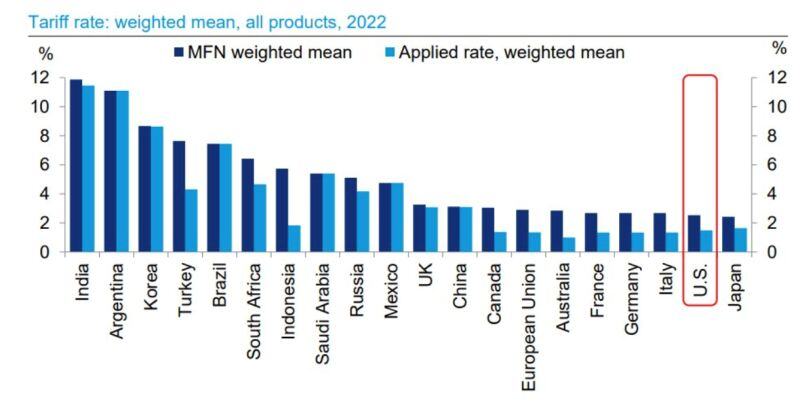

Believe it or not, but the us has one one of the lowest tariff rates in the developed world... See chart below courtesy of DB.

NB: Most favored nations (MFN) Weighted mean tariff is the average of most favored nation rates weighted by the product import shares corresponding to each partner country.

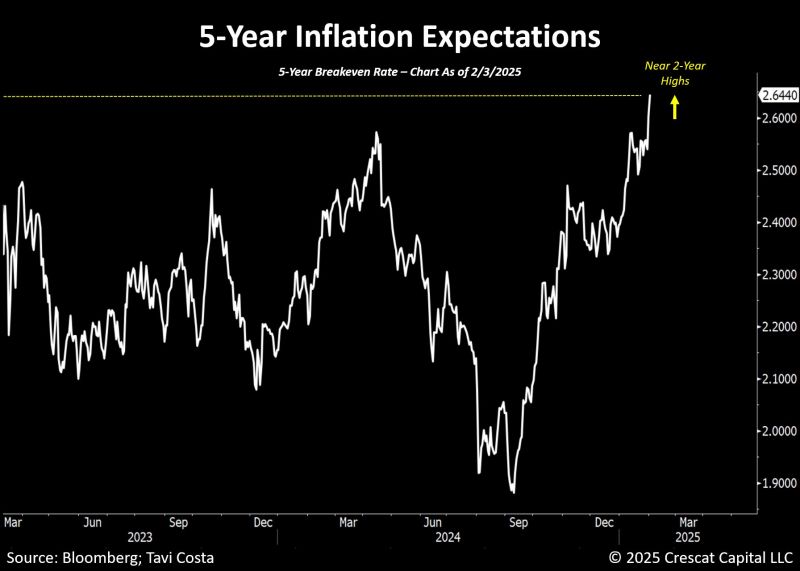

Are tariffs inflationary? us 5-year breakeven rate just surged to its highest level in nearly 2 years.

Source: Tavi Costa, Bloomberg

The price of eggs in the U.S. is at an all time high and continues to climb.

Due to the ongoing bird flu outbreak and inflation, egg prices sat at $4.15 in December, that was up from $3.65 in November. The unusually high prices come after the outbreak...

Will the US have to crash stocks to save bonds ???

Source: Michael A. Gayed

This is what happened to US government revenues from tariffs during Trump's first tradewar.

Source: DB

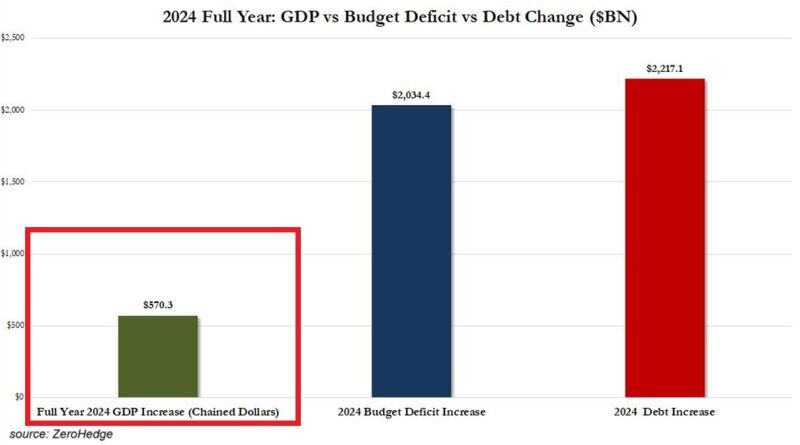

US growth is not a miracle, it is fully DEBT driven:

It took a MASSIVE $2.2 trillion in public debt to create $570 billion in GDP growth in 2024 (before revisions). In other words, it took $3.9 of debt to generate $1 of economic growth. Source: Global Markets Investor

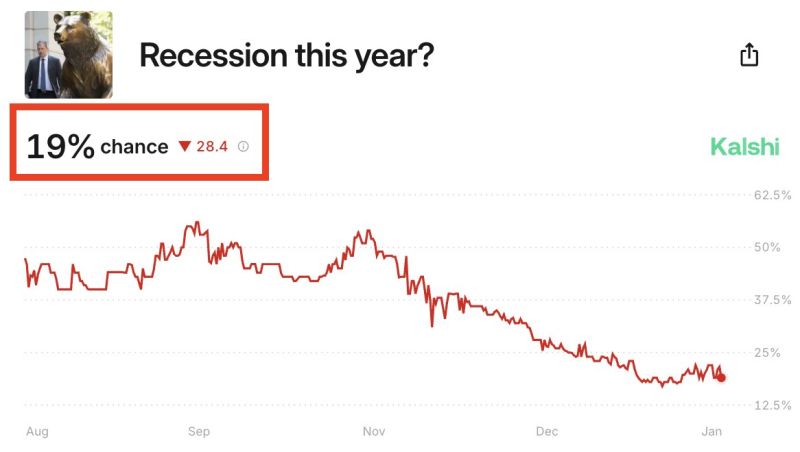

The odds of the US economy entering a recession in 2025 have fallen to a fresh low of just 19%.

Since Election Day, the odds of the US economy entering a recession are down 35 percentage points, per @Kalshi .This comes after the preliminary reading of Q4 2024 GPD showed the US economy grew by 2.3%. Even as interest rates remain elevated and inflation rebounds, the US economy is growing. Source: The Kobeissi Letter

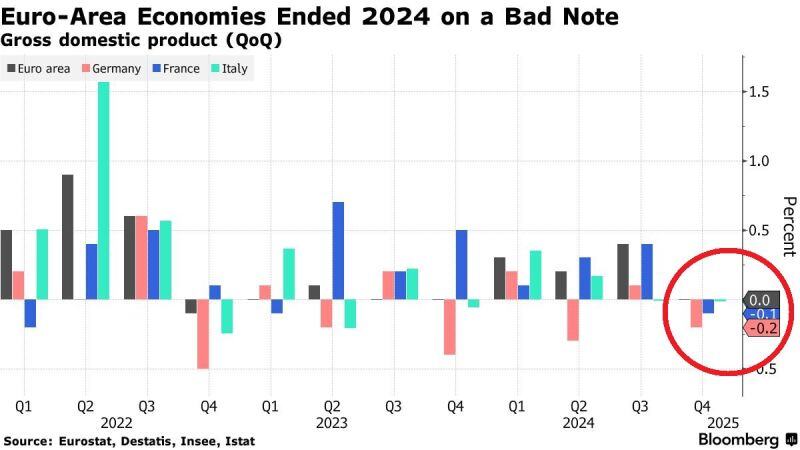

🚨What is happening with the eurozone economy?

Germany and France GDP fell 0.2% and 0.1% in Q4 2024. Italy's GDP was flat for the 2nd consecutive quarter. In effect, Euro-area economy did not grow in Q4 2024. Germany has contracted for 2 consecutive years in 2023 and 2024... Source: Bloomberg, Global Markets