloomberg

Mortgage demand is collapsing:

US mortgage applications for single-family homes fell 3.7% last week, marking their 4th consecutive weekly decline. As a result, the mortgage demand index has fallen to the lowest since February 2024 and its 3rd lowest level in nearly 30 years. The index has now fallen a whopping -63% over the last 4 years. This comes as home financing costs have rapidly surged while prices remain at all-time highs. Since mid-September, 30-year fixed mortgage rates have risen ~110 basis points and are back above 7%. Mortgage demand is at 1990s levels. Source: The Kobeissi Letter, MBA Purchase index

Government spending is now half of the economy in most of the developed world....

Source: The Long View @HayekAndKeynes

Good news are coming... while US Q4 earnings season is off to a strong start thanks to banks beating estimates, US inflation numbers came in somewhat cooler than expected:

Core CPI slows to 3.2% in December from 3.3% in November. Analysts had expected the rate to remain unchanged at 3.3%. Overall CPI is unchanged at 2.9% as forecasted. Headline CPI inflation is up for 3 straight months, but core inflation is falling again. It seems enough to please investors: S&P 500 futures are surging over +85 points - the equivalent of a $750B market cap gain - as 10y US bond yields are tumbling by 10 basis points. The dollar is easing, gold is shining and cryptos is surging with bitcoin back to $99K. Alles gut... Source: Bloomberg

The first quarter of FY 2025 produced a deficit of $710.9 Billion.

That’s $200B more than the first quarter of fiscal 2024, or a 39% increase YoY. The US is now running a ~$3 TRILLION annual deficit...

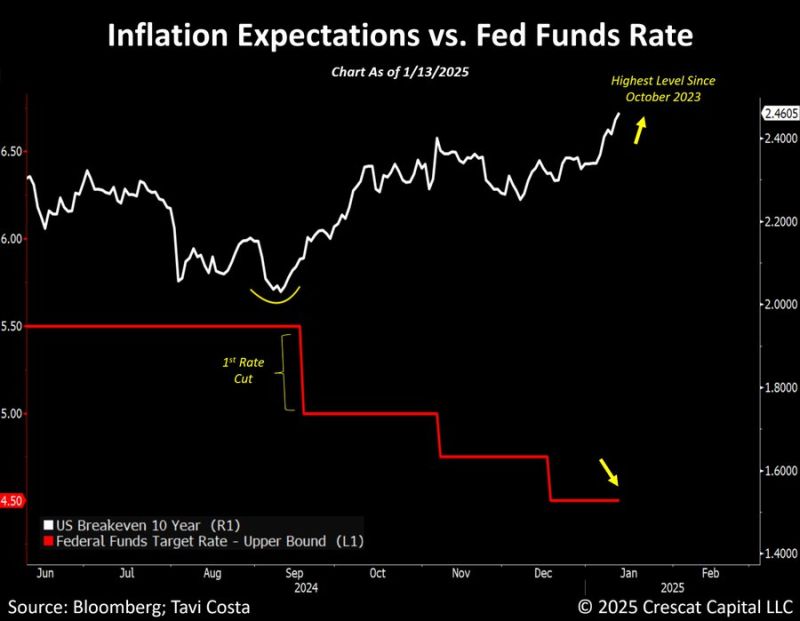

Inflation expectations have almost perfectly bottomed exactly when the Fed started to cut rates.

10-year breakeven rates are now at its highest level since October 2023. As highlighted by Tavi Costa, this is a reminder that when debt limits a monetary authorities actions, inflation becomes the path of least resistance. Source: Tavi Costa, Bloomberg